http://klse.i3investor.com/blogs/sumato88/122720.jsp

Wow, I am so surprised that many ppl don't get my logic and my

calculations for Petronm's 1Q17 profit. Let me put things in order and

hopefully you can see it now.

1) Malaysia operations (listed co + 2 non-listed co in Malaysia owned

by Petron Corp) reported Peso 1.5bn net profit in 1Q17, +335% yoy. So,

1Q16 net profit from Malaysia operation = Peso 345m

Workings

a) (1Q17 profit /1Q16 profit) - 1 = yoy growth

B) (1500/345) - 1 = 335% (In case you are still confuse, ask

yourself, what's the yoy growth rate if your profit increase from 100 in

1Q16 to 150 in 1Q17? The answer is 50% right? Pls apply the same

formula.)

2) Peso 345m net profit in 1Q16 equal to RM30m. This was the profit

from Malaysia operation in 1Q16, including 2 non-listed co. So what's

the profit belong to non-listed co? Petronm (listed co) reported RM16.6m

net profit in 1Q16, so

A) Petronm's 1Q16 profit + 2 non-listed co 1Q16 profit = RM30m

B) RM16.6m + 2 non-listed co 1Q16 profit = RM30m

C) 2 non-listed co 1Q16 profit = RM30m - RM16.6m = RM13.4m

3) Given that 2 non-listed co is involved in fuel marketing and

retailing (basically means petrol stations la), the profit growth should

be steady due to fixed margin, so it should grow in tandem with sales

volume growth. Petron Corp mentioned Malaysia sales volume + 6% yoy in

1Q17, so we can safely assume 2 non-listed co profit grow 10% yoy in

1Q17, from RM13.4m to about RM15m.

4) So how much of RM130m or Peso 1.5bn 1Q17 profit attributes to Petronm?

RM130m - RM15m (2 non-listed co estimated profit) = RM115m (42.6 EPS)

My final advise, if you still don't understand, please don't buy any

stocks anymore as stock investment could be way too complicated for you.

Saturday, May 13, 2017

Thursday, May 11, 2017

Petronm: A Simple Math, 5x PE even after the 100% rally YTD?

First, I would like to congrats to all the shareholders of Petronm who do not sell the shares due to oil price volatiliy. The coming quarter results will be a reward to the believers. As some of you may have aware, Petron Corp (the parent co of Petronm) has released a press statement on 8 May 2017 and mentioned that net income from Malaysia operation in 1Q17 surged 335% to Peso 1.5bn. Many are guessing the profit that the listed co, Petronm will report in the upcoming 1Q17. Well, let me try to solve this simple math.

1) Peso 1.5bn = RM130m net income in 1Q17, given that Petron Corp didn't mention this is net income after minority, we can safely and conservatively assume this is the Malaysia operation net income before minority.

2) 335% yoy increase implied 1Q16 net income from Malaysia operation = Peso346bn or about RM30m

3) Both of these numbers include 2 non-listed sister co that Petron Corp owns in Malaysia, hence, we need to figure out how much is the profit belongs to the non-listed entities.

4) Petronm reported RM16.6m net income in 1Q16, as a result, non-listed sister companies should have contributed RM13.4m in 1Q16.

5) Given that the 2 non-listed sister companies are in fuel marketing and retailing biz, it is safe to assume that the profit growth is likely to be very steady, rise according to the volume + some margin improvement due to operating leverage. As Petron Corp mentioned Malaysia sales volume +6% yoy in 1Q17, we can assume 10% net income growth for non-listed sister co for 1Q17, which probably works out to about RM15m profit.

6) If you minus RM15m out of RM130m net income reported by Malaysia operation, we can get a profit estimate of RM115m for Petronm in 1Q17, this is a whopping 7-fold increase from 1Q16 and another quarter of RM100m profit!

7) I understand that the crack spread is still relatively stronger qoq in April and May to date. If this sustain throughout the 2Q17, we will probably see another RM100m profit in 2Q17, paving way for Petronm to achieve net cash position and record profit in 2017. Initially I was looking at RM300m profit in 2017, but now it seems to be easily beaten if Petronm can achieve RM200-230m profit in 1H17.

In conclusion, I think there is still plenty of upside from current share price, even though the stock had a good rally YTD (almost 100%). At 5x PE (assuming RM400m profit, +63% yoy), I personally think this stock is too cheap to sell.

PETRON Corp's Media release entitled "PETRON POSTS RECORD QUARTER, HITS P5.6 BILLION IN NET INCOME".

1) Peso 1.5bn = RM130m net income in 1Q17, given that Petron Corp didn't mention this is net income after minority, we can safely and conservatively assume this is the Malaysia operation net income before minority.

2) 335% yoy increase implied 1Q16 net income from Malaysia operation = Peso346bn or about RM30m

3) Both of these numbers include 2 non-listed sister co that Petron Corp owns in Malaysia, hence, we need to figure out how much is the profit belongs to the non-listed entities.

4) Petronm reported RM16.6m net income in 1Q16, as a result, non-listed sister companies should have contributed RM13.4m in 1Q16.

5) Given that the 2 non-listed sister companies are in fuel marketing and retailing biz, it is safe to assume that the profit growth is likely to be very steady, rise according to the volume + some margin improvement due to operating leverage. As Petron Corp mentioned Malaysia sales volume +6% yoy in 1Q17, we can assume 10% net income growth for non-listed sister co for 1Q17, which probably works out to about RM15m profit.

6) If you minus RM15m out of RM130m net income reported by Malaysia operation, we can get a profit estimate of RM115m for Petronm in 1Q17, this is a whopping 7-fold increase from 1Q16 and another quarter of RM100m profit!

7) I understand that the crack spread is still relatively stronger qoq in April and May to date. If this sustain throughout the 2Q17, we will probably see another RM100m profit in 2Q17, paving way for Petronm to achieve net cash position and record profit in 2017. Initially I was looking at RM300m profit in 2017, but now it seems to be easily beaten if Petronm can achieve RM200-230m profit in 1H17.

In conclusion, I think there is still plenty of upside from current share price, even though the stock had a good rally YTD (almost 100%). At 5x PE (assuming RM400m profit, +63% yoy), I personally think this stock is too cheap to sell.

PETRON Corp's Media release entitled "PETRON POSTS RECORD QUARTER, HITS P5.6 BILLION IN NET INCOME".

Market leader Petron Corporation continued its strong momentum in the first three months of 2017 posting a consolidated net income of P5.6 billion – the highest quarterly income in the company’s history – double the previous year’s first quarter earnings of P2.8 billion. Net income from Philippine operations grew 69% to P4.1 billion and accounts for 74% of consolidated figures while income from Malaysian operations surged 335% to P1.5 billion.

Petron’s exceptional performance in both markets is mainly due to its strong focus on more profitable segments, production of higher-margin fuels and petrochemicals, and aggressive market expansion.

In the Philippine retail segment, Petron’s volumes grew by another 6% while its LPG and Lubricants businesses grew by 5% and 16%, respectively. Currently, Petron has the highest network count with about 2,300 service stations – more than its next three competitors combined – which retail its cutting edge fuels and serves as outlets for its other products and services.

Petrochemical export volumes more than doubled over the period allowing Petron to capture better margins from benzene, toluene, mixed xylene, and propylene. Meanwhile, exports of fuels were lessened as more volumes were sold locally as part of the company’s strategy to optimize margins.

The company’s Malaysian operations also experienced steady growth with domestic volumes growing by another 6%, fueled by double-digit growth from the Commercial and Lubricants sectors.

Petron’s exceptional performance in both markets is mainly due to its strong focus on more profitable segments, production of higher-margin fuels and petrochemicals, and aggressive market expansion.

In the Philippine retail segment, Petron’s volumes grew by another 6% while its LPG and Lubricants businesses grew by 5% and 16%, respectively. Currently, Petron has the highest network count with about 2,300 service stations – more than its next three competitors combined – which retail its cutting edge fuels and serves as outlets for its other products and services.

Petrochemical export volumes more than doubled over the period allowing Petron to capture better margins from benzene, toluene, mixed xylene, and propylene. Meanwhile, exports of fuels were lessened as more volumes were sold locally as part of the company’s strategy to optimize margins.

The company’s Malaysian operations also experienced steady growth with domestic volumes growing by another 6%, fueled by double-digit growth from the Commercial and Lubricants sectors.

Petronm: Growing evidence of record 1Q17

Spike in maintenance expected to boost oil refining margins

http://www.reuters.com/article/us-oil-refinery-maintenance-idUSKBN15G55W

http://www.reuters.com/article/us-oil-refinery-maintenance-idUSKBN15G55W

Reuters, 2 Feb 2017- Increased refinery maintenance in Asia and the Middle East is expected to boost profits for operators in other regions in the first half of this year, market watchers said on Wednesday.

Refineries worldwide ran hard during the past two years to capitalize on low oil prices, with Chinese refineries processing a record amount of crude in 2016, meaning that some units now have no choice but to carry out maintenance.

Outages in the first half will equate to nearly 1 million barrels per day (bpd) more than in the same period last year, speakers told the Platts Middle Distillates conference in Antwerp.

Though this is likely to help to clear the stocks of oil products such as diesel, gasoline and jet fuel that poured into the world's storage tanks over the past two years of excess, it is also likely to cut into demand for crude oil just as prices recover on the back of production cuts led by the Organization of the Petroleum Exporting Countries (OPEC).

Trading house Gunvor's chief economist, David Fyfe, said that he expects "healthy and robust" refinery margins in the first half of the year.

Gunvor data shows that maintenance in February and March will take close to an additional 1 million bpd offline compared with the same months in 2016.

Both Fyfe and James McCullagh, oil products analyst with Energy Aspects, said the bulk of the work will be concentrated in Asia and the Middle East, offering a reprieve to Europe's comparatively less advanced refineries, which have depended largely on demand -- or supply problems -- in other regions to underpin profits.

Energy Aspects expects Asian refineries alone to account for 900,000 bpd more in offline capacity in April, compared with the prior year, and 250,000 bpd more over first half of 2017. Those shutdowns, paired with diesel stocks in China that it estimates are near record lows, would underpin refinery profits in most regions, he said.

Fires and other issues at refineries worldwide this month suggest that many units are feeling the effects of the ramp-up in output over the past year or two.

"The strong margins have in a way stored up unplanned outages," McCullagh said.

This month's outages included Abu Dhabi National Oil Company's Ruwais refinery, two refineries in West Africa and others in India, Indonesia and Brazil.

S.Korea's S-Oil expects firm refining profits in 2017

http://www.cnbc.com/2017/02/01/reuters-america-update-1-skoreas-s-oil-expects-firm-refining-profits-in-2017.html

SEOUL, Feb 2 (Reuters) - South Korea's S-Oil Corp expects healthy refining profits this year, buoyed by growing demand for oil products in places such as China and Southeast Asia.

The country's third-largest oil refiner said in a quarterly earnings statement on Thursday that global oil demand would grow soundly in 2017, although the rate of increase could ease slightly from last year.

"Healthy margins are expected as 1.32 million barrels per day (bpd) of oil demand growth will outstrip an incremental net capacity increase of 574,000 bpd," the company said, referring to the profit margin on refining barrels of crude oil.

Inventory gains and a recovery in refining margins helped S-Oil, whose top shareholder is Saudi Aramco <IPO-ARMO.SE>, notch up a 444 billion won ($386 million) profit in the last quarter of 2016, compared with a loss of 42.9 billion won the year before.

S-Oil treasurer Shin Kwan-bae said on a call with analysts that the company expected the official selling price (OSP) for Arab Light crude, supplied by Saudi Arabia, to remain steady in Asia from last year.

He said that even if Middle Eastern crude supply drops in the wake of a deal by producers to curb output, Saudi Arabia would not want to harm its market share in Asia by increasing OSPs.

A company official said S-Oil planned to carry out less scheduled maintenances this year, limiting such work to a condensate fractionation unit (CFU) and a No.2 paraxylene unit. He did not give further details.

Industry sources have said S-Oil would shut down its No.1 residue hydro desulphurisation unit (RHDS) and crude oil refining unit in April for about a month.

S-Oil also said on Thursday that its 2018 expansion project was on track to complete in the first half of next year.

Under the project, the company will build a residual fuel oil upgrading system and an olefin production system that will churn out 405,000 tonnes of polypropylene a year, along with other products.

Asian Oil refinery margins jump on outages in Mideast, Asia

http://www.reuters.com/article/us-asia-crude-refineries-idUSKBN151183

Reuters, 17 Jan 2017- Several refineries in the Middle East and Asia have shut down in the past week due to fires and other technical problems, leading to a jump in profit margins for facilities still operating.

The higher Asian refining margins have beat back concerns that profits would fall as crude oil prices gained as the Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC producers began to implement their agreed production cuts from January to reduce global oversupply.

Besides the fires and other shutdowns, maintenance and repairs at refineries in Indonesia by Pertamina [PERTM.UL] and in Singapore by Royal Dutch Shell have further boosted oil product margins.

"Margins will be supported as these outages will affect the ability of the region to stock up before maintenance picks up in March," said Nevyn Nah, a fuel analyst at Energy Aspects in Singapore.

Profits for processing a barrel of Dubai crude at a Singapore refinery jumped to $7.64 a barrel on Jan. 16, the highest since Nov. 30, Reuters data showed.

(richDad) - PETRONM: More than 50% upside (PETRON CORP media release says 1Q earnings to TRIPLE)

1. Main business = oil refinery and retail. These descriptions are from their website which says “Petron Subsidiaries in Malaysia comprise of Petron Malaysia Refining & Marketing Bhd (formerly known as Esso Malaysia Berhad), a public listed company listed on Bursa Malaysia; Petron Fuel International Sdn Bhd (formerly known as ExxonMobil Malaysia Sdn Bhd); and Petron Oil (M) Sdn Bhd (formerly known as ExxonMobil Borneo Sdn Bhd). As a major and reputable company in Oil & Gas, our involvement in refining and retailing of world-class quality of petroleum products and related services, helps the country to meet its energy demands and contributes to the overall socio-economy advancements. Our robust petroleum marketing business that encompasses over 550 service stations nationwide bring high quality, clean energy products to motorists.”

In lay man term, the retail business is the petrol station that we see and possibly pump petrol. In order to get the oil to the station, they need to refine it first (from the crude oil). So, PETRONM is also involved in refining the crude oil to petrol and other products. If you ever wonder how many stations does PETRONM has, it is 550 from the website.

To fully understand what PETRONM does you can visit their website here

http://www.petron.com.my/web/site/slider/9

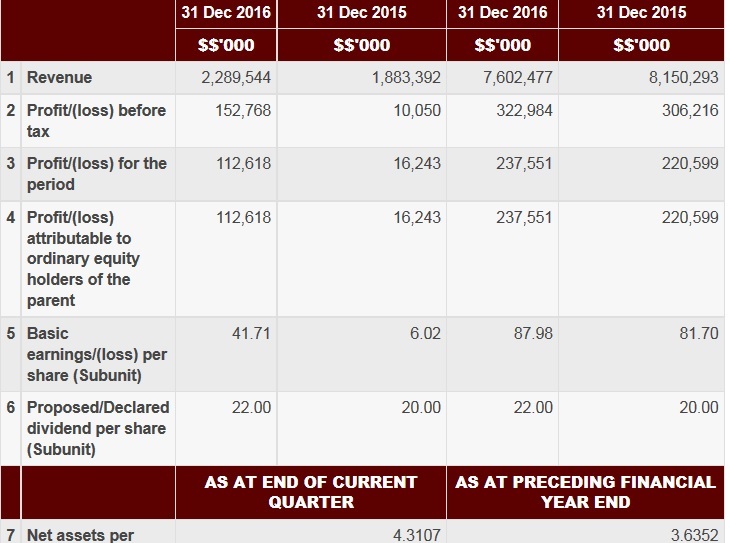

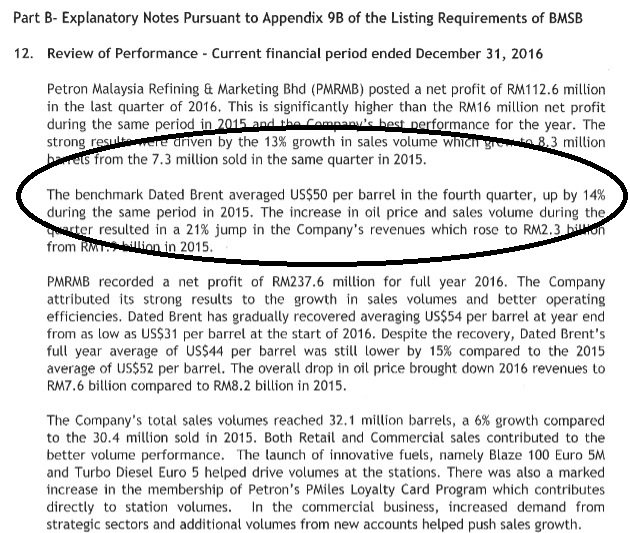

2. Stellar earnings growth in 4QFY16 (+593% to RM112.62m). Accordingly, EPS also jump 593% to 4171sen. Reason for the earnings surge can be seen below. It is mainly due to 13% increase in sales volume (which means this is operation improvement and is sustainable).

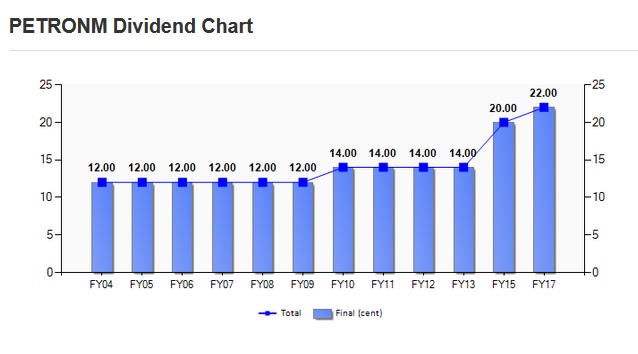

3. Consistent paid dividend (10 out of 11 years) in the past. FY16 dividend has increased by 10% to 22 sen (against 20 sen in FY16). The Company has consistently paid dividend in the past with only one miss in FY14 (but that one is due to loss in that financial year under previous management).

4. SUPER CATALYST = 1QFY17 earnings to triple??? Sometimes, you need to monitor global news as it is increasingly hard to make ALPHA GAIN from the market in Malaysia. Just three days ago, PETRON CORPORATION (parent company of PETRON MALAYSIA made an announcement of its 1Q profit which doubled. BUT the most important thing is it mentioned that

Income from Malaysia operation surged 335% to Peso 1.5 billion (about RM130m). AND Malaysia investors may not fully realize this because it is not annouced yet in the BURSA!!!

You can read the full Media Release from Singapore Exchange here

http://infopub.sgx.com/FileOpen/05%2008%2017%20-%20Media%20Release%20-%20Petron%20Posts%20Record%20Quarter%20Hits%20P5.6%20Billion%20in%20Net%20Income.ashx?App=Announcement&FileID=452503

5. Long term value is between RM12 to RM15 per share. There is more than 50% upside that I am looking at. I think that the Company is worth between 8x to 10x PE. The 8x PE is if you take oil and gas Company PE. While the 10x PE is the minimum for consumer sector PE. I think PETRONM is a mixture of O&G and CONSUMER because its petrol station business is basically similar to 7 ELEVEN. For FY17, the 1Q net profit is assumed at RM130m and I multiply this by 3 to get the full year earnings. I purposely ignore one quarter for conservativeness purpose in my calculation (that's why not multiplying by 4).

That gives me FY17 earnings of around RM390m (or RM1.45 of EPS).

8x PE * RM1.45 FY17 EPS = RM11.60 (round up to RM12)

10x PE * RM1.45 FY17 EPS = RM14.50 (round up to RM15)

For record keeping purpose, I am using last Tuesday closing price of RM7.97

In lay man term, the retail business is the petrol station that we see and possibly pump petrol. In order to get the oil to the station, they need to refine it first (from the crude oil). So, PETRONM is also involved in refining the crude oil to petrol and other products. If you ever wonder how many stations does PETRONM has, it is 550 from the website.

To fully understand what PETRONM does you can visit their website here

http://www.petron.com.my/web/site/slider/9

2. Stellar earnings growth in 4QFY16 (+593% to RM112.62m). Accordingly, EPS also jump 593% to 4171sen. Reason for the earnings surge can be seen below. It is mainly due to 13% increase in sales volume (which means this is operation improvement and is sustainable).

3. Consistent paid dividend (10 out of 11 years) in the past. FY16 dividend has increased by 10% to 22 sen (against 20 sen in FY16). The Company has consistently paid dividend in the past with only one miss in FY14 (but that one is due to loss in that financial year under previous management).

4. SUPER CATALYST = 1QFY17 earnings to triple??? Sometimes, you need to monitor global news as it is increasingly hard to make ALPHA GAIN from the market in Malaysia. Just three days ago, PETRON CORPORATION (parent company of PETRON MALAYSIA made an announcement of its 1Q profit which doubled. BUT the most important thing is it mentioned that

Income from Malaysia operation surged 335% to Peso 1.5 billion (about RM130m). AND Malaysia investors may not fully realize this because it is not annouced yet in the BURSA!!!

You can read the full Media Release from Singapore Exchange here

http://infopub.sgx.com/FileOpen/05%2008%2017%20-%20Media%20Release%20-%20Petron%20Posts%20Record%20Quarter%20Hits%20P5.6%20Billion%20in%20Net%20Income.ashx?App=Announcement&FileID=452503

5. Long term value is between RM12 to RM15 per share. There is more than 50% upside that I am looking at. I think that the Company is worth between 8x to 10x PE. The 8x PE is if you take oil and gas Company PE. While the 10x PE is the minimum for consumer sector PE. I think PETRONM is a mixture of O&G and CONSUMER because its petrol station business is basically similar to 7 ELEVEN. For FY17, the 1Q net profit is assumed at RM130m and I multiply this by 3 to get the full year earnings. I purposely ignore one quarter for conservativeness purpose in my calculation (that's why not multiplying by 4).

That gives me FY17 earnings of around RM390m (or RM1.45 of EPS).

8x PE * RM1.45 FY17 EPS = RM11.60 (round up to RM12)

10x PE * RM1.45 FY17 EPS = RM14.50 (round up to RM15)

For record keeping purpose, I am using last Tuesday closing price of RM7.97

Subscribe to:

Comments (Atom)