| International Financial Statistics, April 2016* | |||||||

Tonnes

|

% of reserves**

|

Tonnes

|

% of reserves**

| ||||

1

|

United States

|

8,133.5

|

75.3%

|

51

|

WAEMU3)

|

36.5

|

11.8%

|

2

|

Germany

|

3,381.0

|

69.0%

|

52

|

Malaysia

|

36.4

|

1.5%

|

3

|

IMF

|

2,814.0

|

1)

|

53

|

Peru

|

34.7

|

2.2%

|

4

|

Italy

|

2,451.8

|

68.3%

|

54

|

Slovakia

|

31.7

|

41.9%

|

5

|

France

|

2,435.6

|

63.2%

|

55

|

Azerbaijan

|

30.2

|

18.4%

|

6

|

China

|

1,788.4

|

2.2%

|

56

|

Ukraine

|

27.4

|

8.1%

|

7

|

Russia

|

1,447.0

|

15.1%

|

57

|

Syria

|

25.8

|

5.8%

|

8

|

Switzerland

|

1,040.0

|

6.8%

|

58

|

Sri Lanka

|

22.1

|

13.4%

|

9

|

Japan

|

765.2

|

2.4%

|

59

|

Morocco

|

22.0

|

3.7%

|

10

|

Netherlands

|

612.5

|

59.4%

|

60

|

Afghanistan

|

21.9

|

12.2%

|

11

|

India

|

557.7

|

6.2%

|

61

|

Nigeria

|

21.4

|

2.6%

|

12

|

ECB

|

504.8

|

26.6%

|

62

|

Serbia

|

18.1

|

6.5%

|

13

|

Turkey6)

|

479.4

|

16.9%

|

63

|

Cyprus

|

13.9

|

63.2%

|

14

|

Taiwan

|

422.7

|

3.8%

|

64

|

Bangladesh

|

13.8

|

1.9%

|

15

|

Portugal

|

382.5

|

72.1%

|

65

|

Tajikistan

|

12.6

|

88.6%

|

16

|

Venezuela

|

361.0

|

69.1%

|

66

|

Cambodia

|

12.4

|

6.5%

|

17

|

Saudi Arabia

|

322.9

|

2.1%

|

67

|

Qatar

|

12.4

|

1.3%

|

18

|

United Kingdom

|

310.3

|

9.3%

|

68

|

Ecuador

|

11.8

|

14.4%

|

19

|

Lebanon

|

286.8

|

22.7%

|

69

|

Mauritius

|

9.9

|

8.9%

|

20

|

Spain

|

281.6

|

19.9%

|

70

|

Czech Republic

|

9.9

|

0.6%

|

21

|

Austria

|

280.0

|

46.5%

|

71

|

Ghana

|

8.7

|

7.6%

|

22

|

Belgium

|

227.4

|

36.8%

|

72

|

Paraguay

|

8.2

|

5.4%

|

23

|

Kazakhstan

|

225.6

|

32.3%

|

73

|

United Arab Emirates

|

7.4

|

0.4%

|

24

|

Philippines

|

195.9

|

9.6%

|

74

|

Myanmar

|

7.3

|

3.9%

|

25

|

Algeria

|

173.6

|

4.5%

|

75

|

Guatemala

|

6.9

|

3.6%

|

26

|

Thailand

|

152.4

|

3.6%

|

76

|

Macedonia

|

6.8

|

10.9%

|

27

|

Singapore

|

127.4

|

2.0%

|

77

|

Tunisia

|

6.8

|

3.6%

|

28

|

Sweden

|

125.7

|

8.4%

|

78

|

Latvia

|

6.6

|

7.3%

|

29

|

South Africa

|

125.2

|

10.9%

|

79

|

Ireland

|

6.0

|

8.0%

|

30

|

Mexico

|

121.2

|

2.7%

|

80

|

Lithuania

|

5.8

|

18.2%

|

31

|

Libya

|

116.6

|

5.8%

|

81

|

Nepal

|

4.9

|

3.0%

|

32

|

Greece

|

112.7

|

63.5%

|

82

|

Bahrain

|

4.7

|

3.1%

|

33

|

BIS2)

|

108.0

|

1)

|

83

|

Brunei Darussalam

|

4.5

|

5.3%

|

34

|

Korea

|

104.4

|

1.1%

|

84

|

Kyrgyz Republic

|

4.3

|

9.5%

|

35

|

Romania

|

103.7

|

10.9%

|

85

|

Colombia

|

3.5

|

0.3%

|

36

|

Poland

|

102.9

|

4.3%

|

86

|

Mozambique

|

3.4

|

5.6%

|

37

|

Iraq

|

89.8

|

6.5%

|

87

|

Slovenia

|

3.2

|

13.5%

|

38

|

Australia

|

79.9

|

7.3%

|

88

|

Aruba

|

3.1

|

14.1%

|

39

|

Kuwait

|

79.0

|

9.5%

|

89

|

Hungary

|

3.1

|

0.4%

|

40

|

Indonesia

|

78.1

|

3.0%

|

90

|

Bosnia and Herzegovina

|

3.0

|

2.5%

|

41

|

Egypt

|

75.6

|

18.4%

|

91

|

Luxembourg

|

2.2

|

8.3%

|

42

|

Brazil

|

67.2

|

0.7%

|

92

|

Hong Kong

|

2.1

|

0.0%

|

43

|

Denmark

|

66.5

|

4.1%

|

93

|

Iceland

|

2.0

|

1.4%

|

44

|

Pakistan

|

64.5

|

13.0%

|

94

|

Papua New Guinea

|

2.0

|

4.4%

|

45

|

Argentina

|

61.7

|

8.6%

|

95

|

Trinidad and Tobago

|

1.9

|

0.7%

|

46

|

Finland

|

49.1

|

18.8%

|

96

|

Haiti

|

1.8

|

3.6%

|

47

|

Belarus4)

|

42.9

|

40.6%

|

97

|

Albania

|

1.6

|

2.0%

|

48

|

Bolivia

|

42.5

|

13.2%

|

98

|

Yemen

|

1.6

|

1.2%

|

49

|

Jordan

|

41.4

|

9.9%

|

99

|

Mongolia

|

1.6

|

5.1%

|

50

|

Bulgaria

|

40.2

|

7.4%

|

100

|

El Salvador

|

1.4

|

1.7%

|

Tuesday, April 26, 2016

WORLD OFFICIAL GOLD HOLDINGS

Silver’s on Fire

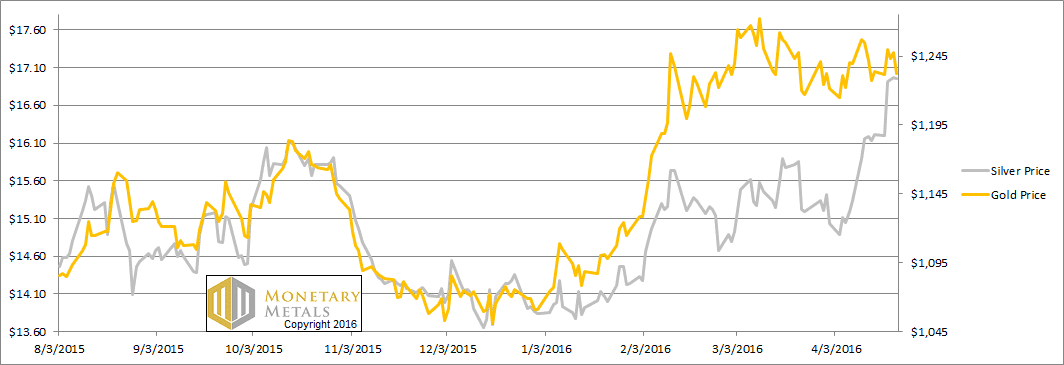

Another interesting week, in that the price of silver separated from the price of gold. The former went no nowhere, while the latter gained over 4.5%.

We get the trading thesis, that if the precious metals are in a bull market, then silver should go up more than gold. Silver is the high-beta gold. It’s a smaller market, less liquid, and at the same time it’s the preferred vehicle for betting on a rising price.

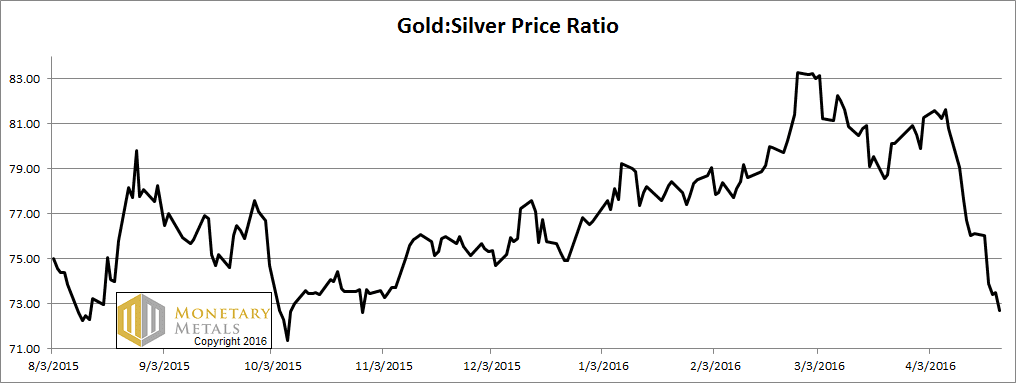

We don’t quite get the thesis that gold is going nowhere or even down, and bet on silver which is going to $50. Yet that is now our market reality. Excited silver bulls have watched as pushed silver up from $14 in late January to $17. Meanwhile the price of gold went from $1,100 to $1,260 and then back down to $1,230. The gold silver ratio initially rose from 78.5 to over 83, and down so far to 72.7.

The growing consensus is bullish. As always, we’re more interested in the fundamentals than in opinions. Let’s look at the only true picture of supply and demand fundamentals. But first, here’s the graph of the metals’ prices.

The Prices of Gold and Silver

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. The ratio was down sharply again this week.

The Ratio of the Gold Price to the Silver Price

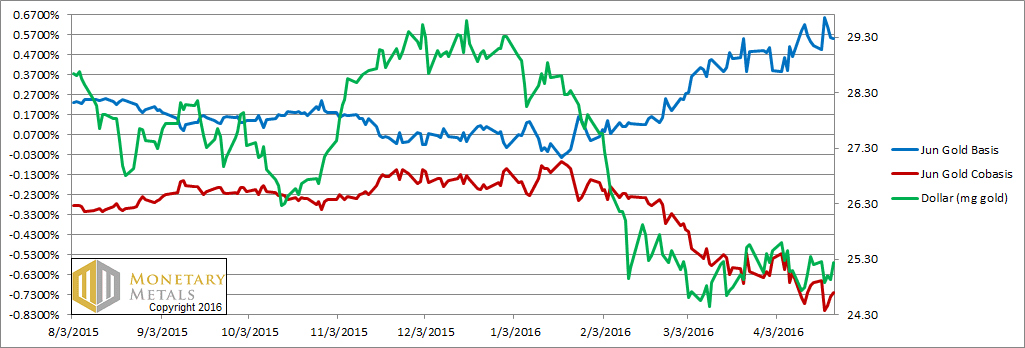

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

Look at that. Carrying gold for June delivery is now even more profitable, over 55 basis points. This is up from last week at 51bps. The increase tells us something. However much gold was carried last week, it became incrementally more attractive to carry this week.

A positive basis is a measure of abundance. This is because it tells us about the profitability of buying metal to warehouse in carry trades. If profitability is rising, then that means the marginal demand for metal is to put into the warehouse.

Not a bullish sign, with a flat to falling price. Indeed our fundamental price for gold is still sagging, down another six Federal Reserve Notes this week.

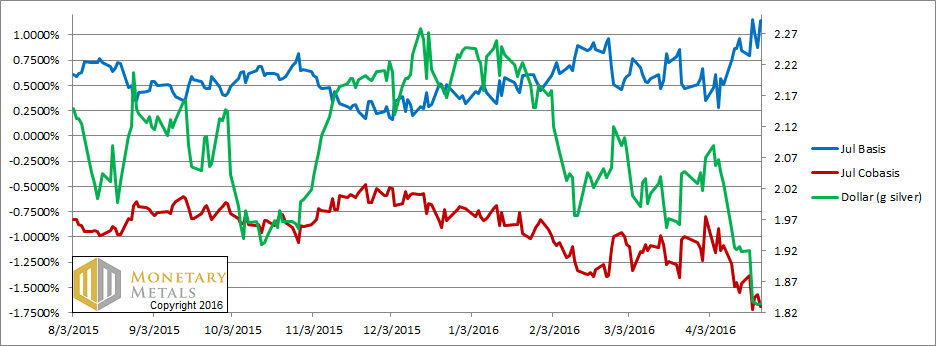

Now let’s turn to silver.

The Silver Basis and Cobasis and the Dollar Price

How much higher can the price of silver go? One talk show host appealed to the “silver faithful” with a promise of a price to skyrocket to levels even they will find “stunning”.

Our response is to point to the basis (blue line). Note that we switched from May to July.

If gold is showing some signs of abundance, silver is practically lying about in the marketscape. To carry silver for July delivery yields an annualized profit of over 1.1%. The flow of metal into the carry trade must be a torrent. If anything occurs that will stun the silver faithful, it will be the epic drop in the silver price. This will be decried as a smashdown.

Our calculated fundamental price did rise a dime this week, but it’s more than two fiat units below the market price.

There are times when the basis analysis does not predict a price move. We certainly did not call for the price of silver to jump. It’s speculation, or “animal spirits” if you will. However, then the basis can predict the reversal of the speculative move.

To be conservative—though this risks missing a quick collapse—one should wait to see the momentum peter out. As we often say at times of bearishness, we NEVER RECOMMEND NAKED SHORTING a monetary metal. The way to play this move would be to go long gold and short silver. If the gold silver ratio is 70, short 70 ounces of silver for every ounce of gold you buy.

70 would be an attractive entry point (assuming momentum dies by then). If the ratio rises to 83, then you have a gain of over 18.5%. For example, if you buy 100oz gold and short 7,000 oz silver, you will pick up over 15.6 ounces of gold.

© 2016 Monetary Metals

We get the trading thesis, that if the precious metals are in a bull market, then silver should go up more than gold. Silver is the high-beta gold. It’s a smaller market, less liquid, and at the same time it’s the preferred vehicle for betting on a rising price.

We don’t quite get the thesis that gold is going nowhere or even down, and bet on silver which is going to $50. Yet that is now our market reality. Excited silver bulls have watched as pushed silver up from $14 in late January to $17. Meanwhile the price of gold went from $1,100 to $1,260 and then back down to $1,230. The gold silver ratio initially rose from 78.5 to over 83, and down so far to 72.7.

The growing consensus is bullish. As always, we’re more interested in the fundamentals than in opinions. Let’s look at the only true picture of supply and demand fundamentals. But first, here’s the graph of the metals’ prices.

The Prices of Gold and Silver

Next, this is a graph of the gold price measured in silver, otherwise known as the gold to silver ratio. The ratio was down sharply again this week.

The Ratio of the Gold Price to the Silver Price

For each metal, we will look at a graph of the basis and cobasis overlaid with the price of the dollar in terms of the respective metal. It will make it easier to provide brief commentary. The dollar will be represented in green, the basis in blue and cobasis in red.

Here is the gold graph.

The Gold Basis and Cobasis and the Dollar Price

Look at that. Carrying gold for June delivery is now even more profitable, over 55 basis points. This is up from last week at 51bps. The increase tells us something. However much gold was carried last week, it became incrementally more attractive to carry this week.

A positive basis is a measure of abundance. This is because it tells us about the profitability of buying metal to warehouse in carry trades. If profitability is rising, then that means the marginal demand for metal is to put into the warehouse.

Not a bullish sign, with a flat to falling price. Indeed our fundamental price for gold is still sagging, down another six Federal Reserve Notes this week.

Now let’s turn to silver.

The Silver Basis and Cobasis and the Dollar Price

How much higher can the price of silver go? One talk show host appealed to the “silver faithful” with a promise of a price to skyrocket to levels even they will find “stunning”.

Our response is to point to the basis (blue line). Note that we switched from May to July.

If gold is showing some signs of abundance, silver is practically lying about in the marketscape. To carry silver for July delivery yields an annualized profit of over 1.1%. The flow of metal into the carry trade must be a torrent. If anything occurs that will stun the silver faithful, it will be the epic drop in the silver price. This will be decried as a smashdown.

Our calculated fundamental price did rise a dime this week, but it’s more than two fiat units below the market price.

There are times when the basis analysis does not predict a price move. We certainly did not call for the price of silver to jump. It’s speculation, or “animal spirits” if you will. However, then the basis can predict the reversal of the speculative move.

To be conservative—though this risks missing a quick collapse—one should wait to see the momentum peter out. As we often say at times of bearishness, we NEVER RECOMMEND NAKED SHORTING a monetary metal. The way to play this move would be to go long gold and short silver. If the gold silver ratio is 70, short 70 ounces of silver for every ounce of gold you buy.

70 would be an attractive entry point (assuming momentum dies by then). If the ratio rises to 83, then you have a gain of over 18.5%. For example, if you buy 100oz gold and short 7,000 oz silver, you will pick up over 15.6 ounces of gold.

© 2016 Monetary Metals

Central Banks may soon start buying silver

Only when the tide goes out do you discover who’s been swimming naked.” – Warren Buffett

In case of emergency, central banks go back to what they know and to what works. Once silver was a monetary commodity for central banks, today only investors buy silver. Central banks have little to none silver, but things can change – fast. In case of emergency, silver can reclaim its monetary status.

Most investors will see you as a fool when you say central banks can start buying silver even when they aren’t interested in gold. But when you think a little further, it’s not a crazy idea after all. But first you must understand the meaning of money.

Money is …

While central banks were still holding gold as part of their reserves, silver was sold off. That’s why some see gold as money but silver only as a commodity.

Many would say that central banks hate gold, based on the majority of their actions over the last 100 years, at least. However, it is not that central banks hate gold per se, but they hate it when it is in their interest to do so, and they love it when they need it.

In the seventies central banks bought gold because there wasn’t much faith in fiat currency. Faith stabilized in the eighties so gold reserves stayed the same. From the nineties till the financial crisis fiat currency was king and gold a barbaric relic.

But things changed in 07/08. Central banks were net buyers for gold again, especially emerging countries. But in the future it may be more difficult to buy gold at a reasonable price as faith in fiat currencies fades away. So at some point, central banks can embrace silver again because silver has the same properties as gold.

The only reason they were not interested in silver is because it was in their interest to hate it. But for how long? After all, it is not like having silver is new thing for them.

Read our Guide to Gold for FREE

OR … 10 ten baggers for just ten dollars

We came up with ten stocks, which have the potential to become ‘ten baggers’. Stocks that can tenfold your returns, when this market really gets going.

We combined these 10 ten baggers is a separate report, for the symbolic low price of $10. So, 10 ten baggers for ten dollars.

In case of emergency, central banks go back to what they know and to what works. Once silver was a monetary commodity for central banks, today only investors buy silver. Central banks have little to none silver, but things can change – fast. In case of emergency, silver can reclaim its monetary status.

Most investors will see you as a fool when you say central banks can start buying silver even when they aren’t interested in gold. But when you think a little further, it’s not a crazy idea after all. But first you must understand the meaning of money.

Money is …

- Divisible: should be divisible in smaller units

- Portable: able to carry it around

- Homogenous: one unit should be the same as any another unit

- Durable: should not be able to be easily destroyed or eroded

- Valuable: should have intrinsic value

Investing in silver before central banks heat up the price

But silver is also divisible, portable, homogenous, durable and valuable. A long time ago central banks had silver in their vaults as a safe haven. But now silver is almost entirely demonetized. Bretton Woods killed silver definitely when the world embraced gold and the US Dollar as true money.While central banks were still holding gold as part of their reserves, silver was sold off. That’s why some see gold as money but silver only as a commodity.

Many would say that central banks hate gold, based on the majority of their actions over the last 100 years, at least. However, it is not that central banks hate gold per se, but they hate it when it is in their interest to do so, and they love it when they need it.

In the seventies central banks bought gold because there wasn’t much faith in fiat currency. Faith stabilized in the eighties so gold reserves stayed the same. From the nineties till the financial crisis fiat currency was king and gold a barbaric relic.

But things changed in 07/08. Central banks were net buyers for gold again, especially emerging countries. But in the future it may be more difficult to buy gold at a reasonable price as faith in fiat currencies fades away. So at some point, central banks can embrace silver again because silver has the same properties as gold.

The only reason they were not interested in silver is because it was in their interest to hate it. But for how long? After all, it is not like having silver is new thing for them.

Read our Guide to Gold for FREE

OR … 10 ten baggers for just ten dollars

We came up with ten stocks, which have the potential to become ‘ten baggers’. Stocks that can tenfold your returns, when this market really gets going.

We combined these 10 ten baggers is a separate report, for the symbolic low price of $10. So, 10 ten baggers for ten dollars.

Monday, April 25, 2016

Stanley Druckenmiller – “The Greatest Moneymaking Machine In History”

Who is Stanley Druckenmiller?

Here is what hedge fund manager Scott Bessent says about Druckenmiller in the book “Inside the House of Money’

Stan may be the greatest moneymaking machine in history. He has Jim Roger’s analytical ability, George Soros’s trading ability, and the stomach of a riverboat gambler when it comes to placing his bets. His lack of volatility is unbelievable. I think he’s had something like five down quarters in 25 years and never a down year. The Quantum record from 1989 to 2000 is really his. The assets grew from $1 billion to $20 billion over that time and the performance never suffered. Soros’s record was made on a smaller amount of money at a time when there were fewer hedge funds to compete against.

Breaking the Bank of England was not a one-man job. Superlatives have gone entirely to Soros, but history has been unjust to the other genius behind the trade – Druckenmiller. Both, Soros and Druckenmiller played crucial roles and one could not have done it without the other. They were a dream-team of speculators.

Here’s is Scott Bessent again about the infamous Pound trade:

What is most interesting to me about the breaking of the pound was the combination of Stan Druckenmiller’s gamesmanship – Stan really understand risk and reward – and George’s ability to size trades. Make no mistake about it, shorting the pound was Stan Druckenmiller’s idea. Soros contribution was pushing him to take a gigantic position.

When people talk about the Breaking the Bank of England story, which netted a billion pounds to Soros, few remember the mention the risk parameters of the trade. His fund was up 12% for the year, when they decided to take the trade. Their pre-defined maximum risk was the entire year-to-date profit, but not more. It takes huge balls of steel to make such a bet.

What is the philosophy behind Stanley Druckenmiller’s exceptional performance:

1. Flexibility

The Friday before the 1987 crash, Druckenmiller goes from net short to 130% long. Here is his conversation with Jack Schwager in The New Market Wizards’ book:

– You’ve repeatedly indicated that you give a great deal of weight to technical input. With the market in a virtual free-fall at the time, didn’t the technical perspective make you apprehensive about the trade?– A number of technical indicators suggested that the market was oversold at that juncture. Moreover, I thought that the huge price base near the 2,200 level would provide extremely strong support— at least temporarily. I figured that even if I were dead wrong, the market would not go below the 2,200 level on Monday morning. My plan was to give the long position a half-hour on Monday morning and to get out if the market failed to bounce.***Another important lesson to be drawn from this interview is that if you make a mistake, respond immediately! Druckenmiller made the incredible error of shifting from short to 130 percent long on the very day before the massive October 19, 1987, stock crash, yet he finished the month with a net gain. How? When he realized he was dead wrong, he liquidated his entire long position during the first hour of trading on October 19 and actually went short. Had he been less open-minded, defending his original position when confronted with contrary evidence, or had he procrastinated to see if the market would recover, he would have suffered a tremendous loss. Instead, he actually made a small profit. The ability to accept unpleasant truths (i.e., market action or events counter to one’s position) and respond decisively and without hesitation is the mark of a great trader.***Druckenmiller flipped the portfolio from short to long, a reversal that saved Quantum in 1999, but then hurt it a few months later in 2000. Druckenmiller finished 2000 up for the year. He went from down 12% in March to up 15% for the year in his own portfolio. If you remember, the Nasdaq dumped in March 2000 but then it almost made a marginal new high in September at which point he changed his mind again, went from net long to net short, and caught the whole move down from September to December 2000.Stan is better at changing his mind that anybody I’ve ever seen. Maybe he stayed with it a little too long, but one of the great things about Stan is that he can and does turn on a dime. To paraphrase John Maynard Keynes, when the facts change, he changes his positions.

2. He understands and applies perfectly the concept of risk/reward and one of his main weapons is proper timing:

One of the things that I learned from Stan Druckenmiller is how to enter a trade. The great thing about Stan is that he can be wrong, but he rarely loses money because his entry point is so good.

3. The most important lessons from George Soros

I’ve learned many things from him, but perhaps the most significant is that it’s not whether you’re right or wrong that’s important, but how much money you make when you’re right and how much you lose when you’re wrong. The few times that Soros has ever criticized me was when I was really right on a market and didn’t maximize the opportunitySoros has taught me that when you have tremendous conviction on a trade, you have to go for the jugular. It takes courage to be a pig. It takes courage to ride a profit with huge leverage. As far as Soros is concerned, when you’re right on something, you can’t own enough.***It’s my philosophy, which has been reinforced by Mr. Soros, that when you earn the right to be aggressive, you should be aggressive. The years that you start off with a large gain are the times that you should go for it.The way to build long-term returns is through preservation of capital and home runs. You can be far more aggressive when you’re making good profits. Many managers, once they’re up 30 or 40 percent, will book their year [i.e., trade very cautiously for the remainder of the year so as not to jeopardize the very good return that has already been realized]. The way to attain truly superior long-term returns is to grind it out until you’re up 30 or 40 percent, and then if you have the convictions, go for a 100 percent year. If you can put together a few near-100 percent years and avoid down years, then you can achieve really outstanding long-term returns.***Soros is also the best loss taker I’ve ever seen. He doesn’t care whether he wins or loses on a trade. If a trade doesn’t work, he’s confident enough about his ability to win on other trades that he can easily walk away from the position. There are a lot of shoes on the shelf; wear only the ones that fit. If you’re extremely confident, taking a loss doesn’t bother you.

4. Great defense wins championships

Druckenmiller’s entire trading style runs counter to the orthodoxy of fund management. There is no logical reason why an investor (or fund manager) should be nearly fully invested in equities at all times. If an investor’s analysis points to the probability of an impending bear market, he or she should move entirely to cash and possibly even a net short position.

5. About valuation and timing the market

I never use valuation to time the market. I use liquidity considerations and technical analysis for timing. Valuation only tells me how far the market can go once a catalyst enters the picture to change the market direction.The catalyst is liquidity, and hopefully my technical analysis will pick it up.

6. About leverage:

You could be right on a market and still end up losing if you use excessive leverage.One basic market truth (or, perhaps more accurately, one basic truth about human nature) is that you can’t win if you have to win. Druckenmiller’s plunge into T-bill futures in a desperate attempt to save his firm from financial ruin provides a classic example. Even though he bought T-bill futures within one week of their all-time low (you can’t pick a trade much better than that), he lost all his money. The very need to win poisoned the trade— in this instance, through grossly excessive leverage and a lack of planning. The market is a stern master that seldom tolerates the carelessness associated with trades born of desperation.

And a more recent quote from Druckenmiller, related to Soros’s advice “don’t try to play the game better, pay attention to when the game has changed”:

I really don’t care whether we go to $70 billion or $65 billion in September, … But if you tell me quantitative easing is going to be removed over 9 or 12 months, that is a big deal

SOURCES:

INSIDE THE HOUSE OF MONEY, STEVEN DROBNEY, WILEY, 2008

Schwager, Jack D. (2009-10-13). The New Market Wizards: Conversations with America’s Top Traders. HarperBusiness. Kindle Edition.

Schwager, Jack D. (2009-10-13). The New Market Wizards: Conversations with America’s Top Traders. HarperBusiness. Kindle Edition.

Friday, April 22, 2016

[转贴] 【现金流公司 2】- 10家【手持现金 = Cash】> 【借贷 = Borrowing】的优质股,平均Dividend yiled = 4.28%. - Harryt30

Friday, April 22, 2016

股价为2016 April 21

股价为2016 April 21

昨天跟大家分享了10家【0借贷】的公司得到不错的回响。看来在动荡不安的股市里,还是有不少人喜欢Cash Is King的高股息公司,因为可以获得稳定的被动收入。而今天笔者要跟大家分享的是10家有【手持现金 = Cash】> 【借贷 = Borrowing】的优质公司。

例子:

A公司有10亿现金,5亿债务,

所以净现金, Net Cash = 10亿 - 5亿 = 5亿

为什么有些公司在有能力清还借贷的情况下还是会跟银行借钱呢??因为天有不测之风云,如果公司突然急需要用大笔钱,跟银行借贷可能需要一些时间。所以有些公司宁愿每年还一些借贷的利息,也要手握多点现金。

例子:

A公司有10亿现金,5亿债务,

所以净现金, Net Cash = 10亿 - 5亿 = 5亿

为什么有些公司在有能力清还借贷的情况下还是会跟银行借钱呢??因为天有不测之风云,如果公司突然急需要用大笔钱,跟银行借贷可能需要一些时间。所以有些公司宁愿每年还一些借贷的利息,也要手握多点现金。

举个例子,TOP GLOV现在手握的Investment securities & cash相等于8.09亿,手上握有3.374亿净现金。但是它们同时拥有4.72亿的借贷,为什么拥有清还能力的TOPGLOV不还清债务呢?原因是它们今年的目标是收购1 -2 家公司来扩张规模,因此手上需要握有大笔的现金做准备。聪明又有钱生意人会跟银行借钱做生意,而打工一族会把钱放在银行借给有钱人做生意。

回到正题,大家一起看看10家【手持现金 = Cash】> 【借贷 = Borrowing】的公司。

- 上图10家公司除了FAVCO以及PERSTIM两家是小型股之外,其他8家都是市值超过10亿的公司。

- 而这10家公司手持的现金介于1.02 - 4.28亿之间,非常难得的是UOADEV这家产业股有高达4亿多的现金。

- 此外,这10家公司中只有INARI, FAVCO以及KAREX的股价是下跌的,其他7家都活得不错的表现。

- PE10以下的就有FAVCO以及UOADEV, 周息率都在5.5%以上。FAVCO以及UOADEV在2015年的盈利分别进步6.98%和23.49%,而UOADEV在产业放缓的情况下还可以继续进步,这是非常难能可贵的。

- PERSTIM的周息率高达6.3%,今年股价也突破了新高,手持净1.02亿的现金。不过缺点是成交量非常低。

- HLIND的业绩前天才出炉,公司派发股息,全年派发42仙的股息。所以股价5天内从6.80上涨到7.48,5天上涨了10%。

- BJAUTO拥有3亿以上的现金,所以每年派发股息从不手软。

- PADINI在这一年内表现回用,业绩盈利连续进步两个季度。而且股息也保持在10仙的水平,只要股价在RM2或以下买进,1年就可以获得5%的股息。此外,这家消费股握有1.77亿的现金,想要扩张其实不愁没钱。

- MUHIBAH以及SUNCON是难得的几家Net Cash Company,Econbhd以及PTARAS也是净现金,今年建筑股的表现都非常出色。

- INARI这家公司在上市至今完成了股价超过1000%涨幅的奇迹,业绩盈利机会每年都在进步着。所以它们才可以立下40%的派息政策,现在手上握有2.59亿左右的Net Cash。

- 最后是上市3年的KAREX,盈利每个季度都在进步着。手握1.57亿左右的现金,今年分红股后股价小小跌了一些。不过这家公司是可以逢低买进的,10年后或许就是下一家TOPGLOV了。

以上纯属分享,买卖自负。

4 top investors are betting big on gold

The price of gold is down 40% from all-time highs in 2011, but big hedge fund names are betting the worst is over.

Stanley Druckenmiller's Duquesne fund was the latest one to dive in, investing close to 25% of its U.S. equity portfolio in gold-related stocks as of August 14, 2015. See the gold holdings of other top managers:

Stanley Druckenmiller's Duquesne fund was the latest one to dive in, investing close to 25% of its U.S. equity portfolio in gold-related stocks as of August 14, 2015. See the gold holdings of other top managers:

USD into gold standard

From Porter Stansberry in Stansberry Digest:

Nobody said a word for five blocks…

A few days ago, I (Porter) walked out of a dinner meeting at the Metropolitan Club of New York. I can remember every sight and sound. It all plays back in my head like a high-definition movie. This is not an April Fools’ Day joke, unfortunately. This is a true story, down to the last, incredible, detail.

It was 9:43 p.m. It was Tuesday night. It was about 45 degrees. I was with two of my closest friends and colleagues. There was no wind. Traffic was light. We took a left on Madison, heading north. We went to Club Macanudo on East 63rd Street for an after-dinner drink.

And like I said… nobody said a word.

I was in shock. It felt like I was walking away from a car accident. My adrenaline was pumping. My mind was racing. I couldn’t fully process what I had just learned… but I had never been so afraid – not like this.

At the last minute, I had been invited to have dinner with one of the most powerful men in the world. This man guards his reputation closely. For reasons that will become clear, he does not want to be named in this story. You would immediately recognize his name and you would certainly know his reputation.

His career has spanned the last 40 years and includes stints at the highest levels of the U.S. government. For the last dozen years, he has served as an advisor to the world’s wealthiest men. He sits squarely at the nexus between government policy and the country’s wealthiest and most influential people.

He invited me to dinner on the fifth floor of the Metropolitan Club. Few people outside of New York know about this club. But it’s one of the ultimate bastions of wealth and privilege in our country. Built by J.P. Morgan himself, it sits on the southeast corner of Central Park on Fifth Avenue.

Among other notable events, investing legend Warren Buffett celebrated his 50th birthday there. The most powerful and wealthiest people in the country meet there for dinner. The real policies that run our country get debated and decided there.

I was with two friends that night – our director of business development, Mark Arnold, and Erez Kalir, a well-known and successful hedge-fund manager.

Before coming to Stansberry Research three years ago, Mark was a partner at one of the largest venture-capital law firms in the U.S. He has worked on hundreds of major funding deals. He received his undergraduate degree from Duke and he has both an MBA and a law degree.

A few years ago, Erez managed around $1 billion as part of the Tiger Management group – the hedge-fund family controlled by legendary investor Julian Robertson. Today, Erez runs a small, private investment-advisory business… whose name you might recognize. (It’s called Stansberry Asset Management.*) This firm – which is separately owned and managed – licenses our name and uses our research to build portfolios for high-net-worth investors.

Erez is the smartest investor I have ever met. He received his undergraduate degree from Stanford, was a Rhodes scholar, and graduated from Yale Law School, where he was on Law Review.

You need to understand… the people I was meeting with that night were not conspiracy theorists. They are smart, experienced professionals who know the world (and the major players) of finance inside and out. They do not scare easily. They have seen panics, booms, and busts all around the world. And yet… what we learned at dinner sobered all of us and affected us in a way no other discussion in my career ever has.

Our host – who, by the way, was scheduled to appear on national television at 10 p.m., immediately after our dinner – began the meeting by describing discussions among senior policymakers in the U.S. about the possibility that the U.S. will follow Europe and Japan into negative interest rates. You probably haven’t noticed, but despite the big rebound we’ve seen in the stock market, sovereign interest rates (as measured by the yield on the U.S. 10-year Treasury bond) have continued to fall. In the first quarter of the year, the yield fell from 2.27% to 1.77%

According to our host, among U.S. policymakers it was becoming a foregone conclusion that since Europe (one of our major trading partners) and Japan were both using negative interest rates to weaken their currencies and to avoid deflation, that it was only a matter of time before the U.S. would do the same.

The likelihood that the U.S. will implement a negative interest-rate policy (or “NIRP,” for short) is worrisome. You might have heard about this new kind of monetary policy. It’s like capitalism turned upside down. Instead of being paid to save capital, you’re forced to pay just to keep the money you’ve already earned. Negative interest rates are nothing more than government theft. Its banks literally steal from you every day that you keep your money in dollars, yen, or euros.

The dinner I attended wasn’t about these kinds of NIRP policies, though. Our host was assuming that negative interest rates would certainly occur in the U.S. The problem he wanted to talk about that night wasn’t whether NIRP would happen in America. He wanted to discuss what would happen next… and how the government could possibly put capitalism back together if all hell broke loose under NIRP.

Here’s the hypothesis: What if NIRP spread globally? What if they’re implemented around the world in every major paper currency? Think of it like dominoes. Japan has done it. Europe has done it. Sweden, too.

And last night, China became the latest major domino to fall. The overnight Hong Kong interbank offer rate (“Hibor”), which determines the rate that banks in the city have to pay to borrow Chinese yuan from each other, fell to negative 3.725% annually. Who in his right mind would want to hold yuan if it costs nearly 4% a year just to keep his money in a bank?

America is likely next. If all of the world’s major reserve currencies begin paying negative interest rates, the Federal Reserve will have to follow. Otherwise, the dollar would soar and crash our economy. So if all the major banks in the world are charging negative interest rates… where will the trillions and trillions of dollars in overnight banking deposits flee to next?

Imagine you’re the head of $300 billion reinsurance giant Munich Re. You must hold huge cash reserves so you can pay claims, should they arise. Millions of people around the world depend (and have paid for) the guarantees you’ve made to protect their homes, businesses, properties, and entire cities.And now, instead of earning interest on these reserves, your company must pay huge sums of money simply to keep your capital safe. What will the people who run firms like Munich Re… or JPMorgan Chase… or Japan’s huge Sumitomo Mitsui Banking do with their capital? How can they keep it safe in an era of negative interest rates?

And what will individuals do? Where would you put your money if Bank of America and Wells Fargo began taxing your wealth and your savings every day, instead of paying you interest? How would you keep your money safe?

Let’s see what people are actually doing when faced with this conundrum. Munich Re is responding to negative interest rates by hoarding cash (tens of millions)… and by holding almost 300,000 ounces of gold. Media reports claim the firm has been an active buyer in the gold market. As Bloomberg News says…

Think about what that means for a little while… and see if you don’t find yourself more than a little worried. NIRP could trigger a massive, global “run on the bank” as everyone begins trying to hoard currency and gold to avoid the penalties being charged by the central banks for using paper money.

Trust me when I tell you… Policymakers in the U.S. are cognizant of this risk. This isn’t a doomsday scenario… It’s happening right now. These risks are exactly why gold has seen its biggest quarterly move higher in more than 30 years.

The run has started.

Look who is suddenly buying gold former vice chairman of the investment bank Goldman Sachs John Thornton is now running Barrick Gold, one of the world’s largest gold producers. Goldman has already purchased three tons of physical gold for its house account.

Stanley Druckenmiller – one of the most successful investors of the last 30 years and former head of the Quantum Fund – holds about 30% of his personal portfolio in gold.

The same is true across the top echelon of Wall Street’s best hedge-fund managers: John Paulson owns stakes in several gold-mining companies. David Einhorn is a huge gold bull, with more than $100 million invested in gold stocks. Paul Singer says it’s the only real money. Ray Dalio – founder of Bridgewater, the largest hedge fund in the world – says, “If you don’t own gold, you know neither history nor economics.”

I could go on, but you get the point. Billionaires are suddenly hoarding gold and expounding on its role in history. Doesn’t that make you wonder what’s really going on behind the scenes? More and more senior people in finance are buying huge amounts of gold. Why? Because of what I learned at dinner just a few nights ago…

After outlining the risks of NIRP and the inevitable run on paper currencies these policies will produce, our host at the Metropolitan Club asked us a simple question…

I couldn’t believe my ears. Here was a former government official – at the very highest level – openly discussing a global bank run and how the Federal Reserve and other central banks would try to stop it. I have never in my career heard anyone in government discuss such a scenario. And our host wasn’t merely pondering whether or not this could happen. He was formulating a plan to combat it. He was assuming it would happen… and soon.

He then explained there would only be one sure way to gain control of the system: To use gold. He noted that the U.S. Treasury owns more gold than anyone else in the entire world.

The details about the Treasury’s gold hoard are important to the story. So for review, the U.S. Treasury owns 248 million ounces of gold. It’s held, mostly in the form of gold bricks, at three locations: Fort Knox, West Point, and the U.S. Mint in Denver.

Also important… you should know that about two-thirds of this gold was essentially stolen from private U.S. citizens in 1933, when FDR outlawed the private ownership of gold. The right to own gold wasn’t reinstated until 1974. All of the confiscated gold was melted down into bricks. Then, in 1937, it was put on a special nine-car U.S. Army train and shipped to Fort Knox. Since then, just about the only people who have been allowed to see the gold are auditors from KPMG. No one else is allowed inside.

Our dinner host explained what would happen to this gold if NIRP policies caused a global run on paper money. And that’s when I got genuinely afraid…

The only way to re-establish credibility and regain control of the financial system in the event of a global run on paper currencies would be to re-establish the U.S. dollar’s convertibility into gold. Our host described the means for accomplishing this goal. The Fed, he said, could offer to swap all of the Treasury bonds it holds (about $2.4 trillion) for all of the gold owned by the U.S. Treasury. When you do the math, you come with a new dollar-to-gold ratio of $9,677. Roughly $10,000 an ounce.

Our host went on to describe several important nuances to how such a system would work, which goes beyond the scope of today’s Digest. I want to make sure you understand three key things I learned at this meeting…

Nobody said a word for five blocks…

A few days ago, I (Porter) walked out of a dinner meeting at the Metropolitan Club of New York. I can remember every sight and sound. It all plays back in my head like a high-definition movie. This is not an April Fools’ Day joke, unfortunately. This is a true story, down to the last, incredible, detail.

It was 9:43 p.m. It was Tuesday night. It was about 45 degrees. I was with two of my closest friends and colleagues. There was no wind. Traffic was light. We took a left on Madison, heading north. We went to Club Macanudo on East 63rd Street for an after-dinner drink.

And like I said… nobody said a word.

I was in shock. It felt like I was walking away from a car accident. My adrenaline was pumping. My mind was racing. I couldn’t fully process what I had just learned… but I had never been so afraid – not like this.

At the last minute, I had been invited to have dinner with one of the most powerful men in the world. This man guards his reputation closely. For reasons that will become clear, he does not want to be named in this story. You would immediately recognize his name and you would certainly know his reputation.

His career has spanned the last 40 years and includes stints at the highest levels of the U.S. government. For the last dozen years, he has served as an advisor to the world’s wealthiest men. He sits squarely at the nexus between government policy and the country’s wealthiest and most influential people.

He invited me to dinner on the fifth floor of the Metropolitan Club. Few people outside of New York know about this club. But it’s one of the ultimate bastions of wealth and privilege in our country. Built by J.P. Morgan himself, it sits on the southeast corner of Central Park on Fifth Avenue.

Among other notable events, investing legend Warren Buffett celebrated his 50th birthday there. The most powerful and wealthiest people in the country meet there for dinner. The real policies that run our country get debated and decided there.

I was with two friends that night – our director of business development, Mark Arnold, and Erez Kalir, a well-known and successful hedge-fund manager.

Before coming to Stansberry Research three years ago, Mark was a partner at one of the largest venture-capital law firms in the U.S. He has worked on hundreds of major funding deals. He received his undergraduate degree from Duke and he has both an MBA and a law degree.

A few years ago, Erez managed around $1 billion as part of the Tiger Management group – the hedge-fund family controlled by legendary investor Julian Robertson. Today, Erez runs a small, private investment-advisory business… whose name you might recognize. (It’s called Stansberry Asset Management.*) This firm – which is separately owned and managed – licenses our name and uses our research to build portfolios for high-net-worth investors.

Erez is the smartest investor I have ever met. He received his undergraduate degree from Stanford, was a Rhodes scholar, and graduated from Yale Law School, where he was on Law Review.

You need to understand… the people I was meeting with that night were not conspiracy theorists. They are smart, experienced professionals who know the world (and the major players) of finance inside and out. They do not scare easily. They have seen panics, booms, and busts all around the world. And yet… what we learned at dinner sobered all of us and affected us in a way no other discussion in my career ever has.

Our host – who, by the way, was scheduled to appear on national television at 10 p.m., immediately after our dinner – began the meeting by describing discussions among senior policymakers in the U.S. about the possibility that the U.S. will follow Europe and Japan into negative interest rates. You probably haven’t noticed, but despite the big rebound we’ve seen in the stock market, sovereign interest rates (as measured by the yield on the U.S. 10-year Treasury bond) have continued to fall. In the first quarter of the year, the yield fell from 2.27% to 1.77%

According to our host, among U.S. policymakers it was becoming a foregone conclusion that since Europe (one of our major trading partners) and Japan were both using negative interest rates to weaken their currencies and to avoid deflation, that it was only a matter of time before the U.S. would do the same.

The likelihood that the U.S. will implement a negative interest-rate policy (or “NIRP,” for short) is worrisome. You might have heard about this new kind of monetary policy. It’s like capitalism turned upside down. Instead of being paid to save capital, you’re forced to pay just to keep the money you’ve already earned. Negative interest rates are nothing more than government theft. Its banks literally steal from you every day that you keep your money in dollars, yen, or euros.

The dinner I attended wasn’t about these kinds of NIRP policies, though. Our host was assuming that negative interest rates would certainly occur in the U.S. The problem he wanted to talk about that night wasn’t whether NIRP would happen in America. He wanted to discuss what would happen next… and how the government could possibly put capitalism back together if all hell broke loose under NIRP.

Here’s the hypothesis: What if NIRP spread globally? What if they’re implemented around the world in every major paper currency? Think of it like dominoes. Japan has done it. Europe has done it. Sweden, too.

And last night, China became the latest major domino to fall. The overnight Hong Kong interbank offer rate (“Hibor”), which determines the rate that banks in the city have to pay to borrow Chinese yuan from each other, fell to negative 3.725% annually. Who in his right mind would want to hold yuan if it costs nearly 4% a year just to keep his money in a bank?

America is likely next. If all of the world’s major reserve currencies begin paying negative interest rates, the Federal Reserve will have to follow. Otherwise, the dollar would soar and crash our economy. So if all the major banks in the world are charging negative interest rates… where will the trillions and trillions of dollars in overnight banking deposits flee to next?

Imagine you’re the head of $300 billion reinsurance giant Munich Re. You must hold huge cash reserves so you can pay claims, should they arise. Millions of people around the world depend (and have paid for) the guarantees you’ve made to protect their homes, businesses, properties, and entire cities.And now, instead of earning interest on these reserves, your company must pay huge sums of money simply to keep your capital safe. What will the people who run firms like Munich Re… or JPMorgan Chase… or Japan’s huge Sumitomo Mitsui Banking do with their capital? How can they keep it safe in an era of negative interest rates?

And what will individuals do? Where would you put your money if Bank of America and Wells Fargo began taxing your wealth and your savings every day, instead of paying you interest? How would you keep your money safe?

Let’s see what people are actually doing when faced with this conundrum. Munich Re is responding to negative interest rates by hoarding cash (tens of millions)… and by holding almost 300,000 ounces of gold. Media reports claim the firm has been an active buyer in the gold market. As Bloomberg News says…

Institutional investors including insurers, savings banks, and pension funds are debating whether it may be worth bearing the insurance and logistics costs of holding physical cash as overnight deposit rates fall deeper below zero and negative yields dent investment returns.

Trust me when I tell you… Policymakers in the U.S. are cognizant of this risk. This isn’t a doomsday scenario… It’s happening right now. These risks are exactly why gold has seen its biggest quarterly move higher in more than 30 years.

The run has started.

Look who is suddenly buying gold former vice chairman of the investment bank Goldman Sachs John Thornton is now running Barrick Gold, one of the world’s largest gold producers. Goldman has already purchased three tons of physical gold for its house account.

Stanley Druckenmiller – one of the most successful investors of the last 30 years and former head of the Quantum Fund – holds about 30% of his personal portfolio in gold.

The same is true across the top echelon of Wall Street’s best hedge-fund managers: John Paulson owns stakes in several gold-mining companies. David Einhorn is a huge gold bull, with more than $100 million invested in gold stocks. Paul Singer says it’s the only real money. Ray Dalio – founder of Bridgewater, the largest hedge fund in the world – says, “If you don’t own gold, you know neither history nor economics.”

I could go on, but you get the point. Billionaires are suddenly hoarding gold and expounding on its role in history. Doesn’t that make you wonder what’s really going on behind the scenes? More and more senior people in finance are buying huge amounts of gold. Why? Because of what I learned at dinner just a few nights ago…

After outlining the risks of NIRP and the inevitable run on paper currencies these policies will produce, our host at the Metropolitan Club asked us a simple question…

How will the world’s central banks regain control of the monetary system when it all finally breaks down? What will get people to stop hoarding cash, to stop buying gold, to put their money back in the banks?

He then explained there would only be one sure way to gain control of the system: To use gold. He noted that the U.S. Treasury owns more gold than anyone else in the entire world.

The details about the Treasury’s gold hoard are important to the story. So for review, the U.S. Treasury owns 248 million ounces of gold. It’s held, mostly in the form of gold bricks, at three locations: Fort Knox, West Point, and the U.S. Mint in Denver.

Also important… you should know that about two-thirds of this gold was essentially stolen from private U.S. citizens in 1933, when FDR outlawed the private ownership of gold. The right to own gold wasn’t reinstated until 1974. All of the confiscated gold was melted down into bricks. Then, in 1937, it was put on a special nine-car U.S. Army train and shipped to Fort Knox. Since then, just about the only people who have been allowed to see the gold are auditors from KPMG. No one else is allowed inside.

Our dinner host explained what would happen to this gold if NIRP policies caused a global run on paper money. And that’s when I got genuinely afraid…

The only way to re-establish credibility and regain control of the financial system in the event of a global run on paper currencies would be to re-establish the U.S. dollar’s convertibility into gold. Our host described the means for accomplishing this goal. The Fed, he said, could offer to swap all of the Treasury bonds it holds (about $2.4 trillion) for all of the gold owned by the U.S. Treasury. When you do the math, you come with a new dollar-to-gold ratio of $9,677. Roughly $10,000 an ounce.

Our host went on to describe several important nuances to how such a system would work, which goes beyond the scope of today’s Digest. I want to make sure you understand three key things I learned at this meeting…

- The first thing you must understand is the world’s system of paper money is unraveling. The only way to prevent a collapse of the banking system under the weight of outrageous sovereign debts is negative interest rates… the very thing that will spark a run on the system itself. The inevitability of this outcome is already influencing the behavior of the world’s largest banks, insurance companies, and the wealthiest investors. And they’re all going to do one thing: Buy gold.

- The second thing you should know is that as this crisis unfolds, people in and around government who understand how to use our country’s gold (most of which was stolen from citizens) will re-establish financial order. But so much money has been created out of thin air that the price of gold will have to soar (relative to the dollar) to stabilize the system after it collapses.

- The third thing you have to understand is that the government will almost surely do something to prevent you from buying gold when the panic comes. That’s why our host (a former leading government official) is buying gold now. And that’s why you must do so, too – immediately.

Subscribe to:

Posts (Atom)