Genting - Are you ready to place your bets?

Genting "GENT" (pronounced as

https://www.youtube.com/watch?v=gF4sUlYTPh0, definitely not pronounced using the Queen’s English otherwise will sound like you need to use the Gent.) is a household name mainly known for their leisure themeparks, casinos, cruise, plantation, and property. To understand Genting, one would need to take a look at Genting Singapore (GENS), Genting Malaysia (GENM) and Genting Plantation (GENP).

You will find a lot of pictures and charts in this note. They say a picture tells a thousand words. Much easier to understand IMO.

For GENT the following 4 catalysts to drive the share price. Namely. 1) Turnaround in GENS, 2) The launch of Twenty Century Theme Park at Genting Highlands Malaysia, 3) TauRx, the potential blockbuster drug getting FDA approval. 4) GENP's leverage to CPO.

Catalyst 1. We expect GENS to turnaround. This following the recent 1Q results which saw GGR stabilizing as of 1Q16 while bad debt provision has stayed flat at 35%.

The share price of GENS has started to stabilized too. Earnings expectations already all time low!

If tourist arrival start to improve, the gaming and theme park of GENS will improve.

Catalyst 2.

Catalyst 2. We move on to 52.9% owned GENM which operates the highland theme park. This was what it look like in the good old days of 90s.

Come 2017, the theme park should be ready and look like this...

That’s right folks. Twenty Century Fox is opening a theme park in partneship with Genting Highlands. This is part of Genting Integrated Tourism Plan (GITP). For GITP, GENM is spending a total MYR8.1 bn and 2.3bn in capex for phase 1 and 2 respectively. In the past, the local theme park is big ROIC generator.

As someone who hasn’t been to the highland for ages, I can’t hide the excitement. Haha.

The theme park is expected to be ready by end 2017. Management however has hinted July 2017 to the investment community. For the latest photos on their status, please refer to

http://www.themeparx.com/20th-century-fox-world-malaysia/

20th Century Fox World Genting Theme Park Rides

• Rio

• Ice Age

• Titanic

• Life of Pi

• Planet of the Apes

• Alien vs. Predator

• Night at the Museum

As the theme park is being build as we speak, the financial numbers for GENM is of course not exciting. For 2016, GENM’s revenue will be driven by its UK business. The recent Brexit should not affect much on its UK operation. DB estimated about c1% decline in core profit for every 10% depeciation in the pound. UK assets comprises 19% of GENM of total assets in the form of casino property.

Similar to GENS, GENM’s earnings has already bottomed, how low can it go?

“History doesn't repeat itself but it often rhymes,” Mark Twain

“History doesn't repeat itself but it often rhymes,” Mark Twain

The timeline on GENS from start construction to finish/opening of thempark and share price during the same period. I believe the same could happen for GENM.

Catalyst 3.

Catalyst 3. TauRx may provide a blockbuster boost for Genting’s valuation. Its initial investment of MYR450m or USD150m could be worth RM15b if TauRx goes for IPO listing. This would add RM10.4b or 40% to the sum of parts of Genting.

TauRx, founded by Claude Wischik is involved in Alzeheimer research. Its biggest backers include Genting, Singapore Temasek and little known Dundee Corp.

http://www.thestar.com.my/business/business-news/2016/01/07/taurx-boost-for-genting/

http://www.bloomberg.com/news/articles/2016-03-17/a-30-year-quest-for-an-alzheimer-s-remedy-nears-the-finish-line

http://www.thestar.com.my/business/business-news/2016/01/07/taurx-boost-for-genting/

http://www.bloomberg.com/news/articles/2016-03-17/a-30-year-quest-for-an-alzheimer-s-remedy-nears-the-finish-line

When the Star and bloomberg news reported about this drug. The investors reaction was bullish and share price of Genting soared from MYR7.00 to MYR9.90 in 3 months.

To follow TauRx.

https://twitter.com/hashtag/TauRx?src=hash

The excitement in TauRx is clearly reflected in the share price of Dundee Corp which has rallied some 58% YTD.

http://www.investing.com/equities/dundee-corp

The key date to watch will be around 27 July 2016 where the company will present results from its third phase of human trial on its experiemental Alzheimer’s drug known as LMTX.

Meanwhile, we can see insiders buying Genting.

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5135433

DEALINGS IN LISTED SECURITIES (CHAPTER 14 OF LISTING REQUIREMENTS) : DEALINGS OUTSIDE CLOSED PERIOD

| Type | Announcement |

| Subject | DEALINGS IN LISTED SECURITIES (CHAPTER 14 OF LISTING REQUIREMENTS)

DEALINGS OUTSIDE CLOSED PERIOD |

| Description | Pursuant to Paragraph 14.09(a) of the Main Market Listing Requirements of Bursa Malaysia Securities Berhad, we set out below details of the dealings in the Company's securities by a Principal Officer. |

Name of Principal Officer : Tan Kong Han

Date of Dealing

|

Consideration per Share

|

Number of Shares

|

% of Issued Share Capital

|

Transaction

|

24 June 2016

|

RM7.88

|

30,000

|

0.0008

|

Acquisition

|

27 June 2016

|

RM7.84013

|

30,000

|

0.0008

|

Acquisition

|

Remarks : The percentages are computed based on the total number of issued and paid-up share capital of the Company excluding a total of 26,220,000 shares bought back by the Company and retained as treasury shares as at 24 June 2016 and 27 June 2016 respectively.

Profile

Mr. Kong Han Tan has been Deputy Chief Executive Officer of Genting Plantations Berhad since December 2010. Mr. Tan served as President and Chief Operating Officer of Genting Berhad. Mr. Tan served as the Group Chief Operating Officer of Tanjong PLC from March 2003 to June 2007. Mr. Tan has more than 13 years of working experience with an Investment Bank in Malaysia. He has been a Director of TauRx Pharmaceuticals Ltd., since November 20, 2012. He was called to the English Bar (Lincoln's Inn) in 1989 and the Malaysian Bar in 1990. He holds Bachelor of Arts degree in Economics and Law from Cambridge in 1988.

|

OMG!, insider buying ahead of clinical phase 3 trials.. a signal of confidence?

Catalyst 4. GENP is a company involved in crude palm oil (CPO) production. It has fairly young mature estates with good FFB and CPO volume growth. It also has a property development arm. It is leverage to CPO price movement.

GENP earnings and price has bottomed?

Valuations of GENT

Valuations of GENT

So are you ready to place your bets?

So are you ready to place your bets?

Fyi Investors’ chips are already rolling into Genting.

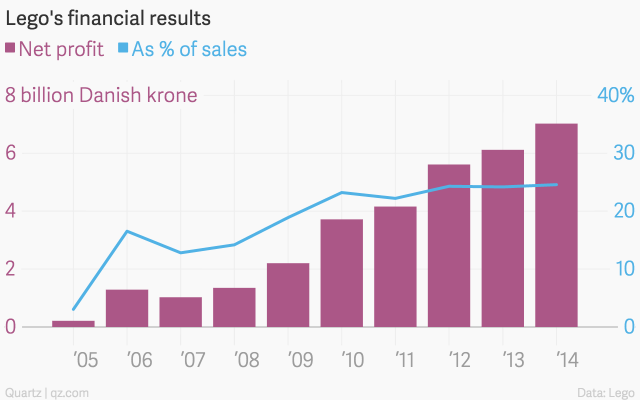

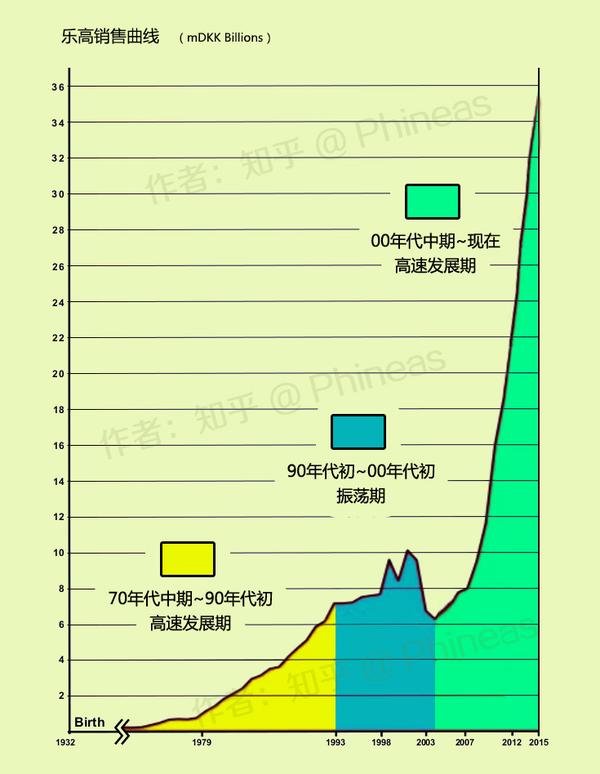

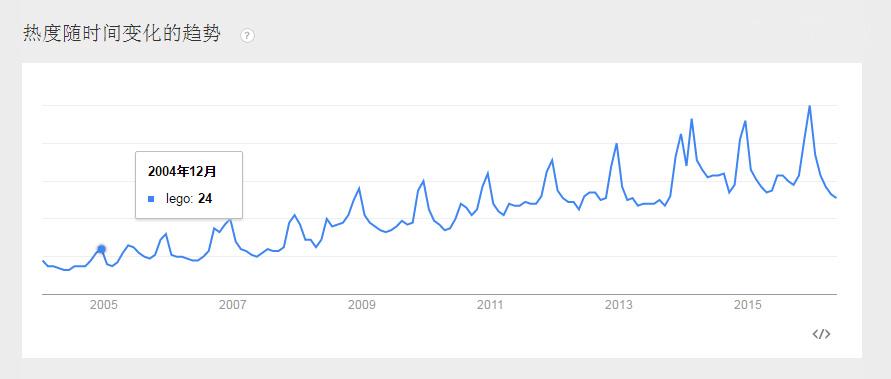

看到 2005 年财报的 net profit 是 2.14 亿丹麦克朗,而 2014 年这个数字是 70 亿克朗。

看到 2005 年财报的 net profit 是 2.14 亿丹麦克朗,而 2014 年这个数字是 70 亿克朗。

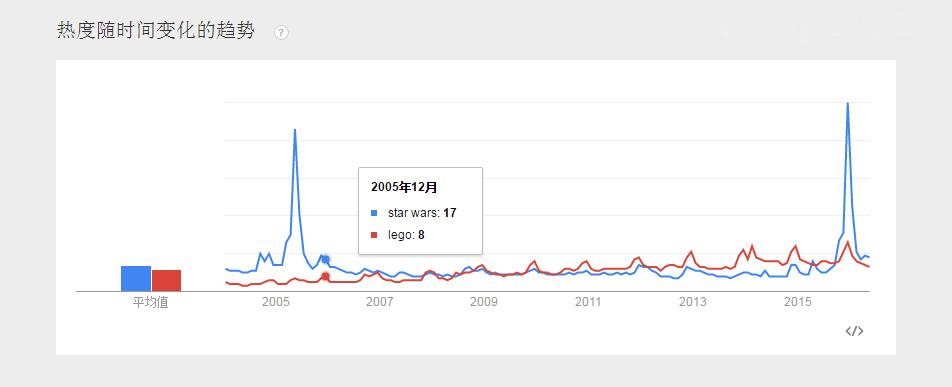

上面也有人提到了乐高大电影,确实牛逼啊,这动画电影不光是拍给熊孩子看的!能把品牌嵌入电影还不惹人讨厌,也就乐高能干得出来,这简直就是个巨大的品牌广告片!段子够逗逼,乐高人仔的渲染非常细腻,关键是结尾确实完美植入了品牌理念。一部电影,转化成了实实在在的巨额销量,攒新粉丝的效果惊人,14年上半年因为电影提振,销量直涨11%。乐高大电影还会有2,就是不知道大陆会不会引进。

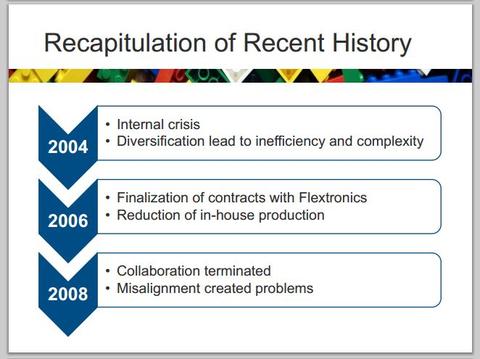

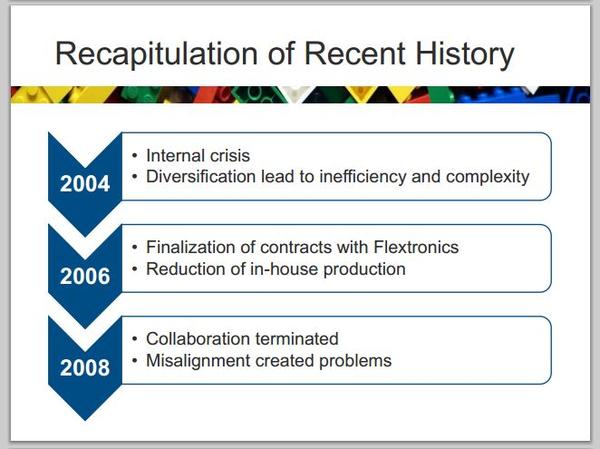

上面也有人提到了乐高大电影,确实牛逼啊,这动画电影不光是拍给熊孩子看的!能把品牌嵌入电影还不惹人讨厌,也就乐高能干得出来,这简直就是个巨大的品牌广告片!段子够逗逼,乐高人仔的渲染非常细腻,关键是结尾确实完美植入了品牌理念。一部电影,转化成了实实在在的巨额销量,攒新粉丝的效果惊人,14年上半年因为电影提振,销量直涨11%。乐高大电影还会有2,就是不知道大陆会不会引进。 我来试着回答一下05~09年那波动的净利润......那几年Lego的大动作如下:04年,全球第五大玩具制造商Lego集团与电子制造服务提供商Flextronics(伟创力)签订长期协议,外包模型、组装、包装和运输(modeling, assembly, packaging and distribution)以期降低…

我来试着回答一下05~09年那波动的净利润......那几年Lego的大动作如下:04年,全球第五大玩具制造商Lego集团与电子制造服务提供商Flextronics(伟创力)签订长期协议,外包模型、组装、包装和运输(modeling, assembly, packaging and distribution)以期降低…

从数学角度来说,如果你有六块八颗凸起的乐高长方体积木,可以砌出一亿种组合。

从数学角度来说,如果你有六块八颗凸起的乐高长方体积木,可以砌出一亿种组合。

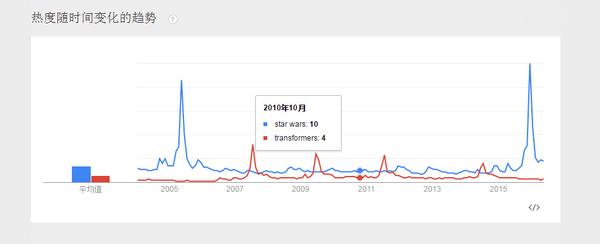

我们注意到:

我们注意到:

猜猜这是什么?乐高全球CEO的名片(读音是姚根儿,后面还会讲他),在背面印着姚根儿的座机和email。这个人偶的脖子,腿,胳膊,和手都是都是可以拆卸可以转的,连头发都可以转可以拆下来,所以转到90°的时候,CEO的眼睛会被挡住而风中凌乱,时尚时尚最时…

猜猜这是什么?乐高全球CEO的名片(读音是姚根儿,后面还会讲他),在背面印着姚根儿的座机和email。这个人偶的脖子,腿,胳膊,和手都是都是可以拆卸可以转的,连头发都可以转可以拆下来,所以转到90°的时候,CEO的眼睛会被挡住而风中凌乱,时尚时尚最时…

姚根儿挺帅的不是么?

姚根儿挺帅的不是么?