http://klse.i3investor.com/blogs/sumato88/122720.jsp

Wow, I am so surprised that many ppl don't get my logic and my

calculations for Petronm's 1Q17 profit. Let me put things in order and

hopefully you can see it now.

1) Malaysia operations (listed co + 2 non-listed co in Malaysia owned

by Petron Corp) reported Peso 1.5bn net profit in 1Q17, +335% yoy. So,

1Q16 net profit from Malaysia operation = Peso 345m

Workings

a) (1Q17 profit /1Q16 profit) - 1 = yoy growth

B) (1500/345) - 1 = 335% (In case you are still confuse, ask

yourself, what's the yoy growth rate if your profit increase from 100 in

1Q16 to 150 in 1Q17? The answer is 50% right? Pls apply the same

formula.)

2) Peso 345m net profit in 1Q16 equal to RM30m. This was the profit

from Malaysia operation in 1Q16, including 2 non-listed co. So what's

the profit belong to non-listed co? Petronm (listed co) reported RM16.6m

net profit in 1Q16, so

A) Petronm's 1Q16 profit + 2 non-listed co 1Q16 profit = RM30m

B) RM16.6m + 2 non-listed co 1Q16 profit = RM30m

C) 2 non-listed co 1Q16 profit = RM30m - RM16.6m = RM13.4m

3) Given that 2 non-listed co is involved in fuel marketing and

retailing (basically means petrol stations la), the profit growth should

be steady due to fixed margin, so it should grow in tandem with sales

volume growth. Petron Corp mentioned Malaysia sales volume + 6% yoy in

1Q17, so we can safely assume 2 non-listed co profit grow 10% yoy in

1Q17, from RM13.4m to about RM15m.

4) So how much of RM130m or Peso 1.5bn 1Q17 profit attributes to Petronm?

RM130m - RM15m (2 non-listed co estimated profit) = RM115m (42.6 EPS)

My final advise, if you still don't understand, please don't buy any

stocks anymore as stock investment could be way too complicated for you.

Saturday, May 13, 2017

Thursday, May 11, 2017

Petronm: A Simple Math, 5x PE even after the 100% rally YTD?

First, I would like to congrats to all the shareholders of Petronm who do not sell the shares due to oil price volatiliy. The coming quarter results will be a reward to the believers. As some of you may have aware, Petron Corp (the parent co of Petronm) has released a press statement on 8 May 2017 and mentioned that net income from Malaysia operation in 1Q17 surged 335% to Peso 1.5bn. Many are guessing the profit that the listed co, Petronm will report in the upcoming 1Q17. Well, let me try to solve this simple math.

1) Peso 1.5bn = RM130m net income in 1Q17, given that Petron Corp didn't mention this is net income after minority, we can safely and conservatively assume this is the Malaysia operation net income before minority.

2) 335% yoy increase implied 1Q16 net income from Malaysia operation = Peso346bn or about RM30m

3) Both of these numbers include 2 non-listed sister co that Petron Corp owns in Malaysia, hence, we need to figure out how much is the profit belongs to the non-listed entities.

4) Petronm reported RM16.6m net income in 1Q16, as a result, non-listed sister companies should have contributed RM13.4m in 1Q16.

5) Given that the 2 non-listed sister companies are in fuel marketing and retailing biz, it is safe to assume that the profit growth is likely to be very steady, rise according to the volume + some margin improvement due to operating leverage. As Petron Corp mentioned Malaysia sales volume +6% yoy in 1Q17, we can assume 10% net income growth for non-listed sister co for 1Q17, which probably works out to about RM15m profit.

6) If you minus RM15m out of RM130m net income reported by Malaysia operation, we can get a profit estimate of RM115m for Petronm in 1Q17, this is a whopping 7-fold increase from 1Q16 and another quarter of RM100m profit!

7) I understand that the crack spread is still relatively stronger qoq in April and May to date. If this sustain throughout the 2Q17, we will probably see another RM100m profit in 2Q17, paving way for Petronm to achieve net cash position and record profit in 2017. Initially I was looking at RM300m profit in 2017, but now it seems to be easily beaten if Petronm can achieve RM200-230m profit in 1H17.

In conclusion, I think there is still plenty of upside from current share price, even though the stock had a good rally YTD (almost 100%). At 5x PE (assuming RM400m profit, +63% yoy), I personally think this stock is too cheap to sell.

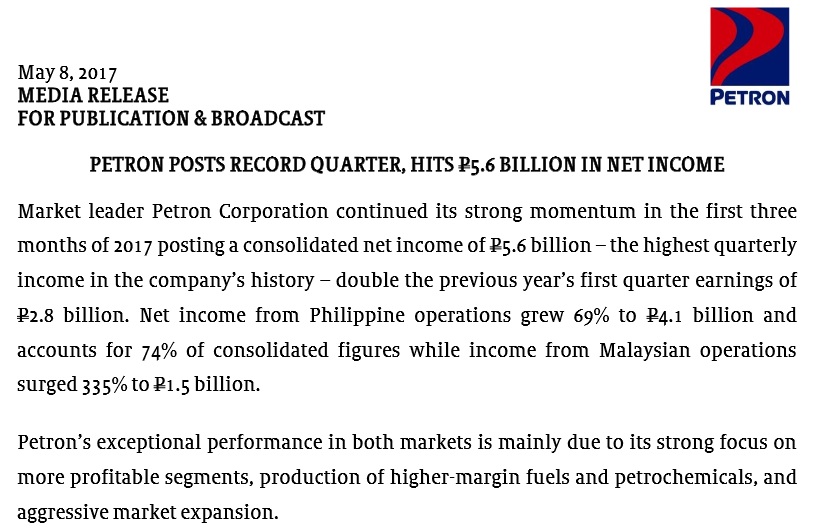

PETRON Corp's Media release entitled "PETRON POSTS RECORD QUARTER, HITS P5.6 BILLION IN NET INCOME".

1) Peso 1.5bn = RM130m net income in 1Q17, given that Petron Corp didn't mention this is net income after minority, we can safely and conservatively assume this is the Malaysia operation net income before minority.

2) 335% yoy increase implied 1Q16 net income from Malaysia operation = Peso346bn or about RM30m

3) Both of these numbers include 2 non-listed sister co that Petron Corp owns in Malaysia, hence, we need to figure out how much is the profit belongs to the non-listed entities.

4) Petronm reported RM16.6m net income in 1Q16, as a result, non-listed sister companies should have contributed RM13.4m in 1Q16.

5) Given that the 2 non-listed sister companies are in fuel marketing and retailing biz, it is safe to assume that the profit growth is likely to be very steady, rise according to the volume + some margin improvement due to operating leverage. As Petron Corp mentioned Malaysia sales volume +6% yoy in 1Q17, we can assume 10% net income growth for non-listed sister co for 1Q17, which probably works out to about RM15m profit.

6) If you minus RM15m out of RM130m net income reported by Malaysia operation, we can get a profit estimate of RM115m for Petronm in 1Q17, this is a whopping 7-fold increase from 1Q16 and another quarter of RM100m profit!

7) I understand that the crack spread is still relatively stronger qoq in April and May to date. If this sustain throughout the 2Q17, we will probably see another RM100m profit in 2Q17, paving way for Petronm to achieve net cash position and record profit in 2017. Initially I was looking at RM300m profit in 2017, but now it seems to be easily beaten if Petronm can achieve RM200-230m profit in 1H17.

In conclusion, I think there is still plenty of upside from current share price, even though the stock had a good rally YTD (almost 100%). At 5x PE (assuming RM400m profit, +63% yoy), I personally think this stock is too cheap to sell.

PETRON Corp's Media release entitled "PETRON POSTS RECORD QUARTER, HITS P5.6 BILLION IN NET INCOME".

Market leader Petron Corporation continued its strong momentum in the first three months of 2017 posting a consolidated net income of P5.6 billion – the highest quarterly income in the company’s history – double the previous year’s first quarter earnings of P2.8 billion. Net income from Philippine operations grew 69% to P4.1 billion and accounts for 74% of consolidated figures while income from Malaysian operations surged 335% to P1.5 billion.

Petron’s exceptional performance in both markets is mainly due to its strong focus on more profitable segments, production of higher-margin fuels and petrochemicals, and aggressive market expansion.

In the Philippine retail segment, Petron’s volumes grew by another 6% while its LPG and Lubricants businesses grew by 5% and 16%, respectively. Currently, Petron has the highest network count with about 2,300 service stations – more than its next three competitors combined – which retail its cutting edge fuels and serves as outlets for its other products and services.

Petrochemical export volumes more than doubled over the period allowing Petron to capture better margins from benzene, toluene, mixed xylene, and propylene. Meanwhile, exports of fuels were lessened as more volumes were sold locally as part of the company’s strategy to optimize margins.

The company’s Malaysian operations also experienced steady growth with domestic volumes growing by another 6%, fueled by double-digit growth from the Commercial and Lubricants sectors.

Petron’s exceptional performance in both markets is mainly due to its strong focus on more profitable segments, production of higher-margin fuels and petrochemicals, and aggressive market expansion.

In the Philippine retail segment, Petron’s volumes grew by another 6% while its LPG and Lubricants businesses grew by 5% and 16%, respectively. Currently, Petron has the highest network count with about 2,300 service stations – more than its next three competitors combined – which retail its cutting edge fuels and serves as outlets for its other products and services.

Petrochemical export volumes more than doubled over the period allowing Petron to capture better margins from benzene, toluene, mixed xylene, and propylene. Meanwhile, exports of fuels were lessened as more volumes were sold locally as part of the company’s strategy to optimize margins.

The company’s Malaysian operations also experienced steady growth with domestic volumes growing by another 6%, fueled by double-digit growth from the Commercial and Lubricants sectors.

Petronm: Growing evidence of record 1Q17

Spike in maintenance expected to boost oil refining margins

http://www.reuters.com/article/us-oil-refinery-maintenance-idUSKBN15G55W

http://www.reuters.com/article/us-oil-refinery-maintenance-idUSKBN15G55W

Reuters, 2 Feb 2017- Increased refinery maintenance in Asia and the Middle East is expected to boost profits for operators in other regions in the first half of this year, market watchers said on Wednesday.

Refineries worldwide ran hard during the past two years to capitalize on low oil prices, with Chinese refineries processing a record amount of crude in 2016, meaning that some units now have no choice but to carry out maintenance.

Outages in the first half will equate to nearly 1 million barrels per day (bpd) more than in the same period last year, speakers told the Platts Middle Distillates conference in Antwerp.

Though this is likely to help to clear the stocks of oil products such as diesel, gasoline and jet fuel that poured into the world's storage tanks over the past two years of excess, it is also likely to cut into demand for crude oil just as prices recover on the back of production cuts led by the Organization of the Petroleum Exporting Countries (OPEC).

Trading house Gunvor's chief economist, David Fyfe, said that he expects "healthy and robust" refinery margins in the first half of the year.

Gunvor data shows that maintenance in February and March will take close to an additional 1 million bpd offline compared with the same months in 2016.

Both Fyfe and James McCullagh, oil products analyst with Energy Aspects, said the bulk of the work will be concentrated in Asia and the Middle East, offering a reprieve to Europe's comparatively less advanced refineries, which have depended largely on demand -- or supply problems -- in other regions to underpin profits.

Energy Aspects expects Asian refineries alone to account for 900,000 bpd more in offline capacity in April, compared with the prior year, and 250,000 bpd more over first half of 2017. Those shutdowns, paired with diesel stocks in China that it estimates are near record lows, would underpin refinery profits in most regions, he said.

Fires and other issues at refineries worldwide this month suggest that many units are feeling the effects of the ramp-up in output over the past year or two.

"The strong margins have in a way stored up unplanned outages," McCullagh said.

This month's outages included Abu Dhabi National Oil Company's Ruwais refinery, two refineries in West Africa and others in India, Indonesia and Brazil.

S.Korea's S-Oil expects firm refining profits in 2017

http://www.cnbc.com/2017/02/01/reuters-america-update-1-skoreas-s-oil-expects-firm-refining-profits-in-2017.html

SEOUL, Feb 2 (Reuters) - South Korea's S-Oil Corp expects healthy refining profits this year, buoyed by growing demand for oil products in places such as China and Southeast Asia.

The country's third-largest oil refiner said in a quarterly earnings statement on Thursday that global oil demand would grow soundly in 2017, although the rate of increase could ease slightly from last year.

"Healthy margins are expected as 1.32 million barrels per day (bpd) of oil demand growth will outstrip an incremental net capacity increase of 574,000 bpd," the company said, referring to the profit margin on refining barrels of crude oil.

Inventory gains and a recovery in refining margins helped S-Oil, whose top shareholder is Saudi Aramco <IPO-ARMO.SE>, notch up a 444 billion won ($386 million) profit in the last quarter of 2016, compared with a loss of 42.9 billion won the year before.

S-Oil treasurer Shin Kwan-bae said on a call with analysts that the company expected the official selling price (OSP) for Arab Light crude, supplied by Saudi Arabia, to remain steady in Asia from last year.

He said that even if Middle Eastern crude supply drops in the wake of a deal by producers to curb output, Saudi Arabia would not want to harm its market share in Asia by increasing OSPs.

A company official said S-Oil planned to carry out less scheduled maintenances this year, limiting such work to a condensate fractionation unit (CFU) and a No.2 paraxylene unit. He did not give further details.

Industry sources have said S-Oil would shut down its No.1 residue hydro desulphurisation unit (RHDS) and crude oil refining unit in April for about a month.

S-Oil also said on Thursday that its 2018 expansion project was on track to complete in the first half of next year.

Under the project, the company will build a residual fuel oil upgrading system and an olefin production system that will churn out 405,000 tonnes of polypropylene a year, along with other products.

Asian Oil refinery margins jump on outages in Mideast, Asia

http://www.reuters.com/article/us-asia-crude-refineries-idUSKBN151183

Reuters, 17 Jan 2017- Several refineries in the Middle East and Asia have shut down in the past week due to fires and other technical problems, leading to a jump in profit margins for facilities still operating.

The higher Asian refining margins have beat back concerns that profits would fall as crude oil prices gained as the Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC producers began to implement their agreed production cuts from January to reduce global oversupply.

Besides the fires and other shutdowns, maintenance and repairs at refineries in Indonesia by Pertamina [PERTM.UL] and in Singapore by Royal Dutch Shell have further boosted oil product margins.

"Margins will be supported as these outages will affect the ability of the region to stock up before maintenance picks up in March," said Nevyn Nah, a fuel analyst at Energy Aspects in Singapore.

Profits for processing a barrel of Dubai crude at a Singapore refinery jumped to $7.64 a barrel on Jan. 16, the highest since Nov. 30, Reuters data showed.

(richDad) - PETRONM: More than 50% upside (PETRON CORP media release says 1Q earnings to TRIPLE)

1. Main business = oil refinery and retail. These descriptions are from their website which says “Petron Subsidiaries in Malaysia comprise of Petron Malaysia Refining & Marketing Bhd (formerly known as Esso Malaysia Berhad), a public listed company listed on Bursa Malaysia; Petron Fuel International Sdn Bhd (formerly known as ExxonMobil Malaysia Sdn Bhd); and Petron Oil (M) Sdn Bhd (formerly known as ExxonMobil Borneo Sdn Bhd). As a major and reputable company in Oil & Gas, our involvement in refining and retailing of world-class quality of petroleum products and related services, helps the country to meet its energy demands and contributes to the overall socio-economy advancements. Our robust petroleum marketing business that encompasses over 550 service stations nationwide bring high quality, clean energy products to motorists.”

In lay man term, the retail business is the petrol station that we see and possibly pump petrol. In order to get the oil to the station, they need to refine it first (from the crude oil). So, PETRONM is also involved in refining the crude oil to petrol and other products. If you ever wonder how many stations does PETRONM has, it is 550 from the website.

To fully understand what PETRONM does you can visit their website here

http://www.petron.com.my/web/site/slider/9

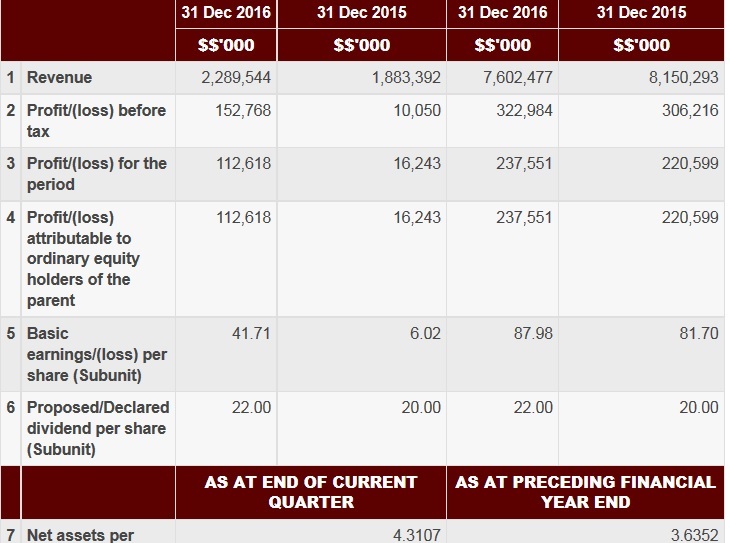

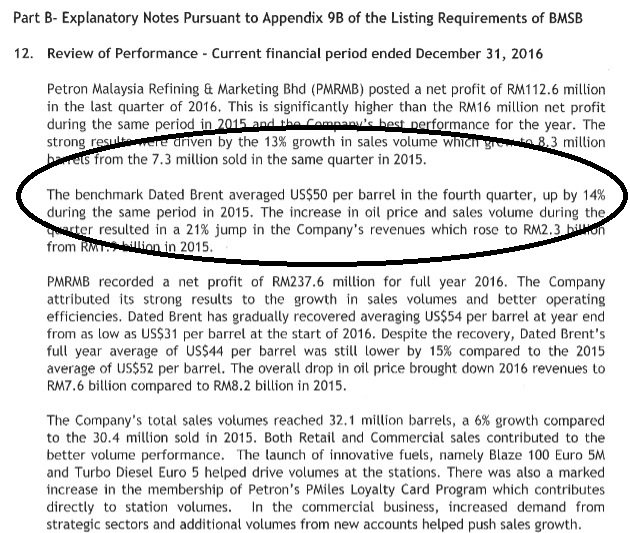

2. Stellar earnings growth in 4QFY16 (+593% to RM112.62m). Accordingly, EPS also jump 593% to 4171sen. Reason for the earnings surge can be seen below. It is mainly due to 13% increase in sales volume (which means this is operation improvement and is sustainable).

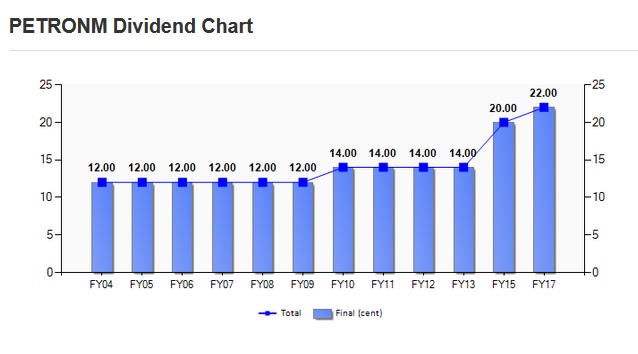

3. Consistent paid dividend (10 out of 11 years) in the past. FY16 dividend has increased by 10% to 22 sen (against 20 sen in FY16). The Company has consistently paid dividend in the past with only one miss in FY14 (but that one is due to loss in that financial year under previous management).

4. SUPER CATALYST = 1QFY17 earnings to triple??? Sometimes, you need to monitor global news as it is increasingly hard to make ALPHA GAIN from the market in Malaysia. Just three days ago, PETRON CORPORATION (parent company of PETRON MALAYSIA made an announcement of its 1Q profit which doubled. BUT the most important thing is it mentioned that

Income from Malaysia operation surged 335% to Peso 1.5 billion (about RM130m). AND Malaysia investors may not fully realize this because it is not annouced yet in the BURSA!!!

You can read the full Media Release from Singapore Exchange here

http://infopub.sgx.com/FileOpen/05%2008%2017%20-%20Media%20Release%20-%20Petron%20Posts%20Record%20Quarter%20Hits%20P5.6%20Billion%20in%20Net%20Income.ashx?App=Announcement&FileID=452503

5. Long term value is between RM12 to RM15 per share. There is more than 50% upside that I am looking at. I think that the Company is worth between 8x to 10x PE. The 8x PE is if you take oil and gas Company PE. While the 10x PE is the minimum for consumer sector PE. I think PETRONM is a mixture of O&G and CONSUMER because its petrol station business is basically similar to 7 ELEVEN. For FY17, the 1Q net profit is assumed at RM130m and I multiply this by 3 to get the full year earnings. I purposely ignore one quarter for conservativeness purpose in my calculation (that's why not multiplying by 4).

That gives me FY17 earnings of around RM390m (or RM1.45 of EPS).

8x PE * RM1.45 FY17 EPS = RM11.60 (round up to RM12)

10x PE * RM1.45 FY17 EPS = RM14.50 (round up to RM15)

For record keeping purpose, I am using last Tuesday closing price of RM7.97

In lay man term, the retail business is the petrol station that we see and possibly pump petrol. In order to get the oil to the station, they need to refine it first (from the crude oil). So, PETRONM is also involved in refining the crude oil to petrol and other products. If you ever wonder how many stations does PETRONM has, it is 550 from the website.

To fully understand what PETRONM does you can visit their website here

http://www.petron.com.my/web/site/slider/9

2. Stellar earnings growth in 4QFY16 (+593% to RM112.62m). Accordingly, EPS also jump 593% to 4171sen. Reason for the earnings surge can be seen below. It is mainly due to 13% increase in sales volume (which means this is operation improvement and is sustainable).

3. Consistent paid dividend (10 out of 11 years) in the past. FY16 dividend has increased by 10% to 22 sen (against 20 sen in FY16). The Company has consistently paid dividend in the past with only one miss in FY14 (but that one is due to loss in that financial year under previous management).

4. SUPER CATALYST = 1QFY17 earnings to triple??? Sometimes, you need to monitor global news as it is increasingly hard to make ALPHA GAIN from the market in Malaysia. Just three days ago, PETRON CORPORATION (parent company of PETRON MALAYSIA made an announcement of its 1Q profit which doubled. BUT the most important thing is it mentioned that

Income from Malaysia operation surged 335% to Peso 1.5 billion (about RM130m). AND Malaysia investors may not fully realize this because it is not annouced yet in the BURSA!!!

You can read the full Media Release from Singapore Exchange here

http://infopub.sgx.com/FileOpen/05%2008%2017%20-%20Media%20Release%20-%20Petron%20Posts%20Record%20Quarter%20Hits%20P5.6%20Billion%20in%20Net%20Income.ashx?App=Announcement&FileID=452503

5. Long term value is between RM12 to RM15 per share. There is more than 50% upside that I am looking at. I think that the Company is worth between 8x to 10x PE. The 8x PE is if you take oil and gas Company PE. While the 10x PE is the minimum for consumer sector PE. I think PETRONM is a mixture of O&G and CONSUMER because its petrol station business is basically similar to 7 ELEVEN. For FY17, the 1Q net profit is assumed at RM130m and I multiply this by 3 to get the full year earnings. I purposely ignore one quarter for conservativeness purpose in my calculation (that's why not multiplying by 4).

That gives me FY17 earnings of around RM390m (or RM1.45 of EPS).

8x PE * RM1.45 FY17 EPS = RM11.60 (round up to RM12)

10x PE * RM1.45 FY17 EPS = RM14.50 (round up to RM15)

For record keeping purpose, I am using last Tuesday closing price of RM7.97

Friday, March 10, 2017

數據不會“說謊”,白銀值得持有的三大理由

匯金網訊: 白銀市場的需求正在回升,儘管目前水平與2016年7月觸及的高點仍相距甚遠。美國白銀期貨市場顯示白銀受到投資者熱捧,自2015年中期以來,中國持有白銀的數量也迅速攀升。此外,摩根大通也在積極囤積白銀。

【理由一、生產商持有的白銀凈空頭頭寸攀升】

美國白銀期貨市場顯示白銀受到投資者熱捧,生產商持有的白銀期貨的總頭寸達到了19.76萬手合約,而去年八月觸及的記錄高位是22.45萬手合約。

(生產商持有白銀凈頭寸)

截至2017年2月28日,生產商持有的白銀凈空頭頭寸達到了54.7%,這是自2016年初開始的白銀上漲周期中最大的比例。生產商持有大量的凈空頭頭寸相當於投機者持有大量的凈多頭頭寸,這推高了白銀價格。

而有趣的是,白銀價格較2016年8月初下跌了11.4%,現貨白銀目前交投於17.81美元/盎司。

但是兩個跡象顯示了投資者對白銀的需求正在升溫:生產商持有的凈空頭頭寸較去年八月高(54.7% VS 48.6%),投機者持有的凈多頭頭寸高於去年八月(48.3% VS 44.5%)。

(投機者持有的凈多頭頭寸)

四家最大的生產商持有的白銀期貨凈空頭頭寸自2014年底以來一直處於上升趨勢,而目前幾乎接近這一周期中的觸及的最高水平。

(四家最大的生產商持有的白銀期貨凈空頭頭寸)

【理由二:中國持有白銀的庫存迅速攀升】

自2015年中期以來,中國持有白銀的數據迅速攀升。截至2017年1月底,上海期貨交易所持有的白銀庫存達到紀錄水平6410萬盎司,而這一數據自那時起持續增加,目前已經攀升至6870萬盎司。

(上海期貨交易所白銀庫存)

【理由三:國際大投行摩根大通積極囤積白銀】

此外,摩根大通也在積極囤積白銀。自2016年底以來,摩根大通增持了940萬盎司白銀。這對白銀走勢發出更加積極的信號。

不過北美的投資者似乎對白銀的熱情減弱。iShares白銀信託基金,世界上最大的私人白銀持有者,其公布的報告顯示,自2017年初以來,白銀持有量下降了860萬盎司。

【理由一、生產商持有的白銀凈空頭頭寸攀升】

美國白銀期貨市場顯示白銀受到投資者熱捧,生產商持有的白銀期貨的總頭寸達到了19.76萬手合約,而去年八月觸及的記錄高位是22.45萬手合約。

(生產商持有白銀凈頭寸)

截至2017年2月28日,生產商持有的白銀凈空頭頭寸達到了54.7%,這是自2016年初開始的白銀上漲周期中最大的比例。生產商持有大量的凈空頭頭寸相當於投機者持有大量的凈多頭頭寸,這推高了白銀價格。

而有趣的是,白銀價格較2016年8月初下跌了11.4%,現貨白銀目前交投於17.81美元/盎司。

但是兩個跡象顯示了投資者對白銀的需求正在升溫:生產商持有的凈空頭頭寸較去年八月高(54.7% VS 48.6%),投機者持有的凈多頭頭寸高於去年八月(48.3% VS 44.5%)。

(投機者持有的凈多頭頭寸)

四家最大的生產商持有的白銀期貨凈空頭頭寸自2014年底以來一直處於上升趨勢,而目前幾乎接近這一周期中的觸及的最高水平。

(四家最大的生產商持有的白銀期貨凈空頭頭寸)

【理由二:中國持有白銀的庫存迅速攀升】

自2015年中期以來,中國持有白銀的數據迅速攀升。截至2017年1月底,上海期貨交易所持有的白銀庫存達到紀錄水平6410萬盎司,而這一數據自那時起持續增加,目前已經攀升至6870萬盎司。

(上海期貨交易所白銀庫存)

【理由三:國際大投行摩根大通積極囤積白銀】

此外,摩根大通也在積極囤積白銀。自2016年底以來,摩根大通增持了940萬盎司白銀。這對白銀走勢發出更加積極的信號。

不過北美的投資者似乎對白銀的熱情減弱。iShares白銀信託基金,世界上最大的私人白銀持有者,其公布的報告顯示,自2017年初以來,白銀持有量下降了860萬盎司。

來源: 匯金網

Friday, February 10, 2017

[Sponsored Infographic] The Berkshire of Malaysia - Insas Berhad

[Sponsored Infographic] The Berkshire of Malaysia - Insas Berhad

http://klse.i3investor.com/blogs/donkeystocks/115492.jsp

Insas Berhad, which is the parent company of several notable industry key players, such as Inari Amertron, Ho Hup Construction, SYF Resources and Omesti Berhad. Insas is arguably the mini Berkshire in Malaysia.

http://klse.i3investor.com/blogs/donkeystocks/115492.jsp

Insas Berhad, which is the parent company of several notable industry key players, such as Inari Amertron, Ho Hup Construction, SYF Resources and Omesti Berhad. Insas is arguably the mini Berkshire in Malaysia.

Tuesday, January 3, 2017

The building of EKOVEST & What are the plans ahead for Ekovest

Making strides: Lim with the KL River City project, which he envisions to turn into a thriving community like Yarra of Melbourne.

DATUK Seri Lim Keng Cheng was born in Jalan Gombak and studied at Setapak High School. Now, he has his eyes set on transforming the Sentul-Gombak-Setapak area, which he says is still underdeveloped. He aims to make the area into a liveable place like Melbourne.

This 54-year-old Sentul homeboy (who goes by the initials KC), the managing director of Ekovest Bhd, has rebuilt a Chinese primary school and a high school there.

Until recently, KC has not made himself distinctively known to the corporate world. His name did not pop into view when the media wrote about Ekovest and Iskandar Waterfront City Bhd (IWC). Only Tan Sri Lim Kang Hoo, the Ekovest executive chairman and KC’s uncle, was mentioned.

Yet, KC is the driving force behind Ekovest, which is Kuala Lumpur City Hall’s project delivery partner for the River of Life project and DUKE highways.

Early victory: Lim with a picture of a project he undertook in his early years in Sabah. He says he and his uncle Tan Sri Lim Kang Hoo made their first RM100mil while they were in Sabah.

Indeed, KC has been in the construction, property and infrastructure line for more than 30 years.

“I am a business partner of Tan Sri Lim Kang Hoo. Before Ekovest, we were already doing business together,” declares KC.

“But since he is my uncle and executive chairman of Ekovest, and holds 32% stake in the company, while I have only 6.12%, I should give him due respects,” adds KC at the outset of a recent interview with Sunday Star.

Yes, for too long, this trilingual and energetic man who has worked alongside Kang Hoo quietly to jointly build up their companies, including Ekovest and IWC. However, many are not aware of this fact.

KC’s role in Ekovest

Acknowledgement of KC’s role in Ekovest is stated in its latest company profile. Under the section Capable Management Team, the company writes: “Executive chairman Tan Sri Datuk Lim Kang Hoo and managing director Datuk Seri Lim Keng Cheng have been managing the company since (its) inception”.Venturing into Sabah together with his uncle while he was 25 in the early 1980s, this neat-looking man proudly claims he was responsible for the building infrastructure in Felda Sahabat, twice the size of Singapore.

“We made our first RM100mil in Sabah,” says KC, as he shows photographs of the Sabah projects in his office that carry his footprint.

“I was born here, in Batu 4, Jalan Gombak, in a house with number 229A. However, there was no road linking my old house to the main road then. Kang Hoo also lived there then.

“The Sentul-Gombak-Setapak area is still an underdeveloped area. I want to transform this into a liveable place. This is why I want to do a lot of development and CSR work here,” says KC in Ekovest’s office, which stands obliquely opposite the area where he was born.

“The old house is still there. We – including Kang Hoo – still celebrate Chinese New Year there. But now, we have already built a road to connect with the main road,” adds KC as he flashes his handphone to show the location of his old house.

Due to his humble background and vast experience in infrastructure, KC says he could plan cost efficient and workable highways.

In this regard, he has contributed significantly to the success of the Duta-Ulu Kelang Expressway (DUKE). He is also instrumental in convincing Kuala Lumpur City Hall (DBKL) to grant further concessions to Ekovest to extend the DUKE expressways, named as DUKE-3.

DUKE-1 and DUKE-2 are providing alternative routes for road users and have served as an efficient traffic dispersal system in and around Kuala Lumpur to relief traffic congestion.

Toll collection and recent sale of a 40% stake in DUKE-1 and DUKE-2 have boosted the earnings of Ekovest and this is reflected in the rise of its share price. On Thursday, Ekovest share closed at RM2.35 – which was at a six years’ high.

Another of KC’s passionate project is the River of Life project, which involves the improvement of water quality and beautification works along the river from Gombak to the Kuala Lumpur city centre.

Ekovest, which has land-bank and property development projects such as EkoRiver Centre and Ekovst Tower along the river, has on its plate a total GDV of RM7.8bil when all the planned projects are completed.

“My vision is to convert the entire run-down area into a river city with waterfront property development and leisure activities. It will be a place for people to work, live, jog and cycle, cruise in water taxi like the Yarra River of Melbourne.

“Our vision of creating a world class river front development along Gombak River is gaining momentum and we are looking to deliver some of the most vibrant commercial and residential properties in this area.”

According to KC, multi-billionaire Kang Hoo – ranked as one of the top 30 tycoons in Malaysia by Forbes Asia in 2014 – is focussing his attention on IWC and the development of Bandar Malaysia.

KC is charged with taking care of Ekovest.

In a two-hour interview, KC talks enthusiastically about Ekovest projects, his vision and education. Below are excerpts:

Q: What is the latest on DUKE highways? Why are these highways so successful?

A: We have a DUKE Master Plan, with a total of ten functional and cost-effective highways. We are developing the third one. Our planning team will keep submitting proposals on future DUKE projects as and when the need arises.

Within this plan, we provide one tolled road system on top of an existing council road to give an alternative route for drivers who are willing to pay to avoid traffic jams.

We have studied the benefits to be enjoyed by road users and planned according to their needs. This is the success story of our DUKE.

The DUKE concept was based on a study done by JICA (Japan International Cooperation Agency) in the 1980s to fill in the gap in highway connectivity. We submitted our plan to DBKL and got the approval.

There are many highways all over Kuala Lumpur, but they are not connected. We fill in this gap and build “highway connectors”.

But we also innovate to add value to our highways. For example, we are building DUKE-2’s integrated park-and-ride facility at the Segambut Toll Plaza that will allow DUKE’s users to park their cars and hitch a KTM ride at a brand new KTM (train) station, which is two stops away from KL Sentral.

Known as Segambut Rest and Service Area, this park-and-ride complex will be able to house 4,000 cars. This will ensure fewer cars move into and out of the city centre. Hence, it will reduce traffic congestion. (The new KTM train station is expected to be completed in 2018)

Your property development projects appear to concentrate in the Sentul area.

I was born here. My original home is still here. There was no access road from Jalan Gombak to my old house, yet the postman could find it.

My father passed away when I was 14 years old. My study was funded by Lee Foundation. For this reason, I have rebuilt the Lee Rubber primary school building in this area. From road construction and property development to the River of Life project, I hope to create a liveable Sentul-Gombak-Setapak region The whole city will be like Melbourne and Vancouver.

All these years, you have been overshadowed by Tan Sri Lim Kang Hoo, although you are a property man in your own right. Is this observation accurate?

Ekovest, with total staff of 2,000, is managed by a committee. No single person makes the decision.

My uncle Kang Hoo holds a 32% stake in the company while I have 6.12%. As he is my uncle and the company’s executive chairman, I should give him due respects. When my father died, the small family construction outfit run by him was taken over by Kang Hoo. I started helping him when I was in high school.

When I was 25, we went to Sabah together and worked on the infrastructure of Felda Sahabat. In Lahad Datu, we provided 2,500 jobs to the gun-wielding unemployed and helped solve the social problems there.

While in Sabah, we took over a RM2 company called Ekovest. That’s where we made our first RM100mil for Ekovest. After that, we went to Labuan to build the offshore financial centre. Kang Hoo and I were business partners before Ekovest, and are still partners.

Now, Kang Hoo places his focus on IWC and Bandar Malaysia investment, while I take charge of Ekovest projects.

What are the plans ahead for Ekovest?

We will keep inviting institutional funds, such as EPF (Employees’ Provident Fund), to be our investors and strategic partners. These partners will stay and grow with the company. They will become our strong pillars.

Recently, we let go of a 40% stake in Duke-1 and Duke-2 to EPF for RM1.13bil. This will pave way for future partnerships.

We will do the same for future DUKEs and KL River City project. The funds obtained will be used to reward shareholders in the form of special dividend and finance new ventures.

(Ekovest has announced that it is distributing a special dividend to shareholders from the proceeds of its sale to EPF).

We have also set the target to become the top 30 listed companies on Bursa Malaysia within five years. This means that our market capitalisation has to hit RM10bil within five years, from the current RM2bil. It is achievable based on our growth.

But while doing so, we must maintain our policy to give out dividends every year. Since 1993, we have been profitable. This is something we are proud of.

We also believe in doing CSR work. We have given Chong Hwa Independent High School a total of RM2mil and next year another RM1mil. For the Government’s SM Chong Hwa, we have given RM3mil.

How do you see Ekovest’s future financial performance?

We are doing very well. Our order book is very healthy, with total outstanding external order book of RM4.89bil as at November 2016.

For the current financial year, we won the biggest-ever project (DUKE-3) worth RM3.74bil, with a 50-year concession to collect tolls. That means our construction segment will be busy for the next three and a half years.

In November 2016, we have also been awarded two contracts to improve and beautify the Klang and Gombak rivers.

The results for the year ending June 2017 will be much better. You can see from our revenue growth. It’s almost doubled in 2016. There is also vast improvement in net profit. (Ekovest posted a revenue of RM794mil and net profit of RM155.4mil for the year ending June 2016, compared to a revenue of RM438mil and net profit of RM18.5mil in previous year).

Does the high-level connection of Tan Sri Lim help in any way to obtain projects?

Ekovest is run professionally.

Based on our technical expertise and our ability to see what people need, we won these public transport projects. There is no objection from people when our projects are displayed to gauge the public reaction. This is because our projects fill in the gap and we collect toll to help future projects.

It is not political connections that help us get jobs. We think out of the box using blue ocean strategy, hence, we came out with the master plan for DUKE highways.

If it was political link, we would have risen sky high long ago.

We will self-create and generate income. In DUKE, we carry out the planning and infrastructure for the government, create income for future highways.

Nowadays, it is impossible for you to bulldoze through projects. You need to do surveys and carry out public engagement. No one has objected to our DUKE highway projects so far.

What is your vision for Ekovest?

I want to create a sustainable city, not just high-rise only. I want to innovate to create value. I also want other people to learn from us when I give media interviews.

2017 stock picks

Reshuffle my portfolio to match 2017 picks soon.

Stock Name

Last Price

|

Change

|

Shares

|

Market Value

|

%

|

Average Cost

|

Per Share

|

Unrealized Gain

|

%

|

Day Gain

|

%

| ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

AEONCR AEONCR | MYR | 14.36 | -0.02 | 1,000 | 14,360.00 | 14.40% | 14,394.79 | 14.394 | -34.79 | -0.24% | -20.00 | -0.14% |

| BORNOIL | MYR | 0.18 | 0.00 | 38,000 | 6,840.00 | 6.86% | 6,857.65 | 0.180 | -17.65 | -0.26% | 0.00 | 0.00% |

| DATAPRP | MYR | 0.135 | 0.00 | 40,000 | 5,400.00 | 5.41% | 5,416.20 | 0.135 | -16.20 | -0.30% | 0.00 | 0.00% |

| EKOVEST | MYR | 2.38 | +0.03 | 6,000 | 14,280.00 | 14.32% | 14,314.68 | 2.385 | -34.68 | -0.24% | +180.00 | 1.28% |

| FLBHD | MYR | 1.60 | -0.01 | 6,000 | 9,600.00 | 9.62% | 9,623.23 | 1.603 | -23.23 | -0.24% | -60.00 | -0.62% |

| HEXZA | MYR | 0.925 | +0.005 | 5,500 | 5,087.50 | 5.10% | 5,103.60 | 0.927 | -16.10 | -0.32% | +27.50 | 0.54% |

| JCBNEXT | MYR | 1.70 | 0.00 | 3,000 | 5,100.00 | 5.11% | 5,116.10 | 1.705 | -16.10 | -0.31% | 0.00 | 0.00% |

| MMCCORP | MYR | 2.33 | +0.02 | 2,000 | 4,660.00 | 4.67% | 4,674.96 | 2.337 | -14.96 | -0.32% | +40.00 | 0.87% |

| MSC | MYR | 3.93 | -0.01 | 7,500 | 29,475.00 | 29.55% | 29,545.62 | 3.939 | -70.62 | -0.24% | -75.00 | -0.25% |

| TIENWAH | MYR | 1.76 | -0.03 | 2,800 | 4,928.00 | 4.94% | 4,943.05 | 1.765 | -15.05 | -0.30% | -84.00 | -1.68% |

| $CASH | 10.12 | 0.01% | ||||||||||

| Total | 99,740.62 | 100.00% | +8.50 | 0.01% | ||||||||

My stock pick results 2016

As per closing 2016, hopefully another good year on 2017.

I target 25% and above every year in order to double my money every 4 years

I target 25% and above every year in order to double my money every 4 years

Stock Name

Last Price

|

Change

|

Shares

|

Market Value

|

%

|

Average Cost

|

Per Share

|

Unrealized Gain

|

%

|

Day Gain

|

%

| ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AIRASIA | MYR | 2.29 | +0.01 | 10,000 | 22,900.00 | 17.36% | 12,930.79 | 1.293 | +9,969.21 | 77.10% | +100.00 | 0.44% |

| FAVCO | MYR | 2.38 | -0.01 | 1,900 | 4,522.00 | 3.43% | 5,222.13 | 2.748 | -700.13 | -13.41% | -19.00 | -0.42% |

| GKENT | MYR | 3.04 | -0.01 | 6,250 | 19,000.00 | 14.41% | 8,170.24 | 1.307 | +10,829.76 | 132.55% | -62.50 | -0.33% |

| IWCITY | MYR | 0.805 | -0.02 | 10,000 | 8,050.00 | 6.10% | 10,124.93 | 1.012 | -2,074.93 | -20.49% | -200.00 | -2.42% |

| KESM | MYR | 9.85 | +0.02 | 5,000 | 49,250.00 | 37.34% | 26,011.77 | 5.202 | +23,238.23 | 89.34% | +100.00 | 0.20% |

| MJPERAK | MYR | 0.26 | 0.00 | 27,000 | 7,020.00 | 5.32% | 8,931.30 | 0.330 | -1,911.30 | -21.40% | 0.00 | 0.00% |

| MUDAJYA | MYR | 0.91 | +0.005 | 5,000 | 4,550.00 | 3.45% | 5,916.36 | 1.183 | -1,366.36 | -23.09% | +25.00 | 0.55% |

| PRKCORP | MYR | 1.67 | 0.00 | 6,000 | 10,020.00 | 7.60% | 15,998.00 | 2.666 | -5,978.00 | -37.37% | 0.00 | 0.00% |

| WTK | MYR | 0.995 | +0.005 | 5,000 | 4,975.00 | 3.77% | 6,617.58 | 1.323 | -1,642.58 | -24.82% | +25.00 | 0.51% |

| $CASH | 1,605.50 | 1.22% | ||||||||||

| Total | 131,892.50 | 100.00% | -31.50 | -0.03% | ||||||||

Subscribe to:

Posts (Atom)