Monday, 29 August 2016 | MYT 9:16 PM

AirAsia’s net profit soars by 41%

BY EUGENE MAHALINGAM

KUALA LUMPUR: AirAsia Bhd’s net profit for its second quarter ended June 30, 2016 soared 40.8% year-on-year to RM342.12mil, boosted mainly by a 40.2% jump in aircraft operating lease income and a 24% reduction in average fuel price to US$59 (RM236) per barrel compared to a year earlier.

Revenue in the second quarter increased to RM1.62bil from RM1.32bil in the previous corresponding period, the low-cost carrier said in a statement on Monday.

Aircraft operating lease income, the second largest component of its revenue after passenger seat sales, grew to RM328.5mil. Passenger seat sales, meanwhile, were up 22.9% to RM991.4mil.

On the performance of its affiliates, AirAsia said 45%-owned Thai AirAsia posted revenue of 7.77 billion baht (RM908.82mil) in the second quarter of 2016, an increase of 13% from the same period last year while net operating profit increased by 69% year-on-year to 671.80 million baht (RM78.56mil).

“This led the associate to post a profit after tax of 767.56 million baht (RM89.78mil) (up 105% year-on-year) in the second quarter of 2016.”

Indonesia AirAsia, in which AirAsia holds a 49% stake, recorded revenue of 887.38 billion rupiah (RM270.6mil) in the second quarter of 2016, down 30% year-on-year which AirAsia said was in-line with the planned 37% decrease in capacity.

“Load factor recorded 10 percentage points improvement to 83%. Meanwhile, IAA registered a lower net operating loss of 84.60 billion rupiah (RM25.8mil) and a smaller loss after tax of 63.35 billion rupiah (RM19.31mil).

Separately, Philippines AirAsia, which is 49% owned by AirAsia Inc (AirAsia’s 40% owned associate), posted an 11% increase in revenue at 2.57 billion peso (RM223.82mil) and strong growth in the number of passenger carried.

“Load factor was at a high of 91%, up by 11 percentage points year-on-year. Cost per available seat kilometre (CASK) increased by 1% to 2.53 peso due to higher depreciation of property, plant and equipment and maintenance and overhaul cost.”

Meanwhile, 49%-owned AirAsia India recorded a 73% increase in revenue at 1.89 billion rupees (RM113.79mil) and carried higher number of passenger.

Commenting on the results, AirAsia chief executive officer Aireen Omar said in a statement that the airline saw good growth and earnings in the second quarter despite it historically being the company’s leanest.

“The highest growth seen among our ancillary products are sale of in-flight merchandise (up 400% year-on-year), AirAsia Courier (up 86%) and connecting fees for our ‘Fly-Thru’ service (up 65%).

“These led to the company recording an ancillary income per pax of RM48 this quarter (up 5% year-on-year). The group recorded a 32% year-on-year increase for Fly-Thru traffic, and Kuala Lumpur remains the largest transit hub with 83% AirAsia Group Fly-Thru traffic with the growth of 31% year-on-year.”

For the six-months period ended June 30, 2016, the low-cost carrier’s net profit more than tripled to RM1.22bil from RM392.36mil a year earlier, while revenue increased to RM3.32bil from RM2.62bil in the previous corresponding period.

Meanwhile, in a separate statement, AirAsia said its board of directors had approved the divestment of Asia Aviation Capital Ltd (AAC), the carrier’s wholly-owned aircraft leasing business.

AAC carries out the aircraft leasing business within the AirAsia group and with third party airlines

AirAsia has appointed RHB Investment Bank, Credit Suisse (Singapore) Ltd and BNP Paribas (acting through its Singapore branch) and BNP Paribas Capital (M) Sdn Bhd, as joint advisers for the potential divestment.

Tuesday, August 30, 2016

Gold - What Happens Next?

Historically, gold bull markets last years and as you can see in the following chart from Casey Research we are still in the very early innings of this one.

As OtterWood Capital notes, Gold has been correcting recently and the question is how much further can it go?

During any bull market the long term moving averages act like support (I look at the 50 day and 200 day moving averages).

Gold has broken through the 50 day and could fall as far as the 200 day and still be in a perfectly normal bull market.

Corrections in long term bull markets happen repeatedly and should be bought.

As OtterWood Capital notes, Gold has been correcting recently and the question is how much further can it go?

During any bull market the long term moving averages act like support (I look at the 50 day and 200 day moving averages).

Gold has broken through the 50 day and could fall as far as the 200 day and still be in a perfectly normal bull market.

Corrections in long term bull markets happen repeatedly and should be bought.

Friday, August 19, 2016

Lord Rothschild: Why I've sold hundreds of millions of pounds worth of shares, and bought gold

Lord Rothschild, chair of the £3.04 billion Rothschild Investment Trust, has revealed that while he has significantly reduced his exposure to listed shares, he has responded to the prevailing economic uncertainty by buying gold.

Lord Rothschild and his family have an investment of well over £100 million in the Rothschild Investment Trust.

In his latest update to shareholders he commented that recent months have seen, ‘Central bankers continuing what is surely the greatest experiment in monetary policy in the history of the world. We are therefore in uncharted waters and it is impossible to predict the unintended consequences of very low interest rates, with some 30 per cent of global government debt at negative yields, combined with quantitative easing on a massive scale. To date, at least in stock market terms, the policy has been successful with markets near their highs, while volatility on the whole has remained low. Nearly all classes of investment have been boosted by the rising monetary tide. Meanwhile, growth remains anaemic, with weak demand and deflation in many parts of the developed world’

The veteran investor continued, ‘The geopolitical situation has deteriorated with the UK having voted to leave the European Union, the presidential election in the US in November is likely to be unusually fraught, while the situation in China remains opaque and the slowing down of economic growth will surely lead to problems. Conflict in the Middle East continues and is unlikely to be resolved for many years. We have already felt the consequences of this in France, Germany and the USA in terrorist attacks. In times like these, preservation of capital in real terms continues to be as important an objective as any in the management of your Company’s assets. In respect of your Company’s asset allocation, on quoted equities we have reduced our exposure from 55 per cent to 44 per cent.’

He added, ‘Our Sterling exposure was significantly reduced over the period to 34 per cent, and currently stands at approximately 25 per cent. We increased gold and precious metals to 8 per cent by the end of June. We also increased our allocation to absolute return and credit, which delivered positive returns over the period, benefiting from a number of special situations. Within this category our new association with Eisler Capital had an encouraging start. We expect this part of the portfolio to be an increasingly important contributor to overall returns. Our significant US Dollar position has now been somewhat reduced as, following the Dollar’s rise, we saw interesting opportunities in other currencies as well as gold, the latter reflecting our concerns about monetary policy and ever declining real yields.’

The Rothschild Investment Trust has returned 58 per cent over the past three years, compared to 15 per cent for the average trust in the AIC Flexible Investment sector, making it the top performing trust.

|

| Lord Rothschild has been selling shares |

Lord Rothschild and his family have an investment of well over £100 million in the Rothschild Investment Trust.

In his latest update to shareholders he commented that recent months have seen, ‘Central bankers continuing what is surely the greatest experiment in monetary policy in the history of the world. We are therefore in uncharted waters and it is impossible to predict the unintended consequences of very low interest rates, with some 30 per cent of global government debt at negative yields, combined with quantitative easing on a massive scale. To date, at least in stock market terms, the policy has been successful with markets near their highs, while volatility on the whole has remained low. Nearly all classes of investment have been boosted by the rising monetary tide. Meanwhile, growth remains anaemic, with weak demand and deflation in many parts of the developed world’

The veteran investor continued, ‘The geopolitical situation has deteriorated with the UK having voted to leave the European Union, the presidential election in the US in November is likely to be unusually fraught, while the situation in China remains opaque and the slowing down of economic growth will surely lead to problems. Conflict in the Middle East continues and is unlikely to be resolved for many years. We have already felt the consequences of this in France, Germany and the USA in terrorist attacks. In times like these, preservation of capital in real terms continues to be as important an objective as any in the management of your Company’s assets. In respect of your Company’s asset allocation, on quoted equities we have reduced our exposure from 55 per cent to 44 per cent.’

He added, ‘Our Sterling exposure was significantly reduced over the period to 34 per cent, and currently stands at approximately 25 per cent. We increased gold and precious metals to 8 per cent by the end of June. We also increased our allocation to absolute return and credit, which delivered positive returns over the period, benefiting from a number of special situations. Within this category our new association with Eisler Capital had an encouraging start. We expect this part of the portfolio to be an increasingly important contributor to overall returns. Our significant US Dollar position has now been somewhat reduced as, following the Dollar’s rise, we saw interesting opportunities in other currencies as well as gold, the latter reflecting our concerns about monetary policy and ever declining real yields.’

The Rothschild Investment Trust has returned 58 per cent over the past three years, compared to 15 per cent for the average trust in the AIC Flexible Investment sector, making it the top performing trust.

Monday, August 8, 2016

AirAsia's resilient Fernandes eyes China to chart new expansion

CK Tan, Nikkei staff writer

AirAsia's group CEO Tony Fernandes, left, and Airbus President & CEO Fabrice Bregier signed the deal in the U.K.

KUALA LUMPUR -- Confidence has returned to AirAsia, the region's largest budget carrier by fleet size. Group Chief Executive Tony Fernandes has gotten more involved in running the airline group, charting a new course for expansion that may include a second listing, in Hong Kong, and a joint venture in China.

Nearly 20 months after one of its jetliners crashed into the Java sea, claiming 162 lives, Fernandes is aggressively charging toward a new phase of growth.

On July 12, AirAsia announced an order of 100 Airbus A321neo passenger aircraft. The deal, AirAsia's biggest since the accident, was announced during the biannual Farnborough Air Show, on the outskirts of London. The purchase lays bare a bold expansion plan for the no-frills flyer that in 2015 had 172 aircraft.

"With these aircraft," Fernades said during the signing ceremony, "we will hit 100 million passengers in the not-too-distant future."

The group, which has associate carriers in India, Indonesia, the Philippines and Thailand, ferried 51 million travelers last year.

In Farnborough, Fernandes was at ease. His casual attire included his trademark red baseball cap and a pair of jeans. He peppered the post-signing ceremony press conference with jokes. Fabrice Bregier, Airbus' president and CEO, was also on hand.

The new aircraft have a total catalog price of $12.6 billion. Deliveries are to begin in 2019. The A321neos have better fuel efficiency and are more spacious than AirAsia's current A320s. Fernandes has big plans for them.

Fernandes, a former executive of record company Warner Music Group, began his airline in 2001 after being inspired by the success of Ireland's Ryanair, which covers much of Europe.

Fernandes' no-frills business model, from which he has never strayed, made air travel and faraway vacations affordable to many Southeast Asians.

Of course, he never saw the Java Sea tragedy coming.

Nearly 20 months after one of its jetliners crashed into the Java sea, claiming 162 lives, Fernandes is aggressively charging toward a new phase of growth.

"With these aircraft," Fernades said during the signing ceremony, "we will hit 100 million passengers in the not-too-distant future."

The group, which has associate carriers in India, Indonesia, the Philippines and Thailand, ferried 51 million travelers last year.

In Farnborough, Fernandes was at ease. His casual attire included his trademark red baseball cap and a pair of jeans. He peppered the post-signing ceremony press conference with jokes. Fabrice Bregier, Airbus' president and CEO, was also on hand.

The new aircraft have a total catalog price of $12.6 billion. Deliveries are to begin in 2019. The A321neos have better fuel efficiency and are more spacious than AirAsia's current A320s. Fernandes has big plans for them.

Fernandes, a former executive of record company Warner Music Group, began his airline in 2001 after being inspired by the success of Ireland's Ryanair, which covers much of Europe.

Fernandes' no-frills business model, from which he has never strayed, made air travel and faraway vacations affordable to many Southeast Asians.

Of course, he never saw the Java Sea tragedy coming.

"My heart is filled with sadness for all the families involved in Flight 8501," Fernandes tweeted on Dec. 30, 2014, two days after the crash. "Words cannot express how sorry I am."

While AirAsia was dealing with the tragedy, it was also grappling with intense competition. Other budget carriers appeared in the skies, and fares fell. Amid all this, the group was accused of tweaking figures to boost earnings. As a result, the company's stock price last August caved in, falling to a low of 0.78 ringgit.

"Many people were writing off AirAsia, but we stuck to our guns," Fernandes recalled in Farnborough. "We have moved from a Southeast Asian airline to an Asian airline."

And AirAsia's share price has bounced back. On Tuesday, the shares closed at 2.95 ringgit, the highest they've been since two days before the crash. Cheaper fuel prices, which have buoyed the entire aviation industry, and a reshuffling of routes have contributed to the recovery.

The shares finished the week at 2.97 ringgit.

Market capitalization grew by about 7% to $2.03 billion since the crash, but still lacked behind regional peers like Shanghai-based Spring Airlines' $5.89 billion.

According to the Centre for Aviation, or Capa, an Australian consultancy, among the 20 regional airlines in Southeast Asia, 14 reported year-over-year improvements in the first quarter 2016, including all seven of the AirAsia-branded airlines. "The group is upbeat about its outlook, having recovered from a very challenging 2015," Capa added.

After the accident, Fernandes kept a low profile. Only now is he re-emerging. "Super second quarter performance for All Stars," he tweeted on Jul. 27, giving employees credit for AirAsia's strong passenger growth in the April-June period.

AirAsia said it carried 13.9 million travelers during the quarter, 12% more than a year earlier, despite the April-June period traditionally being "our slowest quarter," Fernandes said.

The bumper passenger numbers are thanks to higher demand in Malaysia and Thailand.

By way of comparison, AirAsia's closest rival in the region, Cebu Pacific Air, out of the Philippines, carried 5.2 million in the quarter.

Ten new routes were added during the quarter, mainly to second-tier Chinese cities, which now account for about 40% of revenue. AirAsia also increased the frequency it flies to many of its destinations.

The group is to announce its latest earnings by the end of the month.

In the 20 months since the accident, AirAsia has undergone operational and structural changes.

Fernandes gave up the carrier's ASEAN headquarters, in Jakarta, and put it back in Kuala Lumpur. The CEO had hoped the Jakarta base would lead to growth in Indonesia and the surrounding region.

In April, Fernandes received shareholder approval to raise his stake in AirAsia from 18.9% to 32.4% through Tune Live, a private company co-owned with Kamarudin Meranun, who co-founded AirAsia with Fernandes. The new share issuance will raise 1 billion ringgit ($247 million), which will be used to pare debt and as capital expenditures.

The AirAsia Group's net debt after offsetting cash balances amounted to 9.2 billion ringgit as of March.

"The placement signals the conviction of the major shareholders with regard to the prospects of AirAsia, given the sizable cash outlay and expanded share base of the group," said Marvin Khor of AllianceDBS Research. He added that the capital injection will reduce the carrier's gross debt-to-equity ratio from 2.8 to 2.2, raising its stock valuation.

After the Airbus order, Fernandes traveled to the U.S. and Europe to let institutional investors like Fidelity and The Boston Company Asset Management know that they might want to kick AirAsia's tires. Perhaps they'll find a bargain.

From Paris, Fernandes tweeted, "15 days but very rewarding for me and investors now know how undervalued we are."

To be a bargain, though, the shares have to look like they are ready to jump in price. In other words, AirAsia needs to continue growing.

That is not going to happen in Southeast Asia. Budget short-haul routes there have approached "maturity," Capa said in a report earlier this year. Low-cost carriers made up of 56% of the seats flown in the region, compared to 11% in Northeast Asia.

For AirAsia, then, growth means going north.

To drive growth in China and Japan, AirAsia in June set up North Asia, a Hong Kong-based subsidiary.

The president is Kathleen Tan, who was in the music industry before 2004, when she was named AirAsia's commercial director. She was promoted in 2013 to head of AirAsiaExpedia, a joint venture with a travel agency that AirAsia has since divested.

"North Asia -- with China, South Korea, Japan and Taiwan -- is considered a high growth region" for no-frills flyers, Tan told the Nikkei Asian Review. Tan said demand for regional travel is high, partly due to the proximity of the countries and cultural similarities.

Tan's top priority is China. China's budget aviation market is growing rapidly. A raft of new players entered the skies after the government began opening new routes to promote economic growth in the western part of the country. Spring Airlines and West Air enjoy big pieces of China's low-coast market.

Fernandes said he will pursue more connections to second-tier Chinese cities.

"I can confirm China is a market we will love to be in," he said. "We are not interested in Beijing or Shanghai or those big metropolises. What AirAsia is good at is developing those secondary and tertiary routes, and those are what we are looking at."

Fernandes continued that AirAsia's forte is "providing connectivity where there isn't any connectivity and providing economic growth where there isn't any economic growth."

The strategy is to avoid directly competing with both full-service and budget carriers that have already established hubs in the country. AirAsia might do this by taking the joint venture route. He said AirAsia has been approached by Chinese companies in this regard.

Hong Kong's capital market could also beckon AirAsia.

"We need to attract a new form of capital and awareness of AirAsia," Fernandes said in Farnborough, adding that a Hong Kong listing could help AirAsia accomplish these goals. "It is something we are investigating," he said.

The carrier is also getting ready to start crisscrossing Japan again. It has received two A320s, and Tan said the group hopes to begin test flights this month.

Pending regulatory approval, it hopes to begin commercial flights from its base in Nagoya come January.

It will have to compete against established peers like Peach in Japan and Spring Airlines in China, and the relatively demanding customers in North Asia who may have yet to be fully accustomed to no-frills travels.

"While I joke and laugh but it is not easy," Fernandes said in response to a question on how he manages challenges in different markets.

"To me, business is the same whether it is in an airline or music: Maximize the top line, minimize the cost, do a lot of marketing and be different."

While AirAsia was dealing with the tragedy, it was also grappling with intense competition. Other budget carriers appeared in the skies, and fares fell. Amid all this, the group was accused of tweaking figures to boost earnings. As a result, the company's stock price last August caved in, falling to a low of 0.78 ringgit.

"Many people were writing off AirAsia, but we stuck to our guns," Fernandes recalled in Farnborough. "We have moved from a Southeast Asian airline to an Asian airline."

And AirAsia's share price has bounced back. On Tuesday, the shares closed at 2.95 ringgit, the highest they've been since two days before the crash. Cheaper fuel prices, which have buoyed the entire aviation industry, and a reshuffling of routes have contributed to the recovery.

The shares finished the week at 2.97 ringgit.

Market capitalization grew by about 7% to $2.03 billion since the crash, but still lacked behind regional peers like Shanghai-based Spring Airlines' $5.89 billion.

According to the Centre for Aviation, or Capa, an Australian consultancy, among the 20 regional airlines in Southeast Asia, 14 reported year-over-year improvements in the first quarter 2016, including all seven of the AirAsia-branded airlines. "The group is upbeat about its outlook, having recovered from a very challenging 2015," Capa added.

After the accident, Fernandes kept a low profile. Only now is he re-emerging. "Super second quarter performance for All Stars," he tweeted on Jul. 27, giving employees credit for AirAsia's strong passenger growth in the April-June period.

AirAsia said it carried 13.9 million travelers during the quarter, 12% more than a year earlier, despite the April-June period traditionally being "our slowest quarter," Fernandes said.

The bumper passenger numbers are thanks to higher demand in Malaysia and Thailand.

By way of comparison, AirAsia's closest rival in the region, Cebu Pacific Air, out of the Philippines, carried 5.2 million in the quarter.

Ten new routes were added during the quarter, mainly to second-tier Chinese cities, which now account for about 40% of revenue. AirAsia also increased the frequency it flies to many of its destinations.

The group is to announce its latest earnings by the end of the month.

In the 20 months since the accident, AirAsia has undergone operational and structural changes.

Fernandes gave up the carrier's ASEAN headquarters, in Jakarta, and put it back in Kuala Lumpur. The CEO had hoped the Jakarta base would lead to growth in Indonesia and the surrounding region.

In April, Fernandes received shareholder approval to raise his stake in AirAsia from 18.9% to 32.4% through Tune Live, a private company co-owned with Kamarudin Meranun, who co-founded AirAsia with Fernandes. The new share issuance will raise 1 billion ringgit ($247 million), which will be used to pare debt and as capital expenditures.

The AirAsia Group's net debt after offsetting cash balances amounted to 9.2 billion ringgit as of March.

"The placement signals the conviction of the major shareholders with regard to the prospects of AirAsia, given the sizable cash outlay and expanded share base of the group," said Marvin Khor of AllianceDBS Research. He added that the capital injection will reduce the carrier's gross debt-to-equity ratio from 2.8 to 2.2, raising its stock valuation.

After the Airbus order, Fernandes traveled to the U.S. and Europe to let institutional investors like Fidelity and The Boston Company Asset Management know that they might want to kick AirAsia's tires. Perhaps they'll find a bargain.

From Paris, Fernandes tweeted, "15 days but very rewarding for me and investors now know how undervalued we are."

To be a bargain, though, the shares have to look like they are ready to jump in price. In other words, AirAsia needs to continue growing.

That is not going to happen in Southeast Asia. Budget short-haul routes there have approached "maturity," Capa said in a report earlier this year. Low-cost carriers made up of 56% of the seats flown in the region, compared to 11% in Northeast Asia.

For AirAsia, then, growth means going north.

To drive growth in China and Japan, AirAsia in June set up North Asia, a Hong Kong-based subsidiary.

The president is Kathleen Tan, who was in the music industry before 2004, when she was named AirAsia's commercial director. She was promoted in 2013 to head of AirAsiaExpedia, a joint venture with a travel agency that AirAsia has since divested.

"North Asia -- with China, South Korea, Japan and Taiwan -- is considered a high growth region" for no-frills flyers, Tan told the Nikkei Asian Review. Tan said demand for regional travel is high, partly due to the proximity of the countries and cultural similarities.

Tan's top priority is China. China's budget aviation market is growing rapidly. A raft of new players entered the skies after the government began opening new routes to promote economic growth in the western part of the country. Spring Airlines and West Air enjoy big pieces of China's low-coast market.

Fernandes said he will pursue more connections to second-tier Chinese cities.

"I can confirm China is a market we will love to be in," he said. "We are not interested in Beijing or Shanghai or those big metropolises. What AirAsia is good at is developing those secondary and tertiary routes, and those are what we are looking at."

Fernandes continued that AirAsia's forte is "providing connectivity where there isn't any connectivity and providing economic growth where there isn't any economic growth."

The strategy is to avoid directly competing with both full-service and budget carriers that have already established hubs in the country. AirAsia might do this by taking the joint venture route. He said AirAsia has been approached by Chinese companies in this regard.

Hong Kong's capital market could also beckon AirAsia.

"We need to attract a new form of capital and awareness of AirAsia," Fernandes said in Farnborough, adding that a Hong Kong listing could help AirAsia accomplish these goals. "It is something we are investigating," he said.

The carrier is also getting ready to start crisscrossing Japan again. It has received two A320s, and Tan said the group hopes to begin test flights this month.

Pending regulatory approval, it hopes to begin commercial flights from its base in Nagoya come January.

It will have to compete against established peers like Peach in Japan and Spring Airlines in China, and the relatively demanding customers in North Asia who may have yet to be fully accustomed to no-frills travels.

"While I joke and laugh but it is not easy," Fernandes said in response to a question on how he manages challenges in different markets.

"To me, business is the same whether it is in an airline or music: Maximize the top line, minimize the cost, do a lot of marketing and be different."

Wednesday, August 3, 2016

根本就沒有所謂的狙擊手 (From JIM)

80年代初,大劉把Evergo股份配售給基金。但由於愛美高產品滯銷引致股價下跌,大劉在股市買入股份,最後重新收購並掌握控制權。當初出手價大約為2港元,購回價約7毫,其獲利之豐厚,可想而知。其後他狙擊多次採用同一手法收購其他公司股份,更狙擊老牌地產商華人置業,華人置業控制中華娛樂,此兩家公司控制中環貴重物業的華人行及娛樂行。在兩個月內,由手無一股,至收購馮秉芬家族及李冠春家族手上的股份,持股四成,成為該公司的大股東,終使兩大家族出售其手上的股份予公司醫生韋利及市場人士,終結華人置業收購戰。其後,該公司成為大劉的狙擊艦,先後購入幾家空殼公司及大量的股份,並大量供股,大劉又曾狙擊擁有半島酒店的上海大酒店,但未能獲得董事席位及控制權,最後,大股東嘉道理家族購回劉鑾雄持有股份,並為劉鑾雄取得鉅額利潤。

他狙擊的目標都是市值龐大、股價波動較少、淨資產偏高的老牌上市公司。原因有兩點:一是大股東為了保留控股權,往往被迫回購股票,這時市場已經炒高,「狙擊手」必然獲利豐厚;二是,即便大股東放棄,「狙擊手」也可以在高位拋售,直接獲利。

這些年做投資下來,我深深感悟到,一切都沒有那麼神奇,其實在投資這個行業裡,根本就沒有所謂的狙擊手。你看看萬字醬油如何抵潮州佬就知,卒之搞到一垞屎。資本市場,是一個四層結構:老散,莊家,土豪,Family。土豪,就是人們經常聽到的什麼中國首富,某某大鱷。而土豪背後,各有各的老闆。

資本市場上,真真正正的狙擊手,靠狙擊企業發財的只有一個,就是今年80歲的華爾街

破產當飯吃的Donald Trump當然是他狙擊嘅最佳對象,2009年,Icahn及Donal Trump就為大西洋城、拉

不光是創業者,我們投資人也都是豬。而所謂的馬後炮也僅僅是大家事後總結出來的說辭,很少有人能洞見未來的趨勢,Camino咁好賣?當初點知?有早知冇乞衣,對於絕大多數人而言,你只需要跟著這個大趨勢走就行了,即係跟住我。

所以很多看似光榮偉大的事情,最開始做的原因或許是很簡單的,或許就是沒辦法死撐下來的結果,完全沒有那麼神機妙算。

我經常分享的一句話:我們需要意識到自己時刻都處在「北韓」的狀態。這句話的意思就是我們所處的環境並沒有想像中的完美,但一般廢柴意識不到。而在別人的眼中,或許我們就身處在「北韓」之中。一切事物都是在不斷發展與進化中的,即便處於「北韓」的狀態,也要明白事物基本面的重要性要遠高於扭曲的現狀。

我們經常會問創業者,你有沒有標竿的美國公司。因為常識告訴我們,如果你能在一個成熟的資本市場中找到一家成熟的公司作為Benchmark,那證明你的這個模式可能就是可行的。

有一句經典的西方諺語:Don’t Reinvent the Wheel。翻譯過來就是不要重新發明輪子,這句話在諮詢界非常有名,意思是現實中的全新的問題很少,很多問題的解決方案在其他地方都有現成的,所以不要重新設計解決方案,要善於利用別人的成果。這已經被很多人奉為了常識。

跳出來想一想,用戶到底想要的是什麼?班老細究竟愛看什麼?

Monday, August 1, 2016

RGB eyeing new business in Europe, South America

GEORGE TOWN: Electronic gaming machine and equipment maker RGB International Bhd is eyeing new businesses in Europe and South America, as the company seeks to expand its market reach.

RGB derives 95% of its sales from the Asia-Pacific region.

“We want to move away from our traditional markets to broaden the revenue base for the group,” said group managing director Datuk Chuah Kim Seah (pic).

The company, he said had secured orders for 700 units of gaming machines valued at RM80mil for the first half 2016.

About 500 units had been delivered to customers.

“The remaining 200 will be delivered in the third quarter. With the delivery of the 700 units, we are projecting double-digit percentage growth over last year’s net profit,” he told StarBiz.

The sales of gaming machines made up about 70% of the group’s revenue, while the remainder was contributed by the RGB’s gaming concession programme, which included the leasing of machines and equipment.

Chuah said the group was targeting to sell more machines than last year’s 1,300 units, which generated RM145mil in revenue.

For the second half, the group had 400 more gaming machines with an estimated market value RM45mil to deliver before the end of the year.

“The total undelivered units to date is 600, which includes the 200 yet to be delivered units secured in the first half.

“To surpass last year’s goal, we need to secure sales for 300 more units,” he said.

On RGB’s concession business, the leasing of the machines in the Asia region is expected to generate RM7.6mil per month for 2016, compared with RM7mil in 2015.

RGB leases its gaming machines to customers in Indochina, the Philippines, Timor Leste and Nepal.

“The Philippines is one of the largest markets for us,” he said.

Chuah said the group would be leasing machines soon under its concession programme to Kathmandu, which is a new market for the group.

“The machines are ready to be shipped out and should be operational by the fourth quarter,” he said.

RGB reported a 37% increase in net profit to RM5.9mil in the first quarter ended March 31, as revenue improved 45% to RM56mil.

Meanwhile, the group has settled the remaining RM27mil debts owed under the Commercial Papers Medium Term Notes (CPMTN) programme ahead of the scheduled final payment due in 2019.

“The group has more than RM60mil cash in hand, after settling the CPMTN debts,” Chuah said.

This cashpile will come in handy as the group explores opportunities in new markets.

RGB derives 95% of its sales from the Asia-Pacific region.

“We want to move away from our traditional markets to broaden the revenue base for the group,” said group managing director Datuk Chuah Kim Seah (pic).

The company, he said had secured orders for 700 units of gaming machines valued at RM80mil for the first half 2016.

About 500 units had been delivered to customers.

“The remaining 200 will be delivered in the third quarter. With the delivery of the 700 units, we are projecting double-digit percentage growth over last year’s net profit,” he told StarBiz.

The sales of gaming machines made up about 70% of the group’s revenue, while the remainder was contributed by the RGB’s gaming concession programme, which included the leasing of machines and equipment.

Chuah said the group was targeting to sell more machines than last year’s 1,300 units, which generated RM145mil in revenue.

For the second half, the group had 400 more gaming machines with an estimated market value RM45mil to deliver before the end of the year.

“The total undelivered units to date is 600, which includes the 200 yet to be delivered units secured in the first half.

“To surpass last year’s goal, we need to secure sales for 300 more units,” he said.

On RGB’s concession business, the leasing of the machines in the Asia region is expected to generate RM7.6mil per month for 2016, compared with RM7mil in 2015.

RGB leases its gaming machines to customers in Indochina, the Philippines, Timor Leste and Nepal.

“The Philippines is one of the largest markets for us,” he said.

Chuah said the group would be leasing machines soon under its concession programme to Kathmandu, which is a new market for the group.

“The machines are ready to be shipped out and should be operational by the fourth quarter,” he said.

RGB reported a 37% increase in net profit to RM5.9mil in the first quarter ended March 31, as revenue improved 45% to RM56mil.

Meanwhile, the group has settled the remaining RM27mil debts owed under the Commercial Papers Medium Term Notes (CPMTN) programme ahead of the scheduled final payment due in 2019.

“The group has more than RM60mil cash in hand, after settling the CPMTN debts,” Chuah said.

This cashpile will come in handy as the group explores opportunities in new markets.

获20亿Dyson合约普遍看好‧星光资源依赖单一大客户

获20亿Dyson合约普遍看好‧星光资源依赖单一大客户

(吉隆坡18日讯)星光资源(SKPRES,7155,主板工业产品组)获英国Dyson颁发电子消费产品制造合约,总值高达20亿令吉,合约期限为期4年,每年价值5亿令吉,主要替代之前取消的合约。

(吉隆坡18日讯)星光资源(SKPRES,7155,主板工业产品组)获英国Dyson颁发电子消费产品制造合约,总值高达20亿令吉,合约期限为期4年,每年价值5亿令吉,主要替代之前取消的合约。

由于大马雇用外劳政策改变,去年5月获Dyson公司颁发每年4亿令吉吸尘机合约将不再继续;另外,每年生产价值6亿令吉的无线吸尘机合约(为期5年)则保持不变。

分析

星光资源虽获新合约,但也失去一些合约,惟新合约的价值让分析员普遍看好,唯隐忧是过于依赖单一大客户。

肯纳格研究相当看好上述合约,星光资源拥有Dyson旗下吹风机(Supersonic)的独家制造商,Dyson未来可能会颁发更多合约予星光资源,因Dyson打算继续进行扩展。

安联星展研究认为过于依赖单一客户是隐忧,星光资源2016财政年,55%的营业额由Dyson贡献,并预期2017财政年比例将走高至72%。若Dyson终止合约,届时星光资源净利将受到影响。有鉴于此,星光资源期望来自非Dyson贡献的营业额可取得成长,并设下8%成长的目标。

安联星展补充,星光资源在柔佛士乃的工厂空间使用率为25%,余下75%为空置地段,相信星光资源将会提升使用率,以攫取更多合约。

净现金公司

尽管星光资源过去不断进行扩展计划,但该公司仍保持净现金地位,安联星展认为,2017至2019财政年,星光资源仍可以保持净现金地位。

达证券认为,星光资源虽然可从上述合约受惠,但外劳冻结,可能会导致盈利受损,因此下调2017至2019财政年的净利预测。

大众研究则表示,一旦所有产品生产线全面使用,星光资源未来净利仍有成长空间,本益比介于10至12倍,加上强劲资产负债表,是该公司值得看好的优势。

Holistic View of SKP Resources with Fundamental Analysis & iVolume Spread Analysis (iVSAChart)

Background and Core Business

SKP Resources Bhd was listed on Bursa Malaysia in 2000 and is categorised under the Miscellaneous Manufacturing industry. It belongs to the Industrial Product, FBM Small Cap and FBM Emas Indices. SKP Resources Bhd is an integrated plastic manufacturer, with 3 wholly owned subsidiaries: SKP (Syarikat Sin Kwang Plastic Industries Sdn Bhd), GHI (Goodhart Industries Sdn Bhd) and GHL (Goodhart Land Sdn Bhd). They also own 63% of another subsidiary known as GHT (Goodhart Technology Sdn Bhd). They are based in Batu Pahat, Johor.

Essentially, all the subsidiaries work synergistically from design and fabrication of high precision plastic molds to the manufacturing of plastic parts and components, sub-assembly and other secondary processes. Each subsidiary specialises in the manufacturing of distinct products for different clients. These parts are finally used as casings of media players, printers/scanners, video game console peripherals and also TV cabinets.

SKP Resources proudly lists their clients (both direct and indirect) from MNCs such as Apple, Fujitsu, Sharp, Pioneer, Dyson, HP, Flextronics, Microsoft and Sony.

The FY ended on 31st March 2016 and they are in their 1st quarter for FY 2017. The next quarterly results should be due sometime in August 2016. Market capitalisation stands at around RM1.4 billion.

Financial Brief and Ratios (Historical)

SKP Resources had seen stellar growth in their revenue for the past 5 years, with the highest turnover recorded in FY 2016. This translated into a profit of RM 82 million for its shareholders last year, while profit margin increased only slightly from 6.8% to 7.8% y-o-y. This is due to the increase in cost of revenue, reported at a figure of RM 902 million.

Although the PE ratio is not low, it has reduced over the years from the 40s to less than 20 today. ROE is relatively on the low end. No dividends were declared for FY2016. It is worth mentioning that the company had managed to reduce their current liabilities by nearly half from RM 410 million to RM 200 million during FY 2016.

In terms of cash flow, it has recorded its highest operating cash flow in 2015 at around RM 221 million, at the same time using up to RM 149 million for investing activities in the same year. In line with the increase in cost of revenue during FY2016, do take cautionary note that operating cash flow has turned negative to -RM 37 million from RM 221 million just a year ago. Similarly, Free Cash Flow has turned negative to -RM 70 million for FY 2016.

iVolume Spread Analysis (iVSA) & comments based on iVSAChart software – SKP Resources

Interested to learn more?

- Join our Investment & Market Outlook Conference on 28th Aug 2016. Find out more via: https://www.ivsachart.com/investconference2016.php

- Website: https://www.ivsachart.com/events.php

- Email: sales@ivsachart.com

- WhatsApp: +6011 2125 8389/ +6018 286 9809

- Follow & Like us on Facebook: https://www.facebook.com/priceandvolumeinklse/

This article only serves as reference information and does not constitute a buy or sell call. Conduct your own research and assessment before deciding to buy or sell any stock. If you decide to buy or sell any stock, you are responsible for your own decision and associated risks.

SKP Resources Bhd was listed on Bursa Malaysia in 2000 and is categorised under the Miscellaneous Manufacturing industry. It belongs to the Industrial Product, FBM Small Cap and FBM Emas Indices. SKP Resources Bhd is an integrated plastic manufacturer, with 3 wholly owned subsidiaries: SKP (Syarikat Sin Kwang Plastic Industries Sdn Bhd), GHI (Goodhart Industries Sdn Bhd) and GHL (Goodhart Land Sdn Bhd). They also own 63% of another subsidiary known as GHT (Goodhart Technology Sdn Bhd). They are based in Batu Pahat, Johor.

Essentially, all the subsidiaries work synergistically from design and fabrication of high precision plastic molds to the manufacturing of plastic parts and components, sub-assembly and other secondary processes. Each subsidiary specialises in the manufacturing of distinct products for different clients. These parts are finally used as casings of media players, printers/scanners, video game console peripherals and also TV cabinets.

SKP Resources proudly lists their clients (both direct and indirect) from MNCs such as Apple, Fujitsu, Sharp, Pioneer, Dyson, HP, Flextronics, Microsoft and Sony.

The FY ended on 31st March 2016 and they are in their 1st quarter for FY 2017. The next quarterly results should be due sometime in August 2016. Market capitalisation stands at around RM1.4 billion.

Financial Brief and Ratios (Historical)

SKP Resources (7155.KL)

|

FY 2016

|

| Revenue (RM’000) |

1,051,027

|

| Net Earnings (RM’000) |

82,145

|

| Net Profit Margin (%) |

7.82

|

| EPS (RM) |

0.070

|

| PE Ratio (PER) |

17.52

|

| Dividend Yield (%) |

1.58

|

| ROE (%) |

23.40

|

| Cash Ratio |

0.216

|

| Current Ratio |

1.834

|

| Total Debt to Equity Ratio |

0.158

|

SKP Resources had seen stellar growth in their revenue for the past 5 years, with the highest turnover recorded in FY 2016. This translated into a profit of RM 82 million for its shareholders last year, while profit margin increased only slightly from 6.8% to 7.8% y-o-y. This is due to the increase in cost of revenue, reported at a figure of RM 902 million.

Although the PE ratio is not low, it has reduced over the years from the 40s to less than 20 today. ROE is relatively on the low end. No dividends were declared for FY2016. It is worth mentioning that the company had managed to reduce their current liabilities by nearly half from RM 410 million to RM 200 million during FY 2016.

In terms of cash flow, it has recorded its highest operating cash flow in 2015 at around RM 221 million, at the same time using up to RM 149 million for investing activities in the same year. In line with the increase in cost of revenue during FY2016, do take cautionary note that operating cash flow has turned negative to -RM 37 million from RM 221 million just a year ago. Similarly, Free Cash Flow has turned negative to -RM 70 million for FY 2016.

iVolume Spread Analysis (iVSA) & comments based on iVSAChart software – SKP Resources

· Above is SKP Resources weekly chart showing price & volume action for the last 6 months

· Prices were ranging sideways with some Signs of Strength (green arrows) seen around pivot lows

· Although the bulls had their chance, there were unsuccessful attempts to break beyond RM 1.40 level

· Instead its’ prices drifted lower after the Sign of Weakness (red arrow) appeared in May 2016 culminating in breaking of support level around RM 1.23 in June 2016

· Strong hands emerged when prices hit around the level RM 1.14 to RM 1.12 and the down move has temporarily ceased

· For a sustainable new uptrend, not only do we need to see prices reacting favorably to the Signs of Strength (green arrow) that have appeared in July 2016 but also bullish attempts to rally and break above the RM 1.40 level

Interested to learn more?

- Join our Investment & Market Outlook Conference on 28th Aug 2016. Find out more via: https://www.ivsachart.com/investconference2016.php

- Website: https://www.ivsachart.com/events.php

- Email: sales@ivsachart.com

- WhatsApp: +6011 2125 8389/ +6018 286 9809

- Follow & Like us on Facebook: https://www.facebook.com/priceandvolumeinklse/

This article only serves as reference information and does not constitute a buy or sell call. Conduct your own research and assessment before deciding to buy or sell any stock. If you decide to buy or sell any stock, you are responsible for your own decision and associated risks.

Thursday, July 28, 2016

MQ Research: AirAsia’s air traffic beats estimates

AirAsia reported its operating numbers for the second quarter of 2016, reflecting the performance of its Malaysian, Thai, Indonesian, Indian, and Philippine entities. In terms of air traffic, AirAsia unveiled a better-than-expected performance, beating Macquarie Equities Research’s (MQ Research) estimates by 7.8%, which translated to a better than expected load factor. In its report, MQ Research reiterated an ‘Outperform’ rating on AirAsia, with a 12-month target price of RM3.50.

Event

Impact

Action and recommendation

Event

- AirAsia (AIRA MK) released a good set of 2Q16 operating statistics on late Tuesday.

- In terms of air traffic (RPK), its Malaysian entity, the major contributor to MQ Research’s sum-of-parts target price, is tracking 8% ahead of MQ Research’s estimates and its India entity is tracking marginally above expectations (4%), while its Thai and Indonesia entities are tracking in line with MQ Research’s estimates. However, its Philippine entity is tracking marginally below MQ Research’s estimates due to an unexpected capacity reduction.

Impact

- Load factor improvements across its five entities in Malaysia, Thailand, Indonesia, Philippines and India.

- Malaysia AirAsia improved load factors by 6.7% to 87% and delivered a 10% passenger growth in an industry that had zero growth in 2Q16. Traffic beat MQ Research’s expectations by 7.8% and capacity was in line with MQ Research’s expectations, leading to the positive surprise in load factors

- Thai AirAsia delivered double-digit passenger growth in 2Q16, carrying 18% more passengers in 2Q16. Its three-year compound annual growth rate (CAGR) stands at 20%, a commendable performance, in MQ Research’s view. Capacity and traffic figures for Thai AirAsia were in line with MQ Research’s expectations.

- Indonesia AirAsia, in line with its restructuring plans, carried 2% more passengers. Load factors were 83%, an increase from 73% in 2Q15. Capacity and traffic figures for Indonesia AirAsia were in line with MQ Research’s expectations.

- Philippines AirAsia surprisingly reduced 7% year-on-year (YoY) capacity in 2Q16, thus leading to traffic figures marginally below MQ Research’s expectations. Load factor received a boost, at 91% for 2Q16 vs MQ Research’s expectations of 85%.

Action and recommendation

- Reiterate Outperform with a target price of RM3.50 (+25.8% TSR).

Tuesday, July 26, 2016

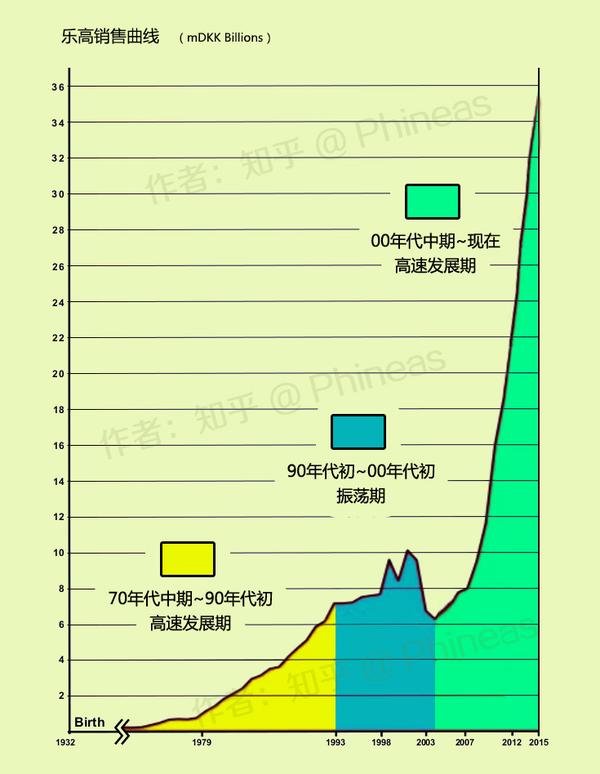

在过去十年里,乐高 (LEGO) 都做了什么使得净利润增长 32 倍,每年营收也长时间保持两位数增长?

FROM: https://www.zhihu.com/question/28383329

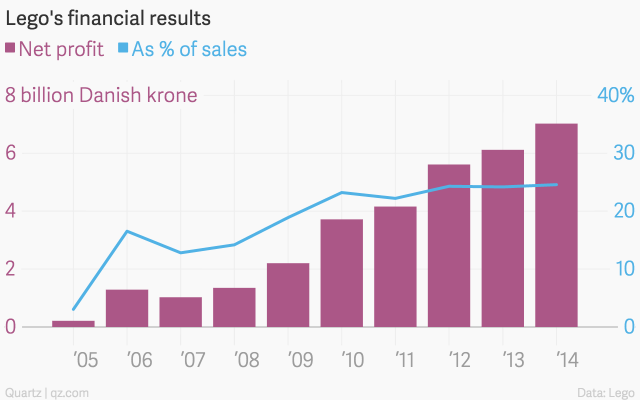

看到 2005 年财报的 net profit 是 2.14 亿丹麦克朗,而 2014 年这个数字是 70 亿克朗。

看到 2005 年财报的 net profit 是 2.14 亿丹麦克朗,而 2014 年这个数字是 70 亿克朗。

现在乐高在玩具市场上也把芭比娃娃和孩之宝甩在了身后1、重整产品线,留下真正赚钱的产业,砍掉头脑发热的产物,恢复创新的正常节奏从产品到周边产业都一样。在70到90年代有过创意井喷期,啥都能上市,丢弃拼砌的传统优势,天马行空,不少产品还蛮奇葩。不信看下图,芭比系列,你信这是乐高么?

婴儿玩具PRIMO、塑料玩具ZNAP、针对于女孩的类似于芭比娃娃的SCALA系列、网络大师机器人套装、防卫者系列、试图取代传统乐高人仔的杰克斯通系列,这些耗费成本且销量不佳的产品后来全部停售。

除了产品以外,乐高鼎盛时期对周边产业的扩展也有点丧失理智,除了乐高主题公园一直运营到现在,其他很多3D乐高数据库、拼砌指令这些周边的东东也都砍掉了,不是说这些项目毫无成就,只是节奏太激进。停止了揠苗助长之后,乐高的颓势已经有所好转。而在之后,乐高扩展周边产业的步子慢了很多也谨慎了很多。

2、削减成本,从制造到人力

在产品方面,在疯狂扩张期,乐高积木有将近1.29万个零件,在发生危机之后减少到7000个。塑料开模是不小的成本,数量少了,但是其实更能发挥想象力。在人力方面,一个比隆工厂就砍掉了1000+号员工。乐高掌权者的变更、管理层换血、股权变化这些就更复杂一些,暂且不谈(其实是因为这个我也不太懂哈哈哈哈)。

3、2013年的乐高大电影

上面也有人提到了乐高大电影,确实牛逼啊,这动画电影不光是拍给熊孩子看的!能把品牌嵌入电影还不惹人讨厌,也就乐高能干得出来,这简直就是个巨大的品牌广告片!段子够逗逼,乐高人仔的渲染非常细腻,关键是结尾确实完美植入了品牌理念。一部电影,转化成了实实在在的巨额销量,攒新粉丝的效果惊人,14年上半年因为电影提振,销量直涨11%。乐高大电影还会有2,就是不知道大陆会不会引进。

上面也有人提到了乐高大电影,确实牛逼啊,这动画电影不光是拍给熊孩子看的!能把品牌嵌入电影还不惹人讨厌,也就乐高能干得出来,这简直就是个巨大的品牌广告片!段子够逗逼,乐高人仔的渲染非常细腻,关键是结尾确实完美植入了品牌理念。一部电影,转化成了实实在在的巨额销量,攒新粉丝的效果惊人,14年上半年因为电影提振,销量直涨11%。乐高大电影还会有2,就是不知道大陆会不会引进。

4、教徒式的忠诚粉丝

这点太重要了,除了苹果之外,还没有哪个品牌能够像乐高那样拥有那么多的忠实粉丝。爸妈玩,带着孩子玩,一代接一代,乐高情况最不好的时候,全球粉丝有过各种自发的支持活动。乐高自己也知道粉丝、粉丝的体验对自己有多重要,一直坚守玩具的品质,这几年开了ideas平台,投票过万的粉丝作品经过评审就可以投产发售,对粉丝是很好的鼓励和振兴。

5、其实还有挺多其他的,NXT机器人神马的,持续主推电影合作产品神马的,断断续续的零零散散的回头想到再补充,大致以上足够大家随便看看~

备注:以上资料很多来自《乐高:创新者的世界》一书和《透过乐高创新兴衰史看文化产业的未来》的论文,简略的提炼了一些主要观点,感兴趣的小伙伴可以看看!

看到 2005 年财报的 net profit 是 2.14 亿丹麦克朗,而 2014 年这个数字是 70 亿克朗。现在乐高在玩具市场上也把芭比娃娃和孩之宝甩在了身后1、重整产品线,留下真正赚钱的产业,砍掉头脑发热的产物,恢复创新的正常节奏从产品到周边产业都一样。在70到90年代有过创意井喷期,啥都能上市,丢弃拼砌的传统优势,天马行空,不少产品还蛮奇葩。不信看下图,芭比系列,你信这是乐高么?

婴儿玩具PRIMO、塑料玩具ZNAP、针对于女孩的类似于芭比娃娃的SCALA系列、网络大师机器人套装、防卫者系列、试图取代传统乐高人仔的杰克斯通系列,这些耗费成本且销量不佳的产品后来全部停售。

除了产品以外,乐高鼎盛时期对周边产业的扩展也有点丧失理智,除了乐高主题公园一直运营到现在,其他很多3D乐高数据库、拼砌指令这些周边的东东也都砍掉了,不是说这些项目毫无成就,只是节奏太激进。停止了揠苗助长之后,乐高的颓势已经有所好转。而在之后,乐高扩展周边产业的步子慢了很多也谨慎了很多。

2、削减成本,从制造到人力

在产品方面,在疯狂扩张期,乐高积木有将近1.29万个零件,在发生危机之后减少到7000个。塑料开模是不小的成本,数量少了,但是其实更能发挥想象力。在人力方面,一个比隆工厂就砍掉了1000+号员工。乐高掌权者的变更、管理层换血、股权变化这些就更复杂一些,暂且不谈(其实是因为这个我也不太懂哈哈哈哈)。

3、2013年的乐高大电影

上面也有人提到了乐高大电影,确实牛逼啊,这动画电影不光是拍给熊孩子看的!能把品牌嵌入电影还不惹人讨厌,也就乐高能干得出来,这简直就是个巨大的品牌广告片!段子够逗逼,乐高人仔的渲染非常细腻,关键是结尾确实完美植入了品牌理念。一部电影,转化成了实实在在的巨额销量,攒新粉丝的效果惊人,14年上半年因为电影提振,销量直涨11%。乐高大电影还会有2,就是不知道大陆会不会引进。4、教徒式的忠诚粉丝

这点太重要了,除了苹果之外,还没有哪个品牌能够像乐高那样拥有那么多的忠实粉丝。爸妈玩,带着孩子玩,一代接一代,乐高情况最不好的时候,全球粉丝有过各种自发的支持活动。乐高自己也知道粉丝、粉丝的体验对自己有多重要,一直坚守玩具的品质,这几年开了ideas平台,投票过万的粉丝作品经过评审就可以投产发售,对粉丝是很好的鼓励和振兴。

5、其实还有挺多其他的,NXT机器人神马的,持续主推电影合作产品神马的,断断续续的零零散散的回头想到再补充,大致以上足够大家随便看看~

备注:以上资料很多来自《乐高:创新者的世界》一书和《透过乐高创新兴衰史看文化产业的未来》的论文,简略的提炼了一些主要观点,感兴趣的小伙伴可以看看!

我来试着回答一下05~09年那波动的净利润......那几年Lego的大动作如下:04年,全球第五大玩具制造商Lego集团与电子制造服务提供商Flextronics(伟创力)签订长期协议,外包模型、组装、包装和运输(modeling, assembly, packaging and distribution)以期降低…

我来试着回答一下05~09年那波动的净利润......那几年Lego的大动作如下:04年,全球第五大玩具制造商Lego集团与电子制造服务提供商Flextronics(伟创力)签订长期协议,外包模型、组装、包装和运输(modeling, assembly, packaging and distribution)以期降低…

我来试着回答一下05~09年那波动的净利润......

那几年Lego的大动作如下:

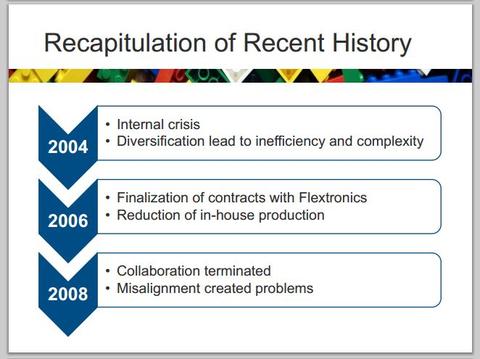

04年,全球第五大玩具制造商Lego集团与电子制造服务提供商Flextronics(伟创力)签订长期协议,外包模型、组装、包装和运输(modeling, assembly, packaging and distribution)以期降低成本提高利润。当时Lego认为外包约80%产品生产和关闭大部分高人力成本国家的生产基地将大幅降低公司生产成本。然而4年后,因为全球供应链管理上的力不从心,Lego终止了协议并重开了在欧洲的生产基地。再1年后,通过管理层重组和优化供应链,标准化生产,公司内部流程更新等,Lego重新走上了稳健发展的道路。

---------------------------------------------------------------------------------------------------------------------------------

纵观外部环境对Lego的影响:

那几年Lego的大动作如下:

04年,全球第五大玩具制造商Lego集团与电子制造服务提供商Flextronics(伟创力)签订长期协议,外包模型、组装、包装和运输(modeling, assembly, packaging and distribution)以期降低成本提高利润。当时Lego认为外包约80%产品生产和关闭大部分高人力成本国家的生产基地将大幅降低公司生产成本。然而4年后,因为全球供应链管理上的力不从心,Lego终止了协议并重开了在欧洲的生产基地。再1年后,通过管理层重组和优化供应链,标准化生产,公司内部流程更新等,Lego重新走上了稳健发展的道路。

---------------------------------------------------------------------------------------------------------------------------------

纵观外部环境对Lego的影响:

- 政治:

- 出口欧盟和美国的税负增加导致售价提高;

- 不同国家对玩具的尺寸、材料不同,增加Lego的设计和生产压力。

- 经济:

- 08年全球经济危机开始,作为主要顾客的中产阶级家庭收入减少,玩具支出自然相应减少;随着经济复苏,中产阶级也逐渐增加了部分支出;

- 发展中国家为了吸引外资,提供了良好的投资条件,使得Lego对在海外设立新生产基地重拾信心。

- 社会文化:

- 信息时代的孩子们对互联网和电子游戏的兴趣更大;家长也乐于尝试使用教育类应用;

- 孩子们很忙:不少孩子在课业之外被家长送去参加各种兴趣班,使得他们也许没空玩或者对自己学得东西更感兴趣而不玩Lego了。

- 技术:

- 随着技术的发展,Lego要求的产品2毫米(micrometer)误差更容易被达到了;Lego的自家生产机器性能也得到了大幅度提升;

- 智能手机和无线网络的普及,为Lego带来了新的创意。

- 生态

- 作为一家优秀的历史悠久的不上市的公司,Lego一直坚持对产品品质和CSR的追求,随着公众对公司csr的注重,对Lego这样一直保有此种发展模式的公司来说是好事;

- 法务

- 由于产品的易模仿性,Lego在世界各地有无数的盗版和仿制品,自然也产生了大量的版权官司。不同国家对版权的保护程度不同。官司影响了Lego的声誉并增加了法务支出。

- 新进入者的竞争:中等

- 通过几代人的努力,现存的几大玩具制造商已经达到了他们的economic of scale.新进入者不太可能从全行业的角度和现有大品牌竞争。

- 在快速变化和竞争激烈的玩具行业,建立品牌相对优势的方法一是建立自己的独特品牌,如Lego的砖块;二是通过取得Star wars, Harry Porter之类拥有大量粉丝群体的品牌的授权。或者这些品牌会自行发展代工工厂。

- 供应商的议价能力:中/低

- Lego的供应商主要来自3个方面:化学品、模具、电影公司(授权)。

- 买方的议价能力:中/高

- 个人买家:中

- 集团买家如Walmart:高

- 替代品竞争:高

- 电子游戏如任天堂;Mega&Mattel的战略合作(2014年Mattel已收购Mega)

- 同行竞争:除了Lego的仿制者以外,Mattel, Hasbro一类同样的玩具行业全行业玩家和Lego在玩具、游戏、主题乐园有全面竞争。

- 2003到2004年之间,正是乐高(Lego)这个创立已70年企业的历史最低点,连续2年销售暴跌,利润亏损,每个人都在想,明天是不是我们就要看到破产通告?——虽然从2015年的现在看过去,那一刻,不过是又一轮辉煌的起点,但在那时,乐高的第三代家族接班人凯尔德·科尔克·克里斯蒂安森是绝望的。

凯尔德接班20多年,他知道这个时代不属于他了。他赶走了前任CEO,那位奋力十载却没能拯救乐高的悲剧人物。同时提拔了两只左膀右臂,一位叫做克努,营销背景,一位叫做奥夫森,财务背景。而正是这次壮士断腕般悲壮的换帅,为乐高开启了新一轮的伟大征程。

改革的序曲,第一步,熔炼心法,大道至简。

公司比以前大太多了,我们需要新的、有效的管理手段。

前文说到,这左膀克努,右臂奥夫森,两人一个擅长营销,一个擅长财务,凑在一起,他们认为:大企业需要品牌,大企业需要财务控制。可是说来容易做来难。什么是品牌?什么是财务控制?

不管是消费者,还是员工。他们都希望事情简单,对员工而言,你的一套管理办法即便有效,但太过于复杂、繁缛,那么他们倾向于抵制,至少不会积极去执行。同样的,你的财务管理,也许每个会计能头头是道,可对于员工来说,是不能承受之负担。

克努和奥尔森,决定,树立一个标杆,去简化他们的管理,激发员工的积极性。于是推出了创造性的13.5的概念。

13.5原则:“乐高从今天起,每一个产品,它的销售利润率必须大于或者等于13.5%这个基准。”对市场负责,否则淘汰——这是乐高企业几十年来第一次树立这么一个清晰而简单的企业行为准则。

这不禁令我们想起了屈臣氏著名的26周原则:“屈臣氏对新进品牌在第十三周进行库存评估,如果库存周转天数超过26周,则下架停售”。在这一条准则之下,乐高有了几个明显的变化。

一方面,设计师受到了约束,不可以再随心所欲的设计一些自嗨型的积木,另一方面,又极大程度释放了设计师——是的,只要热卖,只要符合成本,你可以任意发挥——这像极了若干年后的一个叫做twitter的机制,我限制你140字,但是在这个范围里,是你的王国。于是在接下来的10年里,乐高设计得到了井喷式的发展。

你说,天呐,这么神奇吗?——其实中国历史上有一个同样神奇的案例。商鞅变法强大了秦国,而这一法度的核心是什么?是军功爵制,士兵们每获取一个敌人的人头(首),就可以官升一级。从而有了一个耳熟能详的词汇:首级。

如果说13.5原则是品牌和财务对内的体现,那么对外,对市场和消费者,乐高反思了它过去十年的产品线,它觉得,也必须要做出一些改变。

第二步,重新定义积木。积木没有被电子游戏淘汰,它有永恒的生命力。

在2004年前,乐高在做什么?电脑游戏和电影工作室、乐高教育中心、新奇特玩具(甚至有芭比那套玩意)……砍掉,统统砍掉,因为他们不符合13.5的原则。那么,乐高的产品中心该向哪里转移呢?

~~~回归原点,得宝系列重生~~~

在此前的乐高振荡期,一个被广为接受的观念是,电子游戏时代来了,积木将被淘汰。正是在这种思潮下,乐高的一个王牌产品得宝系列(0-5岁适用),被废弃停产了。可是这真的对吗?

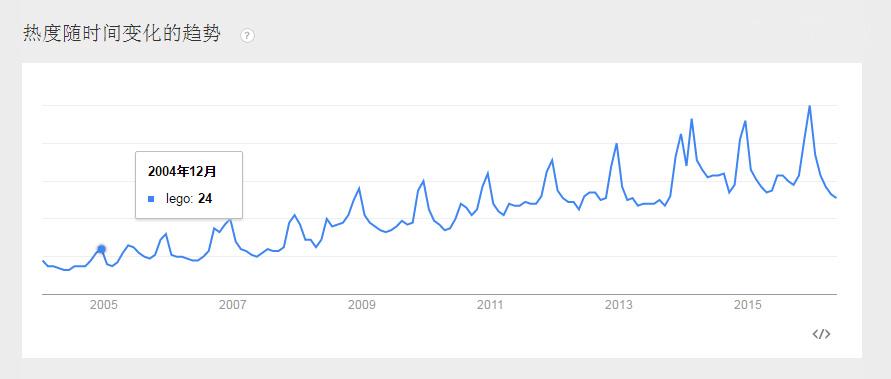

上图是全球趋势。乐高的关注度从2004年至今,有2个明显的特点,一是持续上涨,而是几乎每个高峰点都是圣诞季。ok,一个很大程度上作为礼物的积木产品,它抛弃了专为幼儿的得宝系列?太荒唐了吧。

你问,得宝真的好吗,它有竞争对手吗? 从数学角度来说,如果你有六块八颗凸起的乐高长方体积木,可以砌出一亿种组合。

从数学角度来说,如果你有六块八颗凸起的乐高长方体积木,可以砌出一亿种组合。

从人性角度来说,拼接真的会上瘾。

——这是得宝的天然优势。

乐高设计师在13.5原则引导下,面向广大孩子,推出了全新的得宝系列。2005当年,实现了三倍的销售额,受到热捧。更有死忠粉热泪盈眶:看到得宝重生,我觉得我爱的乐高回来了。

虽然到今天得宝早已退出了乐高销售三甲。但这个系列,是一个细水长流的长青产品,是乐高的初心,也是粉丝的摇篮。

在得宝的这场战役里,新任的左膀右臂收货了信心,同时他们也看到了与时俱进的魅力。满足消费者需求,不是把消费者请到公司来做焦点访谈,而是应该我们自己,去到广阔的真实世界,去仔细观察消费者的实际形态。

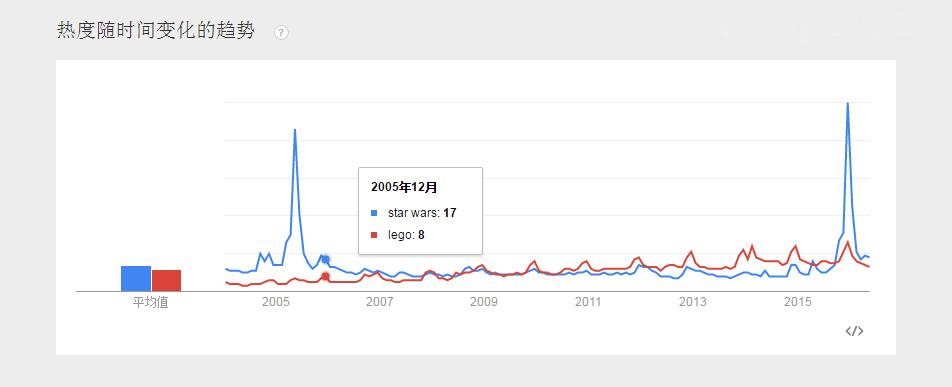

~~~星球大战系列再临~~~

星球大战系列,是乐高热销了几十年的产品。2005年,迎来了星战电影第五集的公映。

我们对比前面的乐高全球趋势,看看星战有多热。

天哪。在大部分的时间里,星战这一个电影系列,居然比乐高还热乎。了解欧美的人知道,星战那是和披头士一样,影响了一代人的伟大作品。乐高显然不能忽视这一点。在得宝上尝到甜头的团队,重新设计(包括复刻)了一系列星战相关周边。

我们来看著名的星战飞行器“千年隼”号(编号7965,2011年推出,是10179的复刻缩小版)在美国亚马逊商城的购买评论。

This is a massive and amazing set. I'm a huge fan of the original trilogy and lego so have been wanting to get a Millennium Falcon set for several years. Unfortunately I found most of them either far to expensive, or simply not worth the asking price. This one finally hit the sweet spot for me…… is nearly perfect……这是一个重大且惊艳的套组。我是星战最初三部曲以及乐高的超级粉丝,所以希望得到一个千年隼套组已经很多年了。不幸的是,我发现他们大多要么太过昂贵,或者干脆不值得的问价。这一次终于击中我要害了……几乎是完美的……

(130个人觉得此评论很赞)

Played with this at a friend's house. He got it for his birthday and took him more than 5 hours to build, and he wouldn't let us take it apart to rebuild! It is impressive! The details on the outside is just like the movie. The fold out panels open the reveal the inside where the minifigs can act out the movie scenes. The size of the Falcon is just right to fly around, not too heavy or bulky, and is actually quite sturdy compared to other Lego sets.在朋友家玩这个,他是作自己的生日礼物的,还花了5个小时去搭建它,还不让我们拆了玩!令人印象深刻!它外面的细节和电影里一模一样……

(86个人觉得此评论很赞)

你说,你知道了,这不就是大IP吗!竞争对手也可以去活捉另外的IP哦!分分钟抢你的粉丝,抢你的市场。

真的吗?

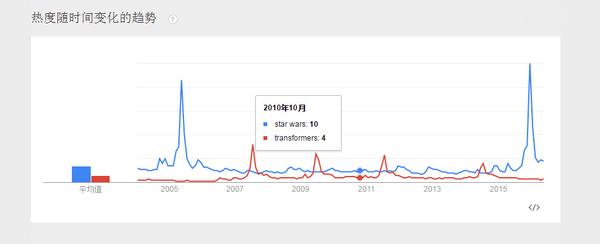

乐高有一个死对头,叫做孩之宝。现在乐高是玩具业老大,可以前孩之宝是老大。孩之宝看到星战很好卖,他也想学习,于是他看中了变形金刚。同样是有广泛受众、特别受男性喜爱。可是呢。 我们注意到:

我们注意到:

1、每个关注热点都是受到电影公映的带动。

2、星战的影响力远远大于变形金刚。

3、星战电影公映结束后,热度维持在一定水平不再衰减。

4、变形金刚电影公映结束后,热度衰减很快。

我们再来看双方公司对于IP题材的深入挖掘。

在youtube搜索“lego star wars”(乐高星球大战),大约156万条结果。排第一的是同人类作品:

在youtube搜索“Hasbro Transformers”(孩之宝变形金刚),大约16万条结果,大都是游戏、产品展示。

所以,不论是从题材本身热度、持续性、可挖掘性,星战都全面超越变形金刚。对此,我们只能说:星战不是IP,星战就是星战。这一条大腿,被乐高抱住了,特别是从2000年以来,星战前传和星战后续,一共6部的持续播出,必将给乐高带来持续助力。

~~~女孩系列咸鱼翻身~~~

除了以星战为代表的授权类产品系列。乐高也从未放弃过原创版权的努力。

如果说星战是男孩的最爱。那么乐高还想要一个女孩的王牌产品。

70年代,发布Homemaker套组,几年后下架。

1979年,发布Scala定制珠宝 卷心菜美人鱼 猜猜这是什么?

卷心菜美人鱼 猜猜这是什么?

乐高全球CEO的名片(读音是姚根儿,后面还会讲他),在背面印着姚根儿的座机和email。这个人偶的脖子,腿,胳膊,和手都是都是可以拆卸可以转的,连头发都可以转可以拆下来,所以转到90°的时候,CEO的眼睛会被挡住而风中凌乱,时尚时尚最时尚。

换了那么多名片,我承认当我拿到这“张”名片的时候忍不住说“wow”。这个小细节让我觉得很能代表这个公司,它就是卖“有趣”的。对于一直在讲智造升级的很多制造企业来说,乐高就是一个故事大师,不知道高明到哪去了。

一些亮瞎的事实是:

2014年乐高在它所有的市场都是两位数的销售增长,而其他的企业都是个位数

乐高的利润和净利润都是两位数的增长,这几年的势头都差不多

乐高的小塑料片都是自己做的,没有外包!

为什么乐高卖的这么好?

乐高卖的其实是背后的一整套玩乐体系。

每一年,乐高生产500多亿个积木,可以连到月球还多一百亿来块,可是可以说乐高卖的可不是塑料片,这个耦合的塑料片可是1958年就申请专利了,到现在还是一样的技术,没变过。从 1958 年开始,无论何时何地乐高生产的所有组件都可以完全兼容。

电子玩具刚刚兴起的时候,乐高不是没傻眼。回到 2000 年面对这些科技领域的挑战者,乐高和其他传统玩具厂商一样感到慌乱。于是,乐高开始模仿迪士尼,不仅在欧美地区建造庞大的乐高乐园,还将业务触角延伸至电子游戏、服装、学习用品等。多元化并未取得预期成效,反而使乐高的产品与形象变得模糊,导致乐高在 2003 年前后陷入亏损泥淖,营收下降 25% ,全年亏损额达到史无前例的 2.3 亿美元。亏损状态一直持续至 2004 年,公司甚至差点倒闭。

现在姚根儿出场了。

麦肯锡管理顾问出身的克努德斯道普(姚根儿)担任 CEO 后,第一件事就是回归玩具创造的核心业务,将乐高乐园与衍生产品经营进行外包,更为重要的是,在乐高产品中引入越来越多的故事元素。

除了经典的无标准拼砌系列,乐高开始推出根据 DC 漫画( DC Comics )和漫威( Marvel )中的形象和场景打造的超级英雄系列产品。可以看到的明显变化是,为了获取大量广受欢迎的动漫形象和故事场景的授权——别忘了,这些动漫形象吸引的,不仅仅是儿童——乐高在授权上所花费的资金,从 2005 年的不足 3 亿丹麦克朗激增到 2012 年的 15.06 亿丹麦克朗。

乐高是怎么包装新产品的?

乐高在制作每个系列产品时,都会用一个故事作为主题进行贯穿,并用动漫、游戏、网站、社交平台等一系列方式去推广在产品背后的故事属性。

以 2013 年上市的新产品系列气功传奇 CHIMA 为例,乐高找来了纪录片导演 John Derevlany ,请他为 CHIMA 写一部 30 集的动漫连续剧,讲述了 8 个动物部落,包括无敌狮,鳄霸王,狼武士等动物互相格斗的故事。2013 年 1 月,这部动漫连续剧开始在美国卡通娱乐网站 Cartoon Network 定期播出,每集都吸引了百万以上观众。在这之后,乐高接着让 Derevlany 继续撰写相关的 4D 电影脚本,这部电影将在乐高乐园上映。

除了动漫和电影,乐高还以这个故事为内核,让华纳兄弟旗下的游戏开发商 TT Games(这家公司在 2007 年被华纳兄弟收购之前,是乐高的游戏开发商)为这款产品制作了衍生的三款游戏,游戏中的英雄角色均采用乐高玩具形象。

其中一款游戏—— CHIMA 传奇之拉法尔的旅程——由华纳兄弟在索尼与任天堂的游戏掌机平台进行发售,在游戏中,不同部落的动物拥有不同的能力,例如狼可凭嗅觉找到隐藏物品,狐狸可以钻进狭小的空间,如果你想拥有这些特殊的能力,那需要付出不菲的价格。当然,这些动漫剧集与游戏都被整合在气功传奇的网站上了。

在这样的故事情境铺垫下,乐高又可以不断推出气功传奇相关的产品,从不同部落场景,不同英雄的拼装人偶,到故事中出现过的回旋飞车、战机,每盒都有不同的玩法。

乐高是怎么设计新产品的?

一边是贴近孩子们的内心故事世界,一边是丰满而富有现实的体验,这让乐高新产品常常能收到来自全世界孩子们,甚至是那些超级大龄粉丝们发现的“ wow ”惊呼声。

乐高在丹麦比隆的产品研发总部,就像一个儿童乐园,墙壁是天空般的蓝色,会议室是柠檬黄色,而沙发则是亮眼的玫红。展示柜上摆满了乐高积木拼砌出的各种造型,例如城堡,汽车等,一只巨大的铁皮滑梯可以让员工直接从二楼冲向一楼。每周两次,许多来自幼儿园、学校,甚至是员工的孩子,会来到这里,他们可以随便在公司里面跑来跑去,快乐地从滑梯上滑下来,而乐高的产品设计人员,则在开心陪玩的过程中实现了互动调研。

没有什么方式比让孩子们做简单的选择题更加有效:当乐高在一款会动的小卡车与一款车身更大、功能更全但不会动的大卡车之间犹豫时,孩子们一齐扑到了小卡车上。显然,孩子们已为这款新产品的市场前景做出了答案。

也只有通过孩子的思维,才更可能发现这些提供给他们自己玩耍的玩意有哪些可完善之处。

乐高 2014 年版本的“监狱”产品,比 2011 年版本除更加丰富建筑细节,还多了一辆小汽车,这是因为乐高设计总监 Ricco 带着这款产品在全世界的几个城市中与儿童互动时,上海的一个小朋友提出“为什么监狱的外面只有警车?那么犯人即使逃出监狱也肯定没法走远,他必须开汽车逃走才能成功越狱”。

当然,想象力固然重要,符合现实的体验同样必不可少。

乐高分布在全球 24 个国家和地区的 180 名设计师,常常要深入各个行业,获取真实的体验。例如设计消防车系列,设计师们曾经到消防队去当一天的见习消防员;设计跑车,设计师们会特地去赛道上进行一场跑车挑战赛;设计太空船模型,Ricco 还在美国国家航空和宇宙航行局( NASA )的阿波罗 13 号任务控制中心体验,甚至开起了曾经登月的月球车。

乐高是怎么售卖产品的?

除了商场、专卖店的布点,在线平台的开发,社交平台的营销,乐高很注重体验营销。

比如说乐高教育

用乐高的各种积木玩具开发孩子们的智力,它是独立运营的,不以售卖产品为目的,但无疑是最好的营销了。乐高教育1980年就成立于丹麦,为全世界的教师和学生提供内容丰富、具有挑战性、趣味性和可操作性的学习工具和教学解决方案。

再比如说乐高的一些宣传活动

乐高教育的独特学习理念、教学指导、小组作业、教师培训、安全环保的学具、趣味性的比赛方式,使孩子们发挥出天生的创意力和想象力,培养团队精神、解决问题能力、应变能力、表达能力、社交能力等,帮助他们从容应对 21世纪所带来的新挑战。

乐高正在以前所未有的速度加快布局在国内的品牌体验活动。伴随着乐高在嘉兴的工厂奠基开工,乐高在嘉兴图书馆举办了一场体验活动,超过 1000 名小朋友在 4 天的时间内拼装 50 万块乐高积木,用想象力拼砌未来城市。在过去的一年中,乐高的主题活动“ build the world ”在中国举办了 16 场,而在中国设立区域办公室后,今年这一活动的数量将增加至 30 场。

暑假期间,乐高带来“卡车秀”,满载着多个主题产品的乐高卡车将停在城市中儿童较为密集的地方,例如商场或公园里的一块场地,有不同的区域,包括幼儿区或女孩们的玩具系列,让小朋友们随意拼搭、比赛。

像前面一些答主说的拼砌,也是一种非常独特的营销。乐高世界杯是从1988年开始举行的。比如拼出世界著名建筑,这些叹为观止的作品都让人过目不忘。

乐高的发展或许说明了,逗比才能赢得全世界。

姚根儿挺帅的不是么?

姚根儿挺帅的不是么?

猜猜这是什么?乐高全球CEO的名片(读音是姚根儿,后面还会讲他),在背面印着姚根儿的座机和email。这个人偶的脖子,腿,胳膊,和手都是都是可以拆卸可以转的,连头发都可以转可以拆下来,所以转到90°的时候,CEO的眼睛会被挡住而风中凌乱,时尚时尚最时…

猜猜这是什么?乐高全球CEO的名片(读音是姚根儿,后面还会讲他),在背面印着姚根儿的座机和email。这个人偶的脖子,腿,胳膊,和手都是都是可以拆卸可以转的,连头发都可以转可以拆下来,所以转到90°的时候,CEO的眼睛会被挡住而风中凌乱,时尚时尚最时…

Subscribe to:

Posts (Atom)