Making strides: Lim with the KL River City project, which he envisions to turn into a thriving community like Yarra of Melbourne.

DATUK Seri Lim Keng Cheng was born in Jalan Gombak and studied at Setapak High School. Now, he has his eyes set on transforming the Sentul-Gombak-Setapak area, which he says is still underdeveloped. He aims to make the area into a liveable place like Melbourne.

This 54-year-old Sentul homeboy (who goes by the initials KC), the managing director of Ekovest Bhd, has rebuilt a Chinese primary school and a high school there.

Until recently, KC has not made himself distinctively known to the corporate world. His name did not pop into view when the media wrote about Ekovest and Iskandar Waterfront City Bhd (IWC). Only Tan Sri Lim Kang Hoo, the Ekovest executive chairman and KC’s uncle, was mentioned.

Yet, KC is the driving force behind Ekovest, which is Kuala Lumpur City Hall’s project delivery partner for the River of Life project and DUKE highways.

Early victory: Lim with a picture of a project he undertook in his early years in Sabah. He says he and his uncle Tan Sri Lim Kang Hoo made their first RM100mil while they were in Sabah.

Indeed, KC has been in the construction, property and infrastructure line for more than 30 years.

“I am a business partner of Tan Sri Lim Kang Hoo. Before Ekovest, we were already doing business together,” declares KC.

“But since he is my uncle and executive chairman of Ekovest, and holds 32% stake in the company, while I have only 6.12%, I should give him due respects,” adds KC at the outset of a recent interview with Sunday Star.

Yes, for too long, this trilingual and energetic man who has worked alongside Kang Hoo quietly to jointly build up their companies, including Ekovest and IWC. However, many are not aware of this fact.

KC’s role in Ekovest

Acknowledgement of KC’s role in Ekovest is stated in its latest company profile. Under the section Capable Management Team, the company writes: “Executive chairman Tan Sri Datuk Lim Kang Hoo and managing director Datuk Seri Lim Keng Cheng have been managing the company since (its) inception”.Venturing into Sabah together with his uncle while he was 25 in the early 1980s, this neat-looking man proudly claims he was responsible for the building infrastructure in Felda Sahabat, twice the size of Singapore.

“We made our first RM100mil in Sabah,” says KC, as he shows photographs of the Sabah projects in his office that carry his footprint.

“I was born here, in Batu 4, Jalan Gombak, in a house with number 229A. However, there was no road linking my old house to the main road then. Kang Hoo also lived there then.

“The Sentul-Gombak-Setapak area is still an underdeveloped area. I want to transform this into a liveable place. This is why I want to do a lot of development and CSR work here,” says KC in Ekovest’s office, which stands obliquely opposite the area where he was born.

“The old house is still there. We – including Kang Hoo – still celebrate Chinese New Year there. But now, we have already built a road to connect with the main road,” adds KC as he flashes his handphone to show the location of his old house.

Due to his humble background and vast experience in infrastructure, KC says he could plan cost efficient and workable highways.

In this regard, he has contributed significantly to the success of the Duta-Ulu Kelang Expressway (DUKE). He is also instrumental in convincing Kuala Lumpur City Hall (DBKL) to grant further concessions to Ekovest to extend the DUKE expressways, named as DUKE-3.

DUKE-1 and DUKE-2 are providing alternative routes for road users and have served as an efficient traffic dispersal system in and around Kuala Lumpur to relief traffic congestion.

Toll collection and recent sale of a 40% stake in DUKE-1 and DUKE-2 have boosted the earnings of Ekovest and this is reflected in the rise of its share price. On Thursday, Ekovest share closed at RM2.35 – which was at a six years’ high.

Another of KC’s passionate project is the River of Life project, which involves the improvement of water quality and beautification works along the river from Gombak to the Kuala Lumpur city centre.

Ekovest, which has land-bank and property development projects such as EkoRiver Centre and Ekovst Tower along the river, has on its plate a total GDV of RM7.8bil when all the planned projects are completed.

“My vision is to convert the entire run-down area into a river city with waterfront property development and leisure activities. It will be a place for people to work, live, jog and cycle, cruise in water taxi like the Yarra River of Melbourne.

“Our vision of creating a world class river front development along Gombak River is gaining momentum and we are looking to deliver some of the most vibrant commercial and residential properties in this area.”

According to KC, multi-billionaire Kang Hoo – ranked as one of the top 30 tycoons in Malaysia by Forbes Asia in 2014 – is focussing his attention on IWC and the development of Bandar Malaysia.

KC is charged with taking care of Ekovest.

In a two-hour interview, KC talks enthusiastically about Ekovest projects, his vision and education. Below are excerpts:

Q: What is the latest on DUKE highways? Why are these highways so successful?

A: We have a DUKE Master Plan, with a total of ten functional and cost-effective highways. We are developing the third one. Our planning team will keep submitting proposals on future DUKE projects as and when the need arises.

Within this plan, we provide one tolled road system on top of an existing council road to give an alternative route for drivers who are willing to pay to avoid traffic jams.

We have studied the benefits to be enjoyed by road users and planned according to their needs. This is the success story of our DUKE.

The DUKE concept was based on a study done by JICA (Japan International Cooperation Agency) in the 1980s to fill in the gap in highway connectivity. We submitted our plan to DBKL and got the approval.

There are many highways all over Kuala Lumpur, but they are not connected. We fill in this gap and build “highway connectors”.

But we also innovate to add value to our highways. For example, we are building DUKE-2’s integrated park-and-ride facility at the Segambut Toll Plaza that will allow DUKE’s users to park their cars and hitch a KTM ride at a brand new KTM (train) station, which is two stops away from KL Sentral.

Known as Segambut Rest and Service Area, this park-and-ride complex will be able to house 4,000 cars. This will ensure fewer cars move into and out of the city centre. Hence, it will reduce traffic congestion. (The new KTM train station is expected to be completed in 2018)

Your property development projects appear to concentrate in the Sentul area.

I was born here. My original home is still here. There was no access road from Jalan Gombak to my old house, yet the postman could find it.

My father passed away when I was 14 years old. My study was funded by Lee Foundation. For this reason, I have rebuilt the Lee Rubber primary school building in this area. From road construction and property development to the River of Life project, I hope to create a liveable Sentul-Gombak-Setapak region The whole city will be like Melbourne and Vancouver.

All these years, you have been overshadowed by Tan Sri Lim Kang Hoo, although you are a property man in your own right. Is this observation accurate?

Ekovest, with total staff of 2,000, is managed by a committee. No single person makes the decision.

My uncle Kang Hoo holds a 32% stake in the company while I have 6.12%. As he is my uncle and the company’s executive chairman, I should give him due respects. When my father died, the small family construction outfit run by him was taken over by Kang Hoo. I started helping him when I was in high school.

When I was 25, we went to Sabah together and worked on the infrastructure of Felda Sahabat. In Lahad Datu, we provided 2,500 jobs to the gun-wielding unemployed and helped solve the social problems there.

While in Sabah, we took over a RM2 company called Ekovest. That’s where we made our first RM100mil for Ekovest. After that, we went to Labuan to build the offshore financial centre. Kang Hoo and I were business partners before Ekovest, and are still partners.

Now, Kang Hoo places his focus on IWC and Bandar Malaysia investment, while I take charge of Ekovest projects.

What are the plans ahead for Ekovest?

We will keep inviting institutional funds, such as EPF (Employees’ Provident Fund), to be our investors and strategic partners. These partners will stay and grow with the company. They will become our strong pillars.

Recently, we let go of a 40% stake in Duke-1 and Duke-2 to EPF for RM1.13bil. This will pave way for future partnerships.

We will do the same for future DUKEs and KL River City project. The funds obtained will be used to reward shareholders in the form of special dividend and finance new ventures.

(Ekovest has announced that it is distributing a special dividend to shareholders from the proceeds of its sale to EPF).

We have also set the target to become the top 30 listed companies on Bursa Malaysia within five years. This means that our market capitalisation has to hit RM10bil within five years, from the current RM2bil. It is achievable based on our growth.

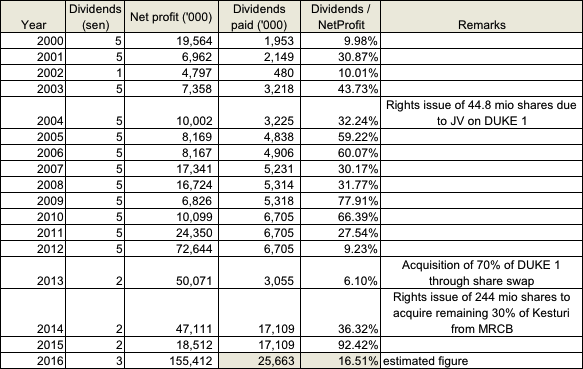

But while doing so, we must maintain our policy to give out dividends every year. Since 1993, we have been profitable. This is something we are proud of.

We also believe in doing CSR work. We have given Chong Hwa Independent High School a total of RM2mil and next year another RM1mil. For the Government’s SM Chong Hwa, we have given RM3mil.

How do you see Ekovest’s future financial performance?

We are doing very well. Our order book is very healthy, with total outstanding external order book of RM4.89bil as at November 2016.

For the current financial year, we won the biggest-ever project (DUKE-3) worth RM3.74bil, with a 50-year concession to collect tolls. That means our construction segment will be busy for the next three and a half years.

In November 2016, we have also been awarded two contracts to improve and beautify the Klang and Gombak rivers.

The results for the year ending June 2017 will be much better. You can see from our revenue growth. It’s almost doubled in 2016. There is also vast improvement in net profit. (Ekovest posted a revenue of RM794mil and net profit of RM155.4mil for the year ending June 2016, compared to a revenue of RM438mil and net profit of RM18.5mil in previous year).

Does the high-level connection of Tan Sri Lim help in any way to obtain projects?

Ekovest is run professionally.

Based on our technical expertise and our ability to see what people need, we won these public transport projects. There is no objection from people when our projects are displayed to gauge the public reaction. This is because our projects fill in the gap and we collect toll to help future projects.

It is not political connections that help us get jobs. We think out of the box using blue ocean strategy, hence, we came out with the master plan for DUKE highways.

If it was political link, we would have risen sky high long ago.

We will self-create and generate income. In DUKE, we carry out the planning and infrastructure for the government, create income for future highways.

Nowadays, it is impossible for you to bulldoze through projects. You need to do surveys and carry out public engagement. No one has objected to our DUKE highway projects so far.

What is your vision for Ekovest?

I want to create a sustainable city, not just high-rise only. I want to innovate to create value. I also want other people to learn from us when I give media interviews.