Analysts at TA Securities Holdings Bhd (TA Research) upgraded its earnings projection for AirAsia Bhd (AirAsia) following a drop in jet fuel prices.

According to the Singapore Jet Fuel Swaps – a jet fuel price indicator – jet fuel prices closed at its lowest level since November 2003. Year to date, it has resumed the fall by another 24.8 per cent to US$33.1 per barrel on Jan 22, 2016 following a drop of 38.4 per cent in 2015, mirroring the downtrend in crude oil price.

Accordingly, TA Research upgraded its financial year 2016 (FY16) to FY18 earnings projections for AirAsia by 1.9 to 8.9 per cent after the change in assumptions for jet fuel price to average at US$50 per barrel for 2016 to 2018 as compared with our previous forecasts of US$65 per barrel for 2016 to 2018.

This also includes a 90 per cent of cost reductions from lower jet fuel price assumptions to be passed on to passengers through lower airfares.

“Although we are only one month into 2016, we reckon that our jet fuel price assumptions of average US$65/bbl for 2016 could be overly bullish, as Iran’s oil exports, after the economic sanctions were lifted, are expected to accelerate the glut in the market,” the firm said in a report yesterday.

“As such, we are revising our jet fuel price assumptions lower in the advent of revised budget 2016 announcement, which the government is expected to trim its expenditure based on a more realistic oil price assumption.”

Meanwhile, TA Research called on investors not to “read too much” into the AirAsia privatisation.

The news about privatising AirAsia first came to the market in October 2015 and recently repeated by AirAsia X, citing that taking the carriers – both AirAsia and AirAsia x – private is an option but both AirAsia and AirAsia X have not received any offers.

“Again, we do not spend much time to look into it as we believe taking AirAsia, one of the world’s best low-cost airlines, private is not an easy task without roping in strategic investors like the Employee Provident Fund, who has a strong financial muscle, to assume the mounting liabilities that AirAsia currently has.

“We upgrade AirAsia’s target price to RM1.72 and upgrade to buy from sell.”

LANGKAWI: AirAsia aims to fly an additional three million passengers to Langkawi over the next five years.

This is on top of the current 1.6 million passengers it ferried in 2015 and in the face of potential demand for traffic to the holiday island.

Group chief executive officer Tan Sri Tony Fernandes said to achieve the target, the airline is looking at more international routes from and to Langkawi, including Hong Kong, Jakarta and Shanghai.

AirAsia today welcomed its inaugural flight from Guangzhou to Langkawi at the Kompleks Lang Merah, Langkawi International Airport.

The budget airline had announced during the LIMA Airshow in March last year that Langkawi would be its latest international hub in Malaysia.

“Our plan is to base five planes here and over the next five years, I believe AirAsia can reach five million passengers.

“We will continue to add to the passengers to Langkawi and Kedah,” he told reporters after the welcoming ceremony.

Prime Minister Datuk Seri Najib Tun Razak, Kedah Menteri Besar Datuk Seri Mukhriz Mahathir and Transport Minister Datuk Seri Liow Tiong Lai were also present to welcome the inaugural flight.

It landed with a healthy 92 per cent flight load.

Among the guests on board were representatives from the Guangdong Tourism Authority and members of the media.

AirAsia currently holds a 60 per cent market share in Langkawi air traffic in operating direct flights to Kuala Lumpur, Penang and Singapore.

Fernandes cited the Guangzhou-Langkawi route as not only strengthening the airlines’ presence on the island, but also further boosting its economy with potential investments from China.

“By making Langkawi an international hub, we are confident we can boost the tourism traffic to the island.

“We have invested substantially to ensure this hub can accommodate and facilitate our projected traffic growth and achieve the goal of turning Langkawi into a regional Low Cost Carrier (LCC) hub,” he said.

Fernandez said AirAsia had received an average booking of above 80 per cent for the commencement of the inaugural flight from Guangzhou, which indicates a boom in tourism for Langkawi in respect of Chinese tourists.

To celebrate the momentous occasion, the airline is offering an all-in-fare from as low as RM199 one-way from Langkawi to Guangzhou and from Jan 25 until Feb 7, 2016 for the travel period of Jan 25 to May 2, 2016. – Bernama

Tony Fernandes to deal in AirAsia shares

KUALA LUMPUR (Jan 27): AirAsia Bhd ( Valuation: 0.60, Fundamental: 0.20)'s group chief executive officer Tan Sri Tony Fernandes intends to deal in the company’s shares during the closed period prior to the release of its results for the fourth quarter ended Dec 31, 2015.

In a filing with Bursa Malaysia, budget airline AirAsia said Fernandes, also AirAsia’s non-independent executive director, owned 530.14 million shares or 19.05% in the company.

AirAsia said the 19.05% stake comprised a 0.06% direct portion and an 18.99% indirect interest.

Fernandes' indirect 18.99% interest in AirAsia is held via Tune Air Sdn Bhd, according to AirAsia. His direct stake in AirAsia is held under CIMB Group Nominees (Tempatan) Sdn Bhd.

At 11:01am, AirAsia shares rose two sen or 1.5% to RM1.34, for a market capitalisation of RM3.73 billion.

The stock saw some four million shares transacted.

AirAsia's share price compares to the company's latest reported net assets per share at RM1.37. (Note: The Edge Research's fundamental score reflects a company’s profitability and balance sheet strength, calculated based on historical numbers. The valuation score determines if a stock is attractively valued or not, also based on historical numbers. A score of 3 suggests strong fundamentals and attractive valuations.)

http://www.theedgemarkets.com/my/article/tony-fernandes-deal-airasia-shares

Soros: China Hard Landing Is Practically Unavoidable

Billionaire investor George Soros said China’s economy is headed for a hard landing, a slump that will worsen global deflationary pressures, drag down stocks and boost U.S. government bonds.

"A hard landing is practically unavoidable," he said in an interview with Bloomberg Television’s Francine Lacqua from the World Economic Forum in Davos on Thursday. "I’m not expecting it, I’m observing it.”

Soros, who built a $24 billion fortune through savvy wagers on markets, said he’s been betting against the Standard & Poor’s 500 Index, commodity-producing countries and Asian currencies, while buying Treasuries. China’s economic downturn will have spillover effects on the rest of the world, even though the nation’s policy makers have resources to manage the domestic fallout, he said.

The former hedge fund manager turned philanthropist joined a chorus of top investors -- including DoubleLine Capital’s Jeffrey Gundlach and Scott Minerd of Guggenheim Partners -- warning of further downside in riskier assets after a selloff that erased $16 trillion from global equities since June and sent commodities to the lowest levels in more than two decades. Concerns over China have roiled global markets this year amid waning investor confidence in the government’s ability to restructure the economy without a crisis.

Past Record

Hungarian-born Soros rose to fame as the manager who broke the Bank of England in 1992, netting $1 billion with a bet that the U.K. would be forced to devalue the pound. He also successfully bet that Germany’s mark would rise after the collapse of the Berlin Wall in 1989 and that Japanese stocks would start to fall in the same year. Soros, who began his career in New York City in the 1950s, led his hedge fund to average annual gains of about 20 percent from 1969 to 2011, when he returned money back to investors.

More recently, he has repeatedly warned of a 2008-like catastrophe. On a panel in Washington in September 2011, he said the Greece-born European debt crunch was “more serious than the crisis of 2008.” He reiterated that idea earlier this month, saying that global markets are facing a crisis reminiscent of the one more than seven years ago.

Deflation Risk

While Soros didn’t elaborate on his definition of a hard landing, he said a more accurate measure of China’s current economic growth is 3.5 percent, versus the latest official figures showing a 6.8 percent expansion in the fourth quarter. He added that the country’s unsustainable debt burden and capital flight are both signals of a hard landing. China had about $843 billion of capital outflows in the 11 months through November, according to a Bloomberg Intelligence estimate.

China’s slowdown is combining with lower oil prices and competitive currency devaluations to increase the risk of deflation around the world, Soros said. That will make 2016 a “difficult” year for markets because it’s a scenario investors aren’t used to, he said. Consumer prices in the U.S. declined 0.1 percent in December, while factory-gate prices in China have dropped for a record 46 consecutive months.

Soros said he would be surprised if the Federal Reserve raised interest rates again after increasing them in December for the first time in almost a decade, despite the central bank’s projection for further hikes this year. The Fed made a mistake in lifting rates when it did, he said, because deflationary expectations had already set in and consumers were less likely to respond to lower borrowing costs with increased spending.

Classic Bottom

Not everyone has such a bearish view. Investors are probably overstating the impact of China’s slowdown on the rest of the world and the economy is likely to avoid a hard landing this year, according to Goldman Sachs Private Wealth Management. Heather Arnold, who overseas about $42 billion as a money manager and director of research at Templeton Global Advisors Ltd., said in an interview in Tokyo this week that China shouldn’t be a big concern for global investors and she’s been boosting stock holdings.

“The depth of pessimism that’s out there seems unwarranted,” Arnold said.

U.S. stocks rebounded from the lowest levels in 21 months on Thursday, with the rally carrying through to Asian markets on Friday. The MSCI Asia Pacific Index climbed 2.4 percent at 10:32 a.m., while oil prices advanced and Malaysia’s ringgit led gains in emerging-market currencies. The Shanghai Composite Index increased 0.3 percent.

While asset prices may post a short-term rallies, Soros said, he hasn’t seen signs of a “classic bottom” in markets. It’s too early to buy, he said.

“This year is going to be a difficult year, and the balance is on the downside,” Soros said. “If you have a real bottom, it’s always retested.”

By MIDF Research / The Edge Financial Daily | January 21, 2016 : 10:29 AM MYT

This article first appeared in The Edge Financial Daily, on January 21, 2016.

AirAsia X Bhd (Jan 20, 19.5 sen) Maintain buy with an unchanged target price of 26 sen: The management’s optimism is not without basis. AirAsia X Bhd (AAX) chief executive officer (CEO) Benyamin Ismail and team hosted sell-side analysts to a financial year 16 (FY16) outlook briefing at their office at the low-cost carrier terminal recently. We were also fortunate enough to chance upon Datuk Kamarudin Meranun (group CEO), who explained to us that he and the board of directors feel that AAX would perform fairly better in 2016 with internal stress testing and number-crunching pointing to operating profit. Overall, I left the meeting feeling upbeat on AAX’s prospects. We believe that fourth quarter ended Dec 31, 2015 (4Q15) results could be in the black at net operating income (NOI) level on the back of 1) higher yields (revenue per unit) due to more rational pricing; 2) improved load factors (utilisation rate) due to seasonality and lower industry capacity; and 3) lower average spot jet kerosene price, which according to our calculations, would average at US$56 (RM244.72) per barrel (bbl; down 39% year-on-year [y-o-y]). While profitable at NOI level, the main deterrent to a positive profit after tax (PAT) remains its interest expenses, which would be higher due to the higher average US dollar/ringgit of +27% y-o-y. Nonetheless, we believe that AAX’s 4QFY15 results will likely break even at PAT level. On the issue of potential threats by Malindo, which is expanding its network to medium- to long-haul destinations such as Australia and China, the management believes that AAX remains ahead of the competition. AAX flies Airbus A330 wide-body aircraft against Malindo’s Boeing 737 narrow-body. The bigger aircraft offers advantages such as higher operating efficiency and comfort to passengers while pricing its fares lower. Moreover, Malindo could find itself in Malaysia Airlines Bhd’s cross hairs or vice versa as Malindo positions itself more as a full-service airline. AAX will be able to reap the benefits of lower jet fuel prices in 2016 as it has currently hedged 50% of its 2016 requirements at US$60/bbl, which is -32% lower than its 2015 hedge at US$88/bbl. Meanwhile, spot jet kerosene is trading at US$40/bbl, which is -38% lower than the 2015 average of US$65/bbl. On a blended average basis, if jet kerosene prices were to remain at current levels for the remainder of the year, AAX would enjoy fuel cost savings of -35%, paying US$50/bbl compared with 2015’s US$77/bbl. Meanwhile, we expect the weaker ringgit to be cushioned by natural hedges as 75% US dollar-denominated cost is hedged against 70% foreign-currency revenue (mainly US dollar and Australian dollar). Our “buy” call is premised on AAX: 1) benefiting from lower fuel hedges in FY16; 2) improving yields and load factors from industry capacity cuts and less competitive pricing; and 3) compelling valuations, trading at only 7.7 times and four times FY16 and FY17 earnings per share respectively. — MIDF Research, Jan 20

"Sell everything" is the startling new advice from The Royal Bank of Scotland - warning its clients to brace for a "cataclysmic year." No one can blame you if you're one of the many investors who is worried right now... Not when CNN is proclaiming that this "global market freakout" is spreading...Canada's officially in a bear market (stocks down more than 20%)...things have gotten so bad in China that officials keep shutting down the market to keep it from falling any further.

And now this "freakout" is hitting close to home - the U.S. markets are off to the worst four day start to a year...ever.

Yes, danger is lurking out there, but brave investors have built enormous fortunes during the worst markets. J Paul Getty became the richest man in the world by buying oil stocks during the Great Depression...and John Paulson reportedly made a mind-boggling $3.7 billion during the largest stock-market crash this century.

And now this crashing market is offering brave investors like you another potentially historic buying opportunity. The way to profit is surprisingly simple...

How to Thrive in Crashing Markets Warren Buffett is the world's most successful investor, and his most famous motto is perfect for making money AT TIMES JUST LIKE NOW.

Buffett's genius solution is as simple as it is effective: "Be Fearful When Others Are Greedy and Greedy When Others Are Fearful"

Well, let me ask you... What are you hearing when you turn on the tv? What are you reading in the newspaper? What are your friends telling you? Does it seem like people are afraid?

Because if others are afraid, I think it's time to start being greedy - by using an investing system that proved itself during the biggest stock market crash of this century. This system's performance was so remarkable that the Wall Street Journal reported that the newsletter was ranked #1 in the world for a five-year period that included the worst stock-market crash since the Great Depression.*

Today is your chance to take advantage of the amazing opportunities this system has uncovered.

Profiting during a market crash can often require two things: The courage to be greedy when others are fearful A system with a long track record of not just surviving, but thriving through market cycles.

I can't give you the courage to act - that's up to you - but if you decide that you are the kind of person who can take advantage of these potentially amazing buying opportunities... I can give you inside access to the recommendations provided by this system - a system which has shown a remarkable ability to succeed through even the worst markets.

Remember, history teaches us that the terrified investors running for the exits will eventually come to their senses - once that happens this amazing opportunity could be gone

I like felicity articles, they are good

I have some comments from a reader which I will try to answer:

felicity, I benefited from reading your blog articles, so here's my take on AirAsia.

1. Look at their free cash flow http://www.marketwatch.com/investing/stock/airasia/financials/cash-flow Taking a long-term perspective, return to shareholders is simply discounted sum of free cash flow. Profit is an opinion, cash is real.

I have been a proponent of free cashflow in my blog and did I change my strategy and investment methods. No. It is accurate that Airasia has not been strong in its cashflow department over the last few years but if one is to read further, Airasia has been on growth path before and they have actually slowed down their growth since 2015. For 2015, one will see a net free cashflow of more than RM1 billion and that is before they have started to fully enjoy the much lower fuel price. Most airlines (except for many American airlines) had yet to enjoy the lower fuel costs. 2016 will be year where the lower fuel will start to provide the additional profits. Airasia's business generates real cash.

2. AirAsia has over $11B ringgit in debt. http://www.airasia.com/my/en/about-us/ir-5-year-financial-highlights.page Sure, they have plenty of planes. But planes can't be sold otherwise, they would have to close shop. Even if they reduce their planes, they probably won't get a good price (see point 3).

Debt is definitely high. They have to work on it before it becomes overly burdensome. However, they are not in the business of selling planes but seats. Most tend to think what if it closes down. It is a business. They do sell old planes and buy new ones. On that part the narrow body planes are much better situation than wide body planes. Example A380 or B777 will have problem to be sold, not so A320.

3. There is a overcapacity in the airlines industry currently (as MAS's new CEO pointed out during a recent interview).

Wonder why you think AirAsia should be worth US$10B someday? Did you do a discounted free cash flow analysis or just compared them to valuations of other budget carriers?

I am the bullish one of course and most analysts provide a higher valuation than its current price. I myself think it should be higher, but of course its my opinion. Analysts tend to take the safe way out as by putting a much higher price, they are taking risk of being considered irrational. I can be irrational. If I think Airasia is worth $2 billion then for it to reach $10 billion is a multiple of 5x. I also do not think dollar will be 4.3x RM in the long run, hence valuation of say RM35billion does not sound too expensive anymore. But of course, many would think I am crazy as Airasia is only priced at RM3.7 billion today. That's 10-20 years down the road. If one is to look at the trajectory of successful and top low costs carrier, Ryanair, Easyjet and Southwest, they have that kind of trajectory over 15 years especially during growth to maturity period.

Today LCC are competitive (even have RayaniAir - hmmm sounds like RyanAir isn't it) but small ones will fizzle out. I am always the proponent of full fledged low costs - not the Singapore model such as Tiger and Scoot where they are owned by SIA. It is hard to have 2 models unless they are independent. I also like the management of Airasia (many will not agree with me) as they are positioned to be successful and grow. Some of the LCCs are positioned to be "jaguh kampung". Airasia is not although they do face huge challenges as we see it when moving overseas. Thailand though is one success story.

I however think SIA's subsidiaries like Tiger will give Airasia a run for their money overtime as SIA is a bigger parent than Airasia has. (Singapore by the country is also more focus, unlike Malaysia whom is trying to kill Airasia and in the process, affecting its own tourism business. I hope overtime they will realise that a strong LCC would bring benefit to the country especially when forex is important to Malaysia)

Also note that as it is Tiger being valued more than SGD1 billion is a sign than a struggling low costs such as Tiger is worth something and not as per what Airasia is valued at today. Check news on SIA's offer for Tiger!

On having a DCF, it is preposterous as DCF model can be out of whack easily. Nobody can predict the cashflow future correctly. These are meant for financial people whom only uses excel well.

On overcapacity, its real and the one who blink first is MAS, right? Them cutting capacity brought some benefits to Airasia and other airlines like Emirates. The data is already been provided by Malaysia Airport whom reports on traffic monthly. The traffic since MAS had its cut brought traffic to KLIA2 significantly. Airasia is by far the biggest user of KLIA2.

In the long run, both LCC and full fledged will see competitions but the next decade will be decade for LCC than the one MAS, Emirates are focusing on. SIA (and I trust the data crunching from Singapore) has already foreseen that. I am seeing also that Airasia is in right position and will be there to ride the wave, But it has to be diligent and careful.

When I bought this low costs airline at RM1.12, many thought I was crazy. It is a difficult sector - I agree. Warren Buffett said no, where many American airline companies went bankrupt before. Many Asian airlines went bankrupt as well and needed rescue by their government. Among them Japan Airlines, Thai Airways, Qantas (in trouble) and of course every now and then MAS had that problem and it may not just end.

Why? Because these are national airline companies and (as I have mentioned before), no country would allow their national airlines to be taken off the sky. That was how it was deemed before. Today, many countries still support their national airline, but that thought of supporting the national airline company - at all costs - is being less considered or shall I say is less important.

I would consider having an airline company to a country as like a country having a football team. No country that is able, would not NOT have a national football team - and believe me except for several very strong national teams, for most countries, these are a costly affair. One cannot however say due to this, we should not have a national football team. This is also why the current suspended FIFA president, Sepp Blatter has been in power for 5 terms. He knows what a poor country needs and through FIFA's financial strength, he supports them albeit the many corruption scandals as well.

Back to airline So when all these countries fight, in a competitive world, most cases there is 1, 2 or at best 3 winners while all the rests would lose - badly. Until 10 years ago, in this region these winners were SIA, to some extent Cathay. The rest were losers that went bankrupt and relived through government rescue. Then came airlines from oil rich countries whom have nothing else to do but to continue throwing oil revenues into their own airlines. These countries supported Emirates, Qatar, Etihad and had seemingly unlimited cash so much so it seems that they are the one until today whom are supporting the Airbus 380 initiative. Without them and originally SIA, A380 would never had gone off the tarmac.

About 20 to 30 years ago, it was also the time where low costs airlines just about were getting traction. First, it was Southwest (in US), in the process killing several full-service airlines in US indirectly. Then of course were Ryanair and Easyjet in Europe. These airlines thrive on deregulation of the air passenger business in their own country (for Southwest) and continent (for Ryanair and Easyjet). If you study, how would an Irish based company (Ryanair) and a Texas based company (Southwest) thrive against competition which are based from higher traffic cities such as New York, Los Angeles, London, Rome, Paris etc? Where they are operated from, these are not the most high traffic places.

These low costs airlines do not follow the usual (past) airline business convention. To be able to compete on price and other means such as efficiency is their business model, with the main intention to carry people point to point - at very affordable price. Prices which were unimaginable, are now possible for mass public to be transported. It is not that we are better off that we are able to fly more often. Our ability to fly is due to there is a big shift in how this sector has changed. Flying should not be a luxury anymore.

Back to Airasia Where Airasia is operating and competing and driving, it is the same as where Ryanair has been so controversially despised by many of their customers, partners etc. But think about it, they revived many of the smaller or older airports, making commuting easier and faster. Of course, at the same time, making themselves very rich. (Micheal O'Leary, Ryanair's brash CEO is one of the richest person in Ireland). You can also see that Airasia sort of made Malaysia Airport what it is today - that's why Tony Fernandes is furious with KLIA2 and KKIA more recently.

Companies such as Airasia and Ryanair of course changed the landscape of the airline business, pushing hard for deregulation - an area where they will thrive. Of course, Airasia is still fighting hard against MAS in Malaysia, Thai Airways in Thailand, Garuda in Indonesia and many other countries. But their business model is different, so much so that sometimes these airlines do not know how to react - to a low costs competitor. For MAS (where they had done), it cannot afford to compete on prices relying on the operational platform they are in. When it competed on prices, it lost more than RM1 billion in 2014, injuring Airasia as well. In the end, it was MAS whom surrendered first, although Airasia was also badly hurt. Think about it, should it not be a private company that is more seriously hurt competing against a government behemoth?

Ironically from there, Khazanah appointed Christoph Muller. In his resume, he was acclaimed as the turnaround specialist whom made it happened for Aer Lingus, the national Irish airline. He is expected to do the same for MAS.

No article in Malaysia carries his work in Ireland and mentioned whom he was up against. The fact is, he was against Ryanair. He did not really try to compete head-on with Ryanair as I would think he knows he would have lost. As in what we have seen in Malaysia where has been trying to do onto MAS, he made Aer Lingus more agile and smaller - and focus on what a full-service airline would do.

As in most turnaround stories, a person is considered successful if he is able to do complete the turning around, but in most cases, the winner is still your competitor - Ryanair in his case. He did not make Aer Lingus very profitable. Aer Lingus stopped bleeding - and that's success. I am expecting the same to happen in Malaysia. MAS would go smaller, while Airasia will be the one transporting more Malaysians. In Ireland that is the same, so much so that Micheal O'Leary would argue that Ryanair should be the national airline of Ireland rather than Aer Lingus as they transport more Irish than the flag carrier.

Where Airasia has gone regional

We have also seen Airasia is not just a carrier whom are operating off Malaysia. It is going after the regional business, much more difficult but needed. Why?

Flying in most part of Asia, it is not about inter cities within the same country but also between countries. In this sense, Airasia should seek to expand (as it already does) as it does not carry the baggage of a national airline where in Asia especially is a no no for one country's airline to be doing well in other people's country. It is much harder for SIA to propose holding stakes in another country's airline company as compared to Airasia, I would think - although SIA does own stakes in some other Asian countries. For SIA I would think, it is their national duty to bring more traffic into their own country rather than making strategic investments in another country's airline. That is also probably why SIA has offered Tiger Airways shareholders and making the Singapore based low costs airline go private. There must be strategic reasons from this and I am speculating that, the future growth of the business is low costs.

For Airasia, as it is going into many other countries such as Thailand at first, Indonesia, Japan, Philippines, India - it is not without challenges. In each of these countries there are already their incumbent. These are Lion Air, CebuAir, Indigo etc. and they are probably given preference by their own government. This is also why Airasia, as you have seen are facing countless challenges - but these are challenges it must overcome and learn from mistakes.

What investors today is expecting is Airasia to be profitable immediately from these ventures - so much so that there are negative valuations provided for these overseas investments. In actual fact, it should not be. If Airasia's venture is to be valued individually in their respective countries, there would be different value provided added up for Airasia as a group.

The fact is the international investments is pulling Airasia's value down as a whole. Are we saying that Airasia should stop holding stakes beyond Malaysia? Is we say no, that's what today's valuation is however telling us. (as an analyst, we are taught sum of parts - where we break up individual business or investment and value them separately. After that, we will tally them up into one valuation for the group. No analyst has done that for Airasia. If I were to ask to have the exercise differently, just value Airasia's Malaysian operation, what should be the value?)

Today, Airasia is being priced at below RM4 billion - i.e. not even USD1 billion. For the first ever low costs airline in Asia and how much it has done to achieve to where it is today, do you think it is worth less than USD1 billion? Of course, no PE ratio or dividend yield or even NTA would have provided a good valuation threshold. This is because Airasia is continuing to invest in overseas where it will create negative valuation to the group as a whole. People is putting huge value on hope and based on aggressive investments into Amazon and Alibaba (and Lazada, Snapdeal) - all e-commerce - for example but not on hope for a low costs airline business where there is also tremendous growth opportunities as well.

What Airasia needs to do is continue to push and survive during bad times while it grows in times - like now - where low oil price is beneficial for all airlines. If it wins in Asia (that means largest low costs airline in Asia), I am sure it will be a USD10 billion company in 10 or 20 years time - where I see a more open Asian skies. --------------------------------------------------------------------------------------------------------------

Airasia's results seems about right although I expected its operating profit to be better due to the downsizing of its main competitor - MAS and lower oil price. Anyone that has a quick look at the results would be shocked as it reported a net loss of RM406 million. However, before one trembles, take a look at what caused these losses. It absorbed RM625 million in losses mainly due to the conversion of Indonesia Airasia's owings into shares - to reverse the negative shareholders funds as required by the regulators in Indonesia. This shall I say is already expected and announced.

3Q15 Income Statement

However, what's exciting and as happened to most of the other airlines is that the low oil price is now allowing them to really make money despite the stiff competition. For the quarter, Airasia achieved a RM166 million Net operating profit. If you looked at the poor Ringgit strength, it seems that its forex losses seems to be cancelled by the gain from amount due from associates and jointly owned entities. It however hit them harder on the finance costs as lower Ringgit may costs them higher interest payment.

What's key in the results

One of the things that's noticeable is the challenges it faces in the newer markets that it has gone to - Indonesia, Philippines and India. As a result, do not expect these new ventures especially India and Japan to be profitable fast.

Airasia has also started to publish results for all its markets and provide its consolidated report. Notice the low right number of RM64.91 million...That's consolidated number in the event it is assumed as it has control over those companies.

Another point to note is that with oil price at around USD42- 45 per barrel, there is still room for Airasia to enjoy better margin due to low fuel price. For the quarter, its average price was USD77. I would expect it to be below USD 60 by 2016. Most airlines have hedged a significant part of their fuel causing them to still buy fuel at higher than spot prices. Most of them has lessen their hedges for 2016. (Notice that fuel still comprise of 38% of the total costs, hence making it the single highest costs element for Airasia and in fact for all other airlines)

All in all, while most may just be looking for a single headline, as shown below, if we look deeper, there are many positives especially for one of the largest airline in Asia and with such a deep discounted price.

Air Asia plunged to around RM0.80 range during its worst period last year, with perfect storm of Airplane crashing in Indonesia, Indon air control asking for Capital topup, and also the unexpected audit report from HK.

But, crude oil plunge further to current USD28 is a BIG positive to me.

I especially like felicity articles on Asia's budget flight and the prospects. I expected it to be one of the booming sector next 10 years and Air Asia stand a good position to become largest here.

My TP set was RM2 level, then longer term around RM3.50-4.00 if expansion in India, Japan, China, HK were to be successful.

WEAKNESS-the only weakness I think will be the many unexpected events such as crash, sudden spike in crude oil fuel price, and also their HIGH debts denominated in USD, thought they are longterm bonds. (Good thing they had launch USD1Bil funding).

Read research as below:

Aviation - Year 2016 – Recovery in Air Travel

Highlights

We expect a gradual demand recovery for air travel in 2016 benefitting MAHB and AirAsia:- 1) Foreigner: Government is stepping up efforts in promoting Malaysia tourists destinations with a huge allocated budget of RM1.2bn for 2016 (vs. RM316m in 2015). Malaysia targets for 30.5m tourist arrivals (vs. 27.4m in 2014). 2) Malaysian: Gradually adjusting to the increasing cost of living and RM depreciation since 2015, increasing number of Malaysian will resume their travelling passion with adjusted budget in 2016.

In 2016, better structured capacity addition is expected to match the gradual recovery in ai r travel demand. Post capacity rationalization exercise in 2015, MAS will be more focused in expanding its domestic and regional networks, integrating with long-hauls (code-sharing), while AirAsia is also working towards equitable supply-demand growth.

With the drastic capacity cut in the system (by MAS) in 2015 and reasonable planned supply-demand structure in 2016, we expect continued yields improvement in 2016, benefitting airlines (i.e. – AirAsia, AirAsia X and MAS).

Jet fuel price has slumped further in 2015 to US$45/bbl and expected to stay low in 2016. The low jet fuel price will improve ai rlines profitability. AirAsia is expected to be the major beneficiary (jet fuel contributed 40-60% to airlines cost structure) of low oil price environment. AirAsia only hedged 41% of 2016 jet fuel requirement at US$63/bbl.

The depreciation of RM impact:- 1) MAHB: Positive impact from the higher translated earnings contribution of wholly owned ISGA in EU€. 2) AirAsia: Negative impact from higher translated cost structure (jet fuel, maintenance and debts) denominated in US$ (+18% YTD). However, the negative impact only partially offset the benefits from the slump in jet fuel costs (-35% YTD).

Risks

World crisis (i.e. war, tourism and epidemic outbreak), delay in KLIA2 completion, high jet fuel price and the development of high speed train between Singapore and Pulau Pinang.

Forecasts

Unchanged.

Rating

OVERWEIGHT

Positives

Low Jet fuel price.

Liberalization of ASEAN open sky policy.

Increased government budget to RM1.2bn for tourism.

Negatives

Ringgit depreciated against US$.

Negatives consumer sentiments – Air Incidents and GST.

Valuation

Maintained BUY on MAHB with unchanged target price of RM6.30 based on DCFE.

Maintained BUY on AirAsia with unchanged target price of RM2.00 based on SOP.

----------------------------------------------------------------------------------

Also, felicity studies on Budget Airline was master piece.

I am wary of the fear in investing into an airline given the past experiences of many collapses - and Malaysia Airlines has been our closest example. Thai Airways did not fare well either. The list goes on and on. But those are the traditional airlines and their possible collapse could be due to the proliferation of low costs model. Airasia's drop however warrant me to look deeper into the company as I feel that it is managed by people who are capable.

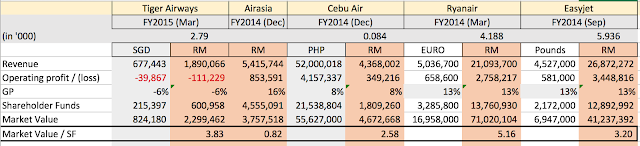

Let's look at comparison of Airasia's successful peers (except for Tiger) than look at the non-performing ones. I have taken some examples of Ryanair, Easyjet, Cebu Air (Airasia's top furious competitor in Philippines) and Tiger Airways. Why did I chose those?

Ryanair - model low costs airline operating only in Europe Easyjet - second to Ryanair and hugely successful as well Cebu Air - as mentioned, Airasia's top competitor in Philippines. It is dominant there and Airasia is having a tough competitor. But it is predominantly a Philippines airline. Tiger - well, nearest financially available competitor to Airasia. Not very successful and it needed injection of capital last year.

The significant names that are not here - Southwest (largest low costs in the world and operating only in US) and Lion Air (not listed). I did not pick up Southwest because over the last year, non-US airlines have suffered from the appreciation of US Dollar but benefited from the huge drop in oil price. US Dollar of course appreciated against many currencies and Malaysian Ringgit suffered the most. However, if one is to believe that USD could not appreciate much further, this forex losses will stop. No single currency will appreciate the way USD appreciated in the last few months and continue to appreciate. Think of what the consequences would be to US economy if that happens.

Anyway on the numbers, I have picked up revenue operating gain / loss, GP and shareholders funds. Why I did not use Net Profit is due to the forex loss that some of the companies experienced including Airasia which I do not think will be a long term thing. Fundamentally it is how well the company manages the gross margin as well as the fuel hedges.

The accounting policy for foreign exchange for Airasia is as below.

Comparison

As below are the important numbers for the list of companies.

Airasia's of course is the Malaysian operation only where it can consolidate the numbers. Others are based on equity accounting. While one can understand that Airasia's balance sheet is not that strong as compared to its stronger peers like RyanAir and Easyjet, I do not think that it is cashflow starved. One should note that Airasia's business model is to collect cash upfront and pay later. There is a period where it is benefiting from customer financing and that business model is great especially if applied to one's advantage. Airasia, to some extent have managed to use that to its advantage.

And based on its market value to its book value, would it be a reason to buy? Personally, I would say yes, especially for an airline which is still growing. There should be continuous competition but gone are the days where "everyone wants to own a low costs airline" as the barriers of entry is getting much much tougher.

Remember, the stock market in the short run is a voting machine, but in the long term is a weighing machine. What's substance is more important. Think of Airasia's substance.

Valuation: 0.60, Fundamental: 0.20)'s group chief executive officer Tan Sri Tony Fernandes intends to deal in the company’s shares during the closed period prior to the release of its results for the fourth quarter ended Dec 31, 2015.

Valuation: 0.60, Fundamental: 0.20)'s group chief executive officer Tan Sri Tony Fernandes intends to deal in the company’s shares during the closed period prior to the release of its results for the fourth quarter ended Dec 31, 2015.

浅谈贵股的春天:

浅谈贵股的春天: